This utilities company powered up its growth initiatives, reaching a Uniform ROA of 8%, not 5%

Since 1998, this utilities company has acted as the Philippines’ pioneer in furthering the shift to renewable energy, undertaking growth projects to achieve a decarbonized world for the Philippines.

However, as-reported metrics seem to be downplaying this company’s profitability amid its efforts to go green. In reality, its Uniform return on assets (ROA) show the business is more profitable than you might think.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

The renewable energy industry continues to make waves across the globe as governments and interest groups tackle global warming and climate change.

According to Allied Market Research, the renewable energy industry was valued at $881.7 billion in 2020, with projections to reach $1,977.6 billion by 2030.

Renewable energy—hydro, geothermal, wind, and solar—only makes up 24% of the Philippines’ energy profile. The country is still mostly powered by coal at 47%, while the remaining is natural gas at 22% and oil-based at 6.2%

One company that specializes in the renewable industry is First Gen Corporation (FGEN:PHL). It is an investment holding company in the Philippines engaged in various forms of power generation, such as wind, solar, natural gas, geothermal, and hydropower, with energy facilities located across the country.

However, despite its market leadership, First Gen posted lukewarm earnings for the first half of 2022, with its recurring net income coming in at just PHP 6.6 billion, down 13% from the recorded PHP 7.1 billion in the same period last year.

This weaker result was partly due to inclement weather and unplanned outage issues. Typhoon Odette caused destructive effects on the company’s Visayas plants, while the Avion gas-fired plant in Batangas City had to temporarily shut down due to damages to one of its compressors.

Then there is also the effect of supply chain restrictions on operations. The company is heavily reliant on the Malampaya gas fields. However, given that the reserves in this field have been slowly depleting, First Gen had to prioritize looking for international suppliers to fulfill its natural gas requirements.

Regardless, First Gen continues to expand its operations and pursue growth projects. Specifically, the company announced its plans to launch its own LNG import terminal by early 2023.

First Gen was also awarded a 10-year power supply contract with the island of Bohol through Energy Development Corporation (EDC), one of its main subsidiaries. This collaboration would enable EDC to provide existing Bohol power utilities with baseload power supply from renewable energy to prevent future power outages.

On top of that, First Gen allotted a hefty PHP 29 billion CapEx in 2022, with the majority of it going towards growth projects and initiatives. These include its 3.6-megawatt (MW) Mindanao 3 and 29-MW Palayan Bayan binary projects, as well as the 20-megawatt Tanawon geothermal power plant.

Overall, the company’s focus on growth and innovation with respect to renewable energy appears to be unhampered by the various obstacles it currently faces. However, as-reported data seems to show otherwise.

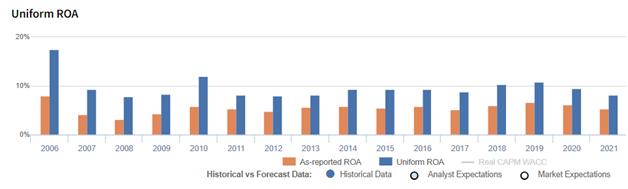

In reality, the company actually did way better than expected with these initiatives, with Uniform ROAs performing above cost of capital levels at 8%.

Historically, one of the largest distortions for First Gen comes from the treatment of minority interest expenses or the income attributable to the non-controlling interests of a company’s subsidiaries.

The Philippine Financial Reporting Standards (PFRS) allows minority interest expense to be recognized under operating cash flow, leading people to incorrectly think that it is essential to the firm’s core operations.

In reality, it should always be classified as a financing cash flow. Minority shareholders provide capital to the subsidiary in exchange for a piece of the company’s profits. As a result, minority interest expense should not be subtracted from revenue when calculating a company’s real core earnings.

In 2021, First Gen recognized PHP 96.0 million in minority interest expense, resulting in a PHP 258 million net profit and a 5% as-reported ROA. Adding this back alongside the many other adjustments Valens makes, the company should actually be recognizing PHP 338 million in Uniform earnings and an 8% Uniform ROA.

First Gen’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that First Gen’s profitability has been weaker than real economic metrics highlight.

Through Uniform Accounting, we can see that the company’s true ROAs have been mostly understated over the past sixteen years. For example, as-reported ROA was 5% in 2021, but its Uniform ROA was actually higher at 8%.

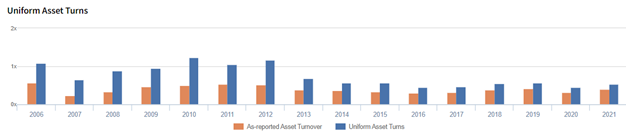

First Gen’s assets are more efficient than you think

Trends in Uniform ROA have been driven by trends in Uniform asset turns. For more than two decades, as-reported metrics have understated First Gen’s asset efficiency, a key driver of profitability.

Moreover, as-reported asset turnover has reached a peak of 0.6x. In comparison, Uniform turns have reached a high of 1.2x over the same time period, making First Gen appear to be a less efficient business than real economic metrics highlight.

SUMMARY and First Gen Corporation Tearsheet

As our Uniform Accounting tearsheet for First Gen Corporation (FGEN:PHL) highlights, the company trades at a Uniform P/E of 6.1x, below the global corporate average of 19.3x and its historical P/E of 8.3x.

Low P/Es require low EPS growth to sustain them. In the case of First Gen, the company has recently shown a 6% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, First Gen’s sell-side analyst-driven forecast is to see Uniform earnings growth of 18% in 2022 and 2023.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify First Gen’s PHP 18.00 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink 20% in each year over the next three years. What sell-side analysts expect for First Gen’s earnings growth is well above what the current stock market valuation requires in 2022 and 2023.

Moreover, the company’s earning power is above the long-run corporate average. Also, cash flows and cash on hand are 2x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low dividend and credit risk.

Lastly, First Gen’s Uniform earnings growth is in line with its peer averages, but is trading below its average peer valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com