Uniform Accounting cleans up this renewable energy company’s financials, revealing a 16% earning power, not just twice the cost of capital!

This Chinese company’s products support sustainability as they promote clean energy by manufacturing solar PV inverters, wind power converters, and other power supplies.

However, as-reported metrics do not reflect how the company is benefiting from the increasing demand for renewable energy.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

With large environmental and social problems emerging worldwide, sustainability has become an important and pressing issue. Sustainability is defined as the capacity for ecosystems and mankind to coexist, so that natural resources are not depleted while still maintaining a certain level of quality of life.

To ensure sustainability, businesses are now being urged to consider the long-term environmental and social impact of their business decisions. In some countries, governments encourage sustainability by giving tax incentives or subsidies to companies that actively pursue eco-friendly projects.

Companies in alternative energy sources have benefited from this sustainability movement.

Although the coronavirus pandemic has delayed numerous clean energy construction projects, this Chinese company has managed to quickly respond to changes brought about by the crisis.

Though China is still the world’s largest producer of carbon emissions, it is also the global leader in renewable energy investments. At the forefront of this is Sungrow Power Supply Co., Ltd.

The coronavirus pandemic has had minimal negative effects on the business, with the majority of customer orders’ processing and delivery remaining on schedule. Sungrow has also continued to increase its R&D investments amidst the crisis to further innovate its products.

Sungrow offers clean and sustainable power to residential, commercial, and industrial areas through its PV inverter and storage technology. The company also provides a floating system for water installations, having created the world’s largest floating PV plant.

In 2019, the company’s revenue increased by 25.4% and overseas shipments increased by 87.5%, making it the first inverter manufacturer in the world to accumulate 100GW in shipments. Recently, Sungrow announced that it will be supplying 1500V SG250HX inverter solutions to a project in Oman’s largest utility-scale PV plant in the Sultanate.

Oman has chosen Sungrow’s products in order to increase the country’s renewable energy mix by 10%. Since the project is located in the desert, Sungrow’s SG250HX, the world’s most powerful 1500V string inverter, is ideal to withstand high temperatures and maximize profitability.

Furthermore, the company is also partnering with Huanghe Hydropower Development Co., Ltd. to supply PV inverter solutions and energy storage systems to a PV-plus-storage project in Northwest China’s Qinghai Province. Huanghe Hydropower praises Sungrow for being the first ever company to pass the functional test of synergizing control of both PV and energy storage systems. This serves to be a milestone for Sungrow in globalizing PV-plus-storage landscape.

Given all of Sungrow’s initiatives and offerings, it’s likely that it will see significant opportunities going forward.

According to a report published by the International Energy Agency (IEA), solar, wind, and hydropower projects will roll out at their fastest rate over the next four years. The agency also predicted that the world’s solar power capacity will grow by 600GW in 2024.

Global renewable energy supplies are forecast to increase by 50% in the next five years, with most of it to be contributed by solar energy.

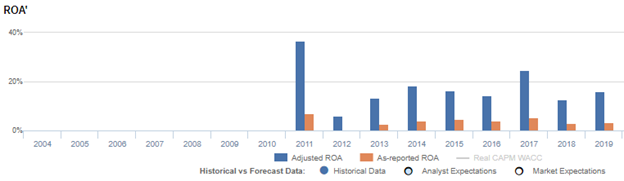

Despite the company’s strong offerings combined with the expansion of renewable energy, its profits are still below cost of capital levels based on as-reported figures. As-reported return on assets (ROA) in 2019 was only at 3%, making it look weaker than what it actually is.

Sungrow’s real economic profitability can be better reflected with Uniform Accounting adjustments. Looking at the company’s performance in 2019, Sungrow’s Uniform ROA is at 16%, which is more than 5x its as-reported ROA of 3%.

One key metric that is causing distortions in as-reported ROAs is R&D expenses.

Sungrow has regular material investments in research and development that they record as an outright expense, in accordance with the accounting standards. However, expensing R&D fails to recognize the matching principle of recognizing expenses in the period when the related revenue is incurred.

R&D investment is actually an investment in the long-term cash flow generation of the company. If this remains treated as an expense, the company’s profitability may appear substantially weaker than it actually is.

After R&D and other significant adjustments are made, the company’s Uniform ROA is at 16% in 2019, which is more than 5x stronger than their as-reported ROA of 3%.

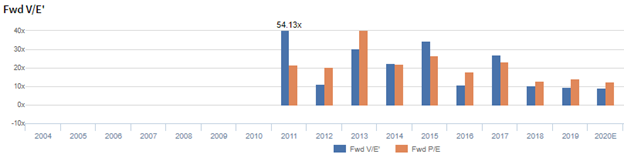

Sungrow’s valuations are cheaper than corporate averages

Sungrow Power Supply Co., Ltd. (300274:CHN) currently trades below corporate averages at a 10.1x Uniform P/E (blue bars), which is also cheaper than its as-reported P/E of 12.6x (orange bars).

At these levels, the market is pricing in expectations for Uniform ROA to fall to 3% in 2024, accompanied by 26% Uniform asset growth going forward.

However, analysts have less bearish expectations, projecting Uniform ROA to only slightly decrease to 17% in 2021, accompanied by a 13% Uniform asset growth.

Sungrow’s profitability is much better than you think it is

As-reported metrics are distorting the market’s perception of the firm’s profitability.

If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight.

Sungrow’s Uniform ROA has actually been higher than its as-reported ROA in the past nine years. For example, as-reported ROA is 7% in 2011, significantly lower than its Uniform ROA of 37%. When Uniform ROA reached 16% in 2019, as-reported ROA was just at 3%.

Through Uniform Accounting, we can see that the company’s true ROAs have actually been higher. Sungrow’s Uniform ROA for the past nine years has ranged from 6% to 37%, while as-reported ROA ranged only from 0% to 7% in the same timeframe.

From a peak of 37% in 2011, Uniform ROA fell to an all-time low of 6% in 2012, then gradually recovered to 25% in 2017. Afterwards, Uniform ROA fell to 13% in 2018, before improving to 16% in 2019.

Sungrow’s margins may be weaker than you think, but its stronger turns makes up for it

Cyclicality in Uniform ROA has been primarily driven by both trends in Uniform asset turns and Uniform earnings margins, with peaks and troughs lining up historically with that of Uniform ROA.

Uniform earnings margins fell from 22% in 2011 to 6% in 2012, before gradually recovering to 14% in 2017. It then declined to 9% in 2019.

Meanwhile, Uniform asset turns slumped from 1.6x in 2011 to a historical low of 1.0x in 2012 before recovering to 1.8x in 2017. It then fell back to 1.4x in 2018, before rebounding to 1.8x in 2019.

SUMMARY and Sungrow Power Supply Co., Ltd. Tearsheet

As the Uniform Accounting tearsheet for Sungrow Power Supply Co., Ltd. (300274:CHN) highlights, the Uniform P/E trades at 10.1x, which is below corporate average valuation levels and its own recent history.

Low P/Es require low EPS growth to sustain them. In the case of Sungrow, the company has recently shown a 25% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Chinese Accounting Standards (CAS) earnings and convert them to Uniform earnings forecasts. When we do this, Sungrow’s sell-side analyst-driven forecast is a 24% and 18% growth in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Sungrow’s CNY 11.00 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 13% each year over the next three years and still justify current price levels. What sell-side analysts expect for Sungrow’s earnings growth is above what the current stock market valuation requires in 2019 and 2020.

The company’s earning power is 3x the corporate average. Also, cash flows are 6x higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Sungrow’s Uniform earnings growth is in line with its peer averages in 2019. However, the company is trading below average peer valuations.

About the Philippine Market Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com