Uniform Accounting uncovers the true value of this beauty company’s luxury strategy, with returns that have actually gone up to a record high of 28%

Marketing a product to target high-end consumers enables firms to command a higher pricing power by leveraging premium features or even just the brand name itself.

This beauty company follows this luxury strategy and has done so successfully. To complement this, the company has also made several brand acquisitions and licensing agreements to increase market share and revenue streams.

While declining as-reported returns make it seem like consumers are no longer seeing the value of luxury products, Uniform Accounting reveals the opposite.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

The beauty industry has become a $500 billion market and is set to grow even further as digital marketing trends and consumer behavior continue to evolve with the industry.

To keep up with the rapid changes, some of the biggest beauty companies are continuously investing in developing strategies to grab market share. The Estée Lauder Companies Inc. (EL), the third-largest beauty company in the world, is one of these companies.

Taking the name of its maker, the company was launched in 1946 with only four products sold to the market—a Cleansing Oil, Skin Lotion, Super Rich All Purpose Crème, and Crème Pack.

In what might seem to be a bold marketing move for a start-up, Estée insisted that her products be sold only in high-end department stores, which was not an easy feat.

She set up many unsuccessful negotiations with Robert Fisk, the cosmetics buyer at Saks Fifth Avenue, to put her products on his shelves. When Fisk finally agreed, within two days of putting these on sale, the entire stock sold out.

The company’s successful business transaction with Saks made Estée more confident in the company’s ability to expand store locations and continue pursuing a luxury brand strategy. Thereafter, she was able to make deals with other luxury department stores like Neiman Marcus, Harrod’s, and Galeries Lafayette.

By associating itself with high-end consumers, Estée Lauder was able to command a premium price by simply tagging itself as a luxury brand. However, relying on that strategy wasn’t enough. Estée knew that if she wanted to beat the other beauty giants, she had to think bigger.

The company made several strategic brand acquisitions and licensing agreements to expand their product portfolio and their industry footprint.

Some of the deals included were with fashion designers Tommy Hilfiger, Kiton, and Donna Karan. On top of that, the company also made several acquisitions of high-end make-up brands over the years, including M.A.C. Cosmetics, La Mer, and Bobbi Brown.

Furthermore, in 2014, the company went into an “acquisition spree” and made four big acquisitions in a span of only three months: RODIN olio lusso, Le Labo, Editions de Parfums Frédéric Malle, and GLAMGLOW.

Historically, this acquisition and licensing strategy has been advantageous for businesses in the industry. It increases revenue potential at low investment costs, particularly for licensing agreements, making access to foreign markets easier and increasing market share.

Given Estée Lauder’s focus on continuous expansion to create more revenue streams and their ability to command higher pricing power by being a luxury brand, it would be reasonable to expect robust, increasing returns.

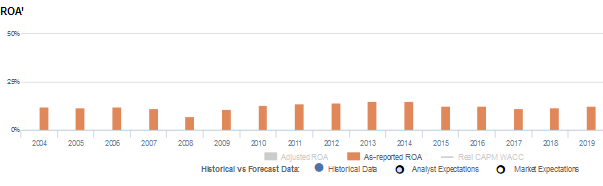

However, looking at as-reported metrics, it seems that its marketing and expansion strategies have not translated to improving returns. In fact, as-reported ROAs have declined from peak 15% levels down to 11%-13%.

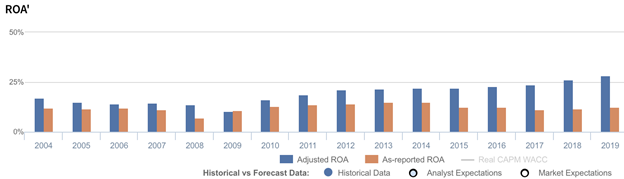

In reality, Estée Lauder’s strategic acquisitions in the luxury space have generated value for the firm and are why returns have gone up to record highs.

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of goodwill on Estée Lauder’s balance sheet. The company’s goodwill sits at about $1.2 billion to $1.9 billion in recent years, due to the aforementioned acquisitions and other acquisitions over the course of its operations.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of Estée Lauder’s earning power. Adjusting for goodwill, we can see that the company isn’t actually performing consistently poorly. In fact, it is the opposite, with returns that are nearly 2x greater.

Estée Lauder’s earning power is actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

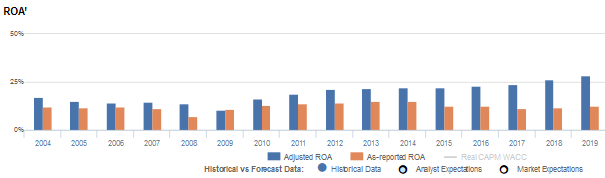

Estée Lauder’s Uniform ROA has actually been higher than its as-reported ROA in fifteen of the past sixteen years. For example, as-reported ROA was 13% in 2019, but its Uniform ROA was actually more than 2x higher at 28%.

Furthermore, Estée Lauder’s Uniform ROA has ranged from 11% to 28% in the past sixteen years while as-reported ROA ranged only from 7% to 15% in the same time frame.

After falling from 17% in 2004 to a low of 11% in 2009, Uniform ROA gradually increased to a peak of 28% in 2019.

Estée Lauder’s Uniform earnings margins are weaker than you think, but its robust Uniform asset turns make up for it

Estée Lauder’s profitability has been driven by improving Uniform earnings margins, coupled with stability in Uniform asset turns.

From 2004-2009, Uniform earnings margins declined from 8% to 6%, before steadily expanding to 15% in 2019.

Meanwhile, Uniform turns fell from 2.0x-2.1x levels in 2004-2006 to 1.7x-1.8x levels in 2008-2009 and remained there through 2018. Thereafter, Uniform turns improved to 1.9x in 2019.

At current valuations, markets are pricing in an expectation for both Uniform margins and Uniform turns to reach new peaks.

SUMMARY and Estée Lauder Tearsheet

As the Uniform Accounting tearsheet for the Estée Lauder Companies Inc. (EL) highlights, its Uniform P/E trades at 39.3x, which is above corporate average valuation levels and its own recent history.

High P/Es require high EPS growth to sustain them. In the case of Estée Lauder, the company has recently shown a 18% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Estée Lauder’s Wall Street analyst-driven forecast is a 39% EPS shrinkage in 2020 and a 57% EPS growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Estée Lauder’s $198 stock price. These are often referred to as market embedded expectations.

The company needs Uniform earnings to grow 11% each year over the next three years to justify current prices. What Wall Street analysts expect for Estée Lauder’s earnings growth is below what the current stock market valuation requires in 2020, but is above its requirement in 2021.

Furthermore, the company’s earning power is 5x the corporate average. Also, cash flows are 3x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low credit and dividend risk.

To conclude, Estée Lauder’s Uniform earnings growth below its peer averages in 2020, but the company is trading far above average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com