Uniform Accounting gives us a crash course on how this college textbook provider earned ROAs that are 2x stronger than as reported

Unyielding competition from trillion-dollar competitors Amazon and Apple spelled trouble for America’s largest retail bookstore chain, Barnes and Noble. This led to the spin-off of Barnes and Noble’s more profitable college textbook business in order to survive.

In effect, this spun-off company has become the largest operator of physical and virtual bookstores for colleges and universities across the U.S.

But while as-reported metrics make it seem that the spin-off to focus on the niche higher education market hasn’t been as lucrative as expected, with return on assets (ROAs) at only sub-3% levels, Uniform Accounting reveals that the company’s returns are at least twice as strong.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

Barnes and Noble is America’s largest retail bookstore chain—and the last one.

Following the broader digitalization trend, eBooks have risen in popularity throughout the last decade. The growth began when companies started offering digital readers such as Amazon’s Kindle, Apple’s iBooks (accessible through iPads or iPhones), and of course, keeping up with the trend, Barnes and Noble’s NOOK.

Some readers prefer eBooks over hard copies because of its ease of access. Purchasing books can be done in the comfort of their own homes, and digital bookstores often have a larger selection of titles available.

eBook devices also allow for features like bookmarks, highlights, keyword search, annotations, and access through a centralized digital library.

That said, eBooks still haven’t outpaced the popularity of printed books, with print still commanding around 90% of the total revenues from U.S. book sales. It seems that people are still fond of having physical books as part of their collection.

This bodes well for Barnes and Noble, except for one, trillion-dollar obstacle: Amazon. Amazon has consistently dominated the eBook market in the 2010s, and has done a successful job of taking half of the print market share as well.

Facing tough competition, declining sales, and mass store closings, Barnes and Noble decided to spin off its college textbook business in 2015. The spin-off into what’s now Barnes and Noble Education (BNED) was seen as a smart move, enabling the company to focus on its strengths.

Barnes and Noble Education is one of the largest operators of physical and virtual bookstores for colleges and universities across the U.S. Under agreements made with these schools, the company has become the exclusive seller of both physical and digital course materials and supplies for these partner schools.

Barnes and Noble Education also offers direct-to-student services to help improve the academic performance of the students, such as:

- Student Brands – a subscription-based writing services business that provides students with study tools and assistance in writing, and even college applications

- bartleby – another subscription-based business that provides textbook solutions, expert question and answers, and writing and tutoring services

These businesses in particular have become more valuable in recent years as technology-based learning and online learning became norms following the pandemic. In FY 2021 alone, the company has seen 300,000 new subscribers for bartleby, a 70% growth over the prior fiscal year.

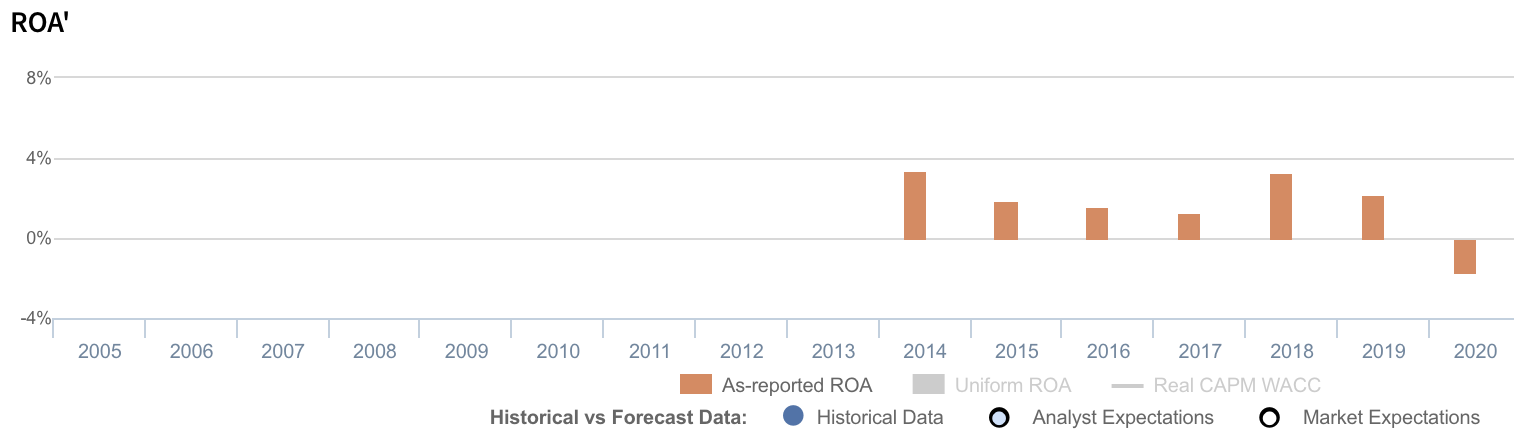

Barnes and Noble Education’s strong offerings on both digital and physical platforms, as well as its focus on the niche higher education market seems to be translating only to dull as-reported return on assets (ROAs) of -2% to 3%.

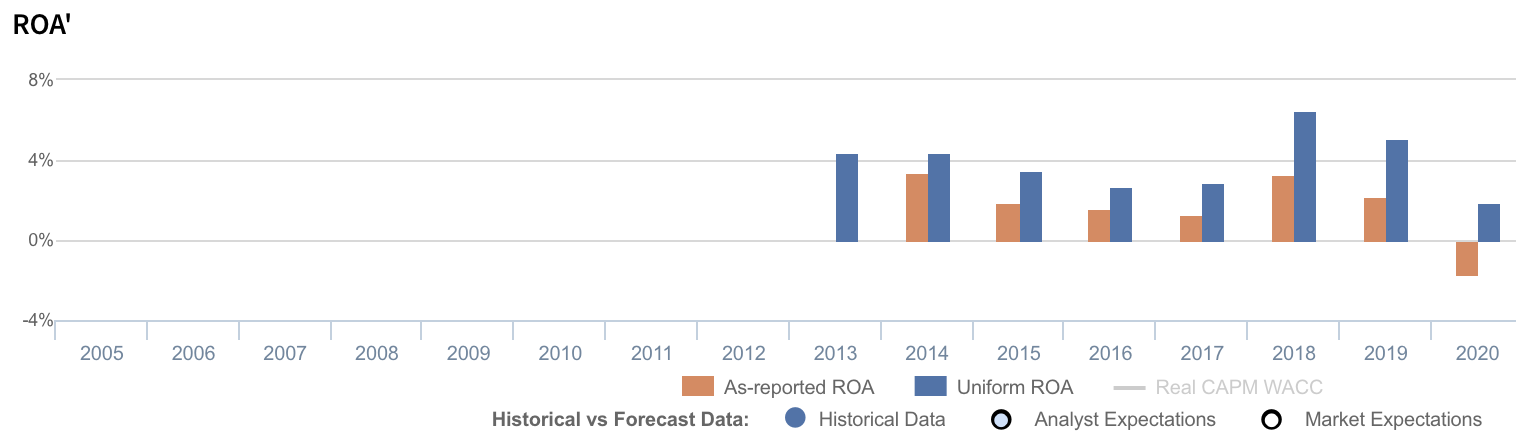

In reality, albeit still below cost of capital, Uniform Accounting reveals that returns have been at least twice as strong, with Uniform ROAs ranging from 2% to 7%.

The distortion comes from as-reported metrics failing to consider the number of operating leases Barnes and Noble Education has from their numerous existing retail stores.

The decision management makes between investing in capex and investing in a lease is based on how management wants to finance their investments. Choosing to lease an asset, however, would not be treated as an investment, but as an expense that would impact the income statement.

As a result, as-reported ROAs are not capturing the strength of Barnes and Noble Education’s earning power. Adjusting for operating leases, along with the other necessary adjustments Valens makes, we can see that the company isn’t actually displaying lackluster performance. In fact, returns have consistently been twice more than as-reported.

Barnes and Noble Education’s earning power is more robust than you think it is

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think the company is a much weaker business than real economic metrics highlight.

Barnes and Noble Education’s Uniform ROA has actually been higher than its as-reported ROA in the past three years. For example, Uniform ROA was at 2% in 2020 while as-reported ROA was at -2%.

Historically, Barnes and Noble Education’s as-reported ROA has ranged from -2% to 3% in the past seven years while Uniform ROA has ranged from 2% to 7% in the same timeframe.

After declining from 4% in 2013 to 3% in 2017, Uniform ROA rebounded to a high of 7% in 2018 before steadily declining to just 2% in 2020.

Barnes and Noble Education’s Uniform earnings margin have been slightly stronger than as-reported metrics recently, but Uniform asset turns have historically been weaker

Overall improvements in profitability have been driven by trends in Uniform earnings margin and, to a much lesser extent, Uniform asset turns.

Uniform margins fell from 4%-5% levels in 2013-2015 to 3% through 2017, before jumping to a peak of 7% in 2018. Uniform margins have since fallen to lows of 2% through 2020. Meanwhile, Uniform turns have sustained 0.8x-1.0x levels since 2013.

At current valuations, markets are pricing in expectations for both Uniform margins and Uniform turns to improve.

SUMMARY and Barnes and Noble Education, Inc. Tearsheet

As our Uniform Accounting tearsheet for Barnes and Noble Education, Inc. (BNED:USA) highlights, the Uniform P/E trades at 38.7x, which is above the global corporate average of 23.7x and its own historical P/E of 17.2x.

High P/Es require high EPS growth to sustain them. In the case of Barnes and Noble Education, the company has recently shown a 67% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Barnes and Noble Education’s Wall Street analyst-driven forecast is a 7% and 25% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Barnes and Noble Education’s $8.47 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 18% annually over the next three years. What Wall Street analysts expect for Barnes and Noble Education’s earnings growth is below what the current stock market valuation requires in 2021, but above that requirement in 2022.

Furthermore, the company’s earning power is below the long-run corporate average. Also, cash flows and cash on hand are below its total obligations—including debt maturities and capex maintenance. Together, this signals a high credit risk.

That said, Barnes and Noble Education’s Uniform earnings growth is above its peer averages, and the company is trading near average peer valuations.

About the Philippine Markets Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com