This trillion-dollar tech company became revolutionary by constantly updating its technology, setting Uniform ROAs of 40%+

This multinational tech company continues to grow more popular as it upgrades its lineup of leading-edge gadgets.

Despite not being the first to market some of the most innovative technologies in the consumer tech industry—touchscreen smartphones or Face ID, to name a few—this company became an industry leader due to its rigorous process of perfecting technology that already exists, and offering the best user experience.

While as-reported data suggests that being an optimizer has been widely unsuccessful, Uniform Accountings shows that this is exactly the reason why it’s been able to maintain robust profitability levels of more than 40%.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

In 2001, Apple (AAPL) transformed the way people listened to music with the launch of its MP3 player, the iPod. The launch revived the company who almost filed for bankruptcy a few years earlier.

Six years later, the company released the iPhone, which would eventually shape the smartphone industry as we know it. The iPhone was, as Steve Jobs aptly put it, “revolutionary.” It was a phone, a camera, an MP3 player, a browser, a notebook, and so much more rolled into one.

These were innovative technologies that changed the world, but Apple wasn’t the first-to-market with these new ideas.

The first MP3 player, called MPMan, was launched by a South Korean company in 1997. Likewise, the first known touchscreen smartphone was introduced by IBM in 1994.

The reason why Apple’s products grew to be far more popular is simply because the company does them significantly better. Instead of looking to rush ideas to the market, the company made sure the product would meet rigorous quality standards and is optimized for a superior user experience.

Just last week, Apple released four new iPhone models: a regular, a mini, a Pro, and a Pro Max. The 12-model line has improved cameras and displays, as well as other incremental hardware and software tweaks, including 5G capability.

These are some of the best, if not the best, smartphones currently in the market—the only other close rival is Samsung’s latest Android phone, the Galaxy S20.

So although the company hasn’t always been the first to introduce new features and capabilities, the strategy of optimizing existing technology to create the best, most unified user experience has made Apple into one of the few companies to ever reach a trillion-dollar market cap.

However, recent as-reported ROAs of only around 11%-12% doesn’t indicate that Apple is the unrivaled trillion-dollar behemoth that it is.

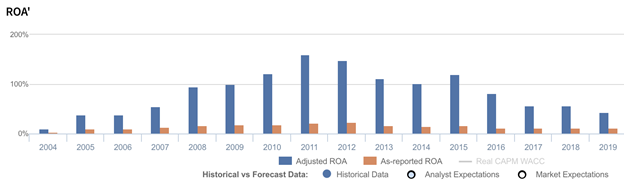

In reality, evaluating the company through the lens of Uniform Accounting, we can see that Apple lives up to its market value, with Uniform ROAs that range from 43%-58%, almost 5x the as-reported.

A source of the distortion between Uniform and as-reported ROAs comes from as-reported metrics incorrectly treating R&D as an expense.

R&D is an investment in the long-term cash flow generation of the company. By recording R&D as an expense, this violates one of the core principles of accounting, which is that expenses should be recognized in the period when the related revenue is incurred.

Since as-reported accounting records R&D on the income statement, as opposed to as an investment on the balance sheet, net income can become materially understated.

Apple materially spends on R&D to continue serving best-in-class products to its consumers. The company’s R&D spend has consistently been about 50% of total operating costs.

After adjustments, we can see that Apple’s Uniform ROA is materially higher than as-reported ROAs. Without this adjustment, it will look like the firm is having less success with its R&D investments than it really is, leading to poorer valuations.

However, despite current Uniform ROAs sustaining its strength, they have fallen massively from a peak of 159% in 2011 as the company became less of an innovator and more of a follower in recent years.

Features like Face ID and triple cameras, and products like smart watches and wireless headphones have rolled out in Android devices long before Apple did.

So, while the strategy of optimizing technology to create superior products has worked well to keep Uniform ROAs robust, the lack of disruptive innovation has caused a declining trend in returns.

Apple’s earning power is actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

Apple’s Uniform ROA has actually been higher than its as-reported ROA in the past sixteen years. For example, as-reported ROA was 11% in 2019, but its Uniform ROA was actually over 4x higher at 43%.

Specifically, Apple’s Uniform ROA has ranged from 10%-159% in the past sixteen years while as-reported ROA ranged only from 3%-24% in the same timeframe.

After gradually expanding to a peak of 159% in 2011, Uniform ROA declined to 102% in 2014, before briefly improving to 120% in 2015. Since then, Uniform ROA has compressed to 43% in 2019.

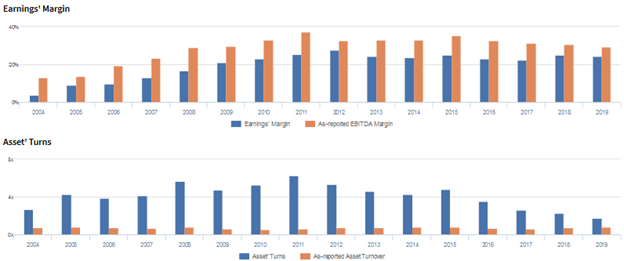

Apple’s Uniform earnings margins are weaker than you think, but its robust Uniform asset turns make up for it

Apple’s trends in Uniform ROA have been driven by compounding trends in Uniform earnings margins and Uniform asset turns.

Uniform margins reached a peak of 28% in 2012, before compressing to 22%-25% levels in 2013-2019.

Meanwhile, Uniform turns consistently improved from 2.7x to a peak of 6.3x from 2004-2011, excluding a 5.7x outperformance in 2008. Thereafter, Uniform turns declined to a low of 1.8x in 2019.

At current valuations, markets are pricing in an expectation for Uniform margins to remain near current levels and for Uniform turns to continue deteriorating.

SUMMARY and Apple Tearsheet

As the Uniform Accounting tearsheet for Apple Inc. (AAPL) highlights, the Uniform P/E trades at 29.2x, which is above corporate average valuation levels and its own recent history.

High P/Es require high EPS growth to sustain them. In the case of Apple, the company has recently shown a 2% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Apple’s Wall Street analyst-driven forecast is a 73% EPS contraction in 2020 and a 12% EPS growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Apple’s $119 stock price. These are often referred to as market embedded expectations.

The company needs Uniform earnings to grow 12% each year over the next three years to justify current prices. What Wall Street analysts expect for Apple’s earnings growth is below what the current stock market valuation requires in 2020, but in line with its requirement in 2021.

Furthermore, the company’s earning power is 7x the corporate average. Also, cash flows and cash on hand are 3x higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low credit and dividend risk.

To conclude, Apple’s Uniform earnings growth is below its peer averages in 2020, but the company is above its average peer valuations.

About the Philippine Markets Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com