Uniform Accounting highlights how this utility company’s ROA is swimming above cost of capital levels

This water utility company created a well-diversified portfolio that enabled it to mitigate numerous risks amid the pandemic. However, its as-reported metrics understate the company’s strategy as its profitability continues to have no shareholder value.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Companies under the utilities sector are considered defensive stocks because of their relatively stable demand and earnings even through economic downturns. In turn, these companies have limited growth due to heavy regulations.

One of these companies is the Manila Water Company, a water utility company that serves the East Zone. This zone is a 1,400 square kilometers area that includes eastern side of Metro Manila (most parts of Quezon City, Makati City, Pasig City, etc.) as well as numerous towns in the Rizal province (Antipolo, Cainta, Taytay, etc.)

After successfully extending its franchise to operate until May 2037, Manila Water continues to earn profits while being consistent with the complied provisions as a public utility company.

One of its strategies is to continuously improve its services through its investments in capex projects.

From 2023 to 2027, Manila Water will be spending around PHP 181 billion in order to improve its water and wastewater projects and ensure water security.

As a result of climate change influencing water supply and demand, the company is set to use alternative sources of water for its customers, which will include the Wawa Calawis Water Supply, Sumag River, and Laguna Lake.

Furthermore, the company has other operations in the Philippines through its subsidiaries in the Manila Water Philippine Ventures, Inc (MWPV). These subsidiaries have different types of business such as the following:

| – | Bulk water supply businesses such as the Davao del Norte Water Infrastructure Company |

| – | Water distribution and used water services with the Boracay Island Water Company |

| – | Business-to-business water and wastewater service businesses like the Bulacan MWPV Development Corporation |

In addition, the company as a group also has a holding company for its international ventures, which include interests in Vietnam, Thailand, Indonesia, and Saudi Arabia.

Yet, despite the size and diversification of Manila Water, the company’s net income had an 18% decline in 2021.

With 79% of the company’s operating revenues from the sale of water, the decline of the company’s financial performance was driven by lower billed volume of water across the East Zone Concession and other travel destinations such as Boracay.

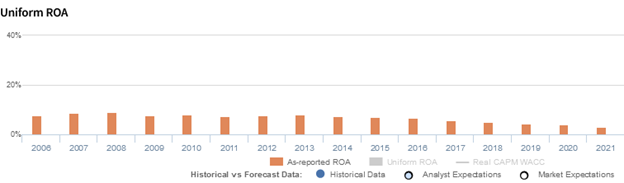

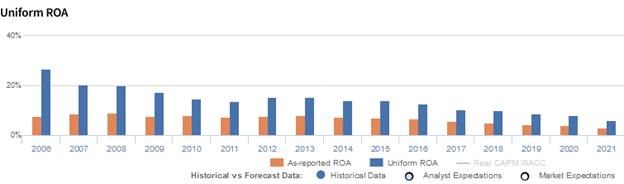

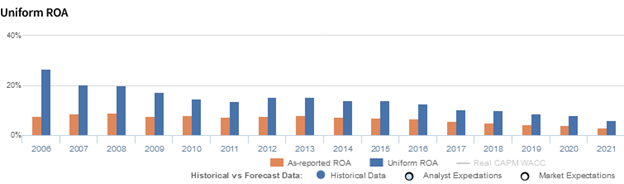

Looking at as-reported metrics, it appears that Manila Water Company’s returns continue to decline and produce below cost of capital levels, with return on assets (ROAs) reaching 3% in 2021.

In reality, the company’s financial performance is much better, with Uniform ROAs performing at 6%.

One of the said distortions stems from how Philippine Financial Reporting Standards (PFRS) classifies interest expense.

According to PFRS, interest expense is an operating cash flow. In reality, interest expense represents the cost of debt and is rightfully a financing cash flow. As such, in Uniform Accounting, interest expense is added back to earnings.

Specifically, in 2021, Manila Water Company recorded interest costs at PHP 2.5 billion. Adding back this expense because it is not an operating expense, along with many other necessary adjustments made by Valens, leads to a PHP 7.5 billion net income and a 6% Uniform ROA, higher than its PHP 3.7 billion as-reported net income and 3% as-reported ROA.

Manila Water Company’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that Manila Water Company’s profitability has been recently weaker than real economic metrics highlight.

Through Uniform Accounting, we can see that the company’s true ROAs have been understated over the past decade. For example, as-reported ROA was 3% in 2021, but its Uniform ROA was 2x higher at 6%.

Manila Water Company’s Uniform asset turns are stronger than you think

For more than two decades, as-reported metrics have understated Manila Water Company’s asset turns, a key driver of profitability.

Moreover, Uniform turns have already reached 0.4x. In comparison, as-reported turns have yet to eclipse beyond 0.3x. over the same time period, making the company appear to be a less efficient business than real economic metrics highlight.

SUMMARY and Manila Water Company, Inc. Tearsheet

As the Uniform Accounting tearsheet for Manila Water Company, Inc. (MWC:PHL) highlights, the company trades at a Uniform P/E of 10.7x, below the global corporate average of 18.4x, but around its historical P/E of 11.7x.

Low P/Es require low EPS growth to sustain them. In the case of Manila Water Company, the company has recently shown a 22% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Manila Water Company’s sell-side analyst-driven forecast is to see Uniform earnings shrinkage of 10% in 2022, and 27% growth in 2023.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Manila Water Company’s PHP 19.72 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 60% annually over the next three years. What sell-side analysts expect for Manila Water Company’s earnings growth is below what the current stock market valuation requires through 2023.

Moreover, the company’s earning power is above the long-run corporate average. However, cash flows and cash on hand are below total obligations—including debt maturities, capex maintenance, and dividends. Together, this moderate low credit risk.

To conclude, Manila Water Company’s Uniform earnings growth is below its peer averages, but in line with its average peer valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com