Uniform Accounting shows that this company’s strong culture of innovation is sticky enough for it to maintain robust 16% ROAs going forward

Innovation can be defined as creating a solution to a problem that has yet to exist.

This company’s ability to meet the needs their customers didn’t know they had allowed them to build a diversified product line through innovation and R&D.

While as-reported metrics may signal that this company’s massive investment in R&D may not have been fruitful, TRUE UAFRS-based (Uniform) analysis shows that this company has actually maintained robust 15%+ Uniform ROA levels in the past decade.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

The ability to create a solution for problems that consumers don’t even know they have is an indispensable skill in the world of business.

In 1968, Dr. Spencer Silver, a scientist at 3M, was attempting to develop an ultra-strong adhesive to be used for aircraft construction. Instead, he accidentally created a pressure-sensitive adhesive that could stick to any surface but can also be peeled without leaving any residue.

He tried to convince executives at the company that this adhesive was a solution to a problem that hasn’t existed yet. Ultimately, though, the higher-ups thought that the product was practically useless—his goal was to create a strong adhesive in the first place, not a weak one.

This adhesive wasn’t useful until a colleague came up with the idea of using this glue on the backs of paper. Thus, the Post-It was born.

Initially, sales of the Post-Its were a massive failure because nobody understood what it was for. After several more attempts and giving away free samples to companies, people finally saw its use and demand began to rise. Now, Post-Its are an iconic symbol for to-do lists.

However, even before Post-Its, 3M already had a myriad of successful products in its arsenal, most of which were born out of innovation to meet unmet and unknown needs.

The company already had Scotch tape (plus the snail dispenser), the first waterproof sandpaper, the Scotch-Brite sponge, the reflective tape on traffic cones, and other products targeted for the healthcare, safety and industrial, transportation and electronics, and the office supplies industry.

Although 3M’s competitors offered similar items, the company’s focus on bringing technological advantage to the table is what ultimately made their products more successful.

With a price-competitive industry such as theirs, the company knew that cost reduction through incremental operational changes wouldn’t cut it. Instead, they heavily invested into research and development to give them that value-over-price edge.

Furthermore, 3M patents all of their developed products to differentiate themselves from their competitors while also keeping their advantage. On average, the company is granted around 3,000 patents per year.

This focus on R&D did not only place them at a favorable competitive position, but also allowed them to pursue a diversification strategy.

3M expanded their product lines by developing and selling similar products—moving from making sandpaper to manufacturing grinding wheels and other abrasives, for example. The company also ventured into other business lines, establishing a total of six unrelated segments that sell items ranging from scissors to cleaning wipes to adhesives.

This strategy widened the company’s reach across several regions and markets, geographically expanding their business in more than 65 countries with over 8,000 scientists and researchers working internationally.

Additionally, because of their wide target market that spanned multiple industries, the company remained a profitable and stable business despite the cyclicality of some of their products.

To illustrate, global demand for their abrasives, sealants, and construction and electrical materials are down in the midst of the current pandemic, but is mitigated by the spike in sales for their N95 masks.

First created by the company in the 1970s, their N95 masks continue to boost their profitability as they ramp up production to supply the healthcare industry globally.

This shows how 3M’s continued focus on R&D and their diversification strategy have created robust returns for their business.

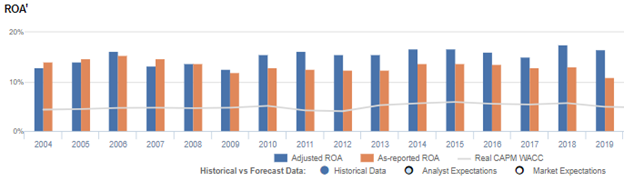

While as-reported ROAs are shown to be only at around 11%-14% levels from 2010-2019, in reality, Uniform ROAs have actually shown an improving trend from 16% to a peak of 18% in 2018, before falling slightly to 17% levels in 2019.

The distortion comes from as-reported metrics incorrectly treating R&D as an expense.

In reality, R&D is an investment in the long-term cash flow generation of the company. By recording R&D as an expense, this violates one of the core principles of accounting, which is that expenses should be recognized in the period when the related revenue is incurred.

Since as-reported accounting records R&D on the income statement, as opposed to as an investment on the balance sheet, net income can become materially understated.

As in the case of 3M, as-reported ROAs are not capturing the true strength of the company’s earning power. Adjusting for R&D, you get returns that are greater than what is actually shown. Without this adjustment, it will look like 3M is having less success with its R&D investments than it really is, leading to poorer valuations.

3M’s earning power is actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

3M’s Uniform ROA has actually been higher than its as-reported ROA in twelve of the past sixteen years. For example, as-reported ROA was 11% in 2019, significantly lower than its Uniform ROA of 17%. When Uniform ROA peaked at 18% in 2018, as-reported ROA was just at 13%.

Through Uniform Accounting, we can see that the company’s true ROAs have actually been higher. 3M’s Uniform ROA for the past sixteen years has ranged from 13% to 18%, while as-reported ROA ranged only from 11% to 15% in the same timeframe.

After falling from 16% in 2006 to 13% in 2009, Uniform ROA bounced back to 16% in 2011. Afterwards, Uniform ROA remained at 15%-16% levels through 2017 before rising to a peak of 18% in 2018. Uniform ROA then decreased to 17% in 2019.

3M’s margins are weaker than you think, but it is coupled with stability in Uniform asset turns

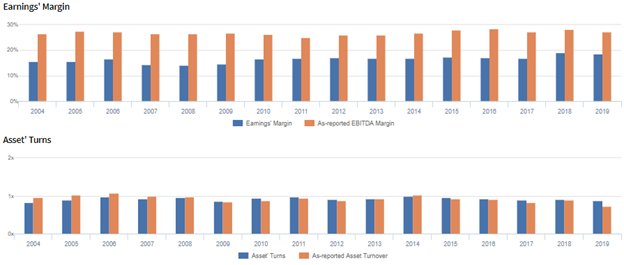

Trends in 3M’s Uniform ROA have largely been driven by trends in Uniform earnings margins, coupled with stability in Uniform asset turns.

From 2004-2006, Uniform earnings margins expanded from 16% to 17%, before fading to 14% in 2008. Thereafter, Uniform margins improved to 17% from 2010 through 2017 and increased further to 19% peaks in 2018-2019. Meanwhile, Uniform turns have been stable, ranging from 0.8x-1.0x levels.

At current valuations, markets are pricing in expectations for a slight Uniform margins regression, coupled with further stability in Uniform turns.

SUMMARY and 3M Tearsheet

As the Uniform Accounting tearsheet for 3M Company (MMM) highlights, the Uniform P/E trades at 21.8x, which is around corporate average valuation levels, but below its own recent history.

Low P/Es require low EPS growth to sustain them. In the case of 3M, the company has recently shown a 4% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, 3M’s Wall Street analyst-driven forecast is a 16% shrinkage in 2020, and a 12% growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify 3M’s $149 stock price. These are often referred to as market embedded expectations.

In order to justify current stock prices, the company would need to have Uniform earnings shrink by 1% each year over the next three years. What Wall Street analysts expect for 3M’s earnings growth is below what the current stock market valuation requires in 2020 but is above that requirement in 2021.

The company’s earning power is 3x the corporate average. Also, cash flows are higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, 3M’s Uniform earnings growth is below peer averages in 2020. Also, the company is trading above average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com