Uniform ROAs of 30%+ show how this company shines bright as a “pickaxe seller” in the solar panel industry

Humans have long known how to harness natural energy, using wind to push their sails and the sun to create fire. That said, modern technology has grown a lot more complicated than just sails and bonfires, and we need more advanced devices to efficiently collect renewable energy.

One of the most common and more accessible energy generation devices are solar panels. But while most companies are competing to sell the panels themselves, this company decided to become the “pickaxe seller” and sell the product that makes solar panels usable and more efficient.

While as-reported return on assets (ROAs) show how this decision has only led to lackluster returns, Uniform Accounting uncovers the company’s real returns, with Uniform ROAs that are actually 3x-5x stronger.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

Just over the past year, we’ve experienced some of the worst global weather events of this century. We’ve seen record-breaking floods, storms, heatwaves, and blizzards from across the globe—if it wasn’t clear enough, climate change is very much a real concern.

Global temperatures have been increasing at an alarming rate all thanks to the burning of fossil fuels such as oil and coal for power, heat, and transportation purposes.

This is why governments are making it a point to switch from fossil fuels to renewable energy.

In the U.S., for example, the Biden administration is aiming to pass laws that require utility companies to source more power from renewable energy sources. This is in line with its commitment to reduce greenhouse gases by half by 2030 and decarbonize the U.S. power sector by 2035.

Renewable energy usage has steadily increased over the past decade. We’ve seen large scale utilization of renewable energy sources from industrial wind farms to hydroelectric dams.

But innovation has lowered the cost of production, which makes it more accessible to the masses. With that, we’re also starting to see small scale expansion in the form of residential rooftop solar panels.

Solar power sounds great. It’s sold as “free electricity” once you install the system. However, it can also be inefficient.

In the traditional PV solar power model, the system is made up of a bunch of PV modules—those black screens you see on the roofs of houses. These PV modules make direct-current (DC) power when light shines on them. From there, DC power is sent to an inverter, which converts it to alternating-current (AC) power. This is what’s used to power homes.

The inefficiency comes from the second step, where the DC power is converted to usable AC power at the inverter.

SolarEdge (SEDG) solves this problem.

It doesn’t try to make better black screens for your roof, which is a highly competitive, fragmented industry. Tons of companies, like SolarCity, are trying to make more efficient panels and are battling for market share. Because of that, it’s a cutthroat market with thin margins.

Instead, SolarEdge makes it easier for panels to deliver usable electricity. The company manufactures power optimizers, which make each panel in a system more efficient and a better inverter. That helps DC electricity become AC electricity more easily.

This makes SolarEdge a “pickaxe seller” in the solar power industry because it doesn’t matter which solar panel you buy, you’re going to have to buy the inverter anyway to make it usable.

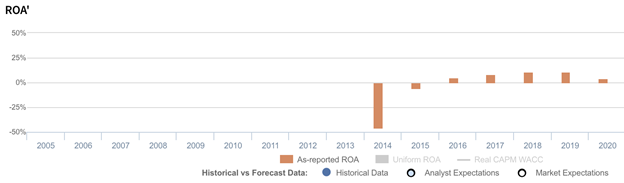

Like we’ve talked about before, pickaxe sellers in trending industries—renewable energy, for example—tend to earn great returns. However, SolarEdge’s as-reported return on assets (ROAs) doesn’t seem to show that.

Returns have only ranged from 4%-11% over the last five years—not weak, but also not great.

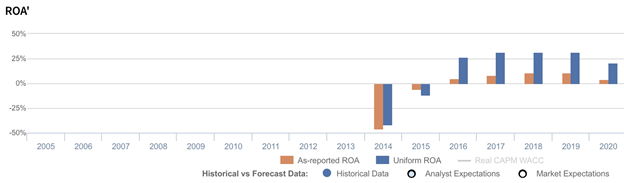

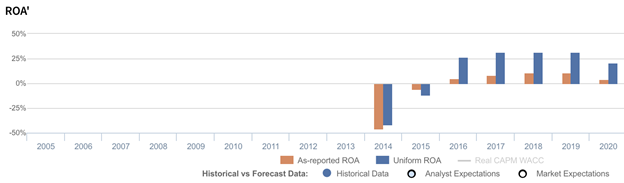

Uniform Accounting, on the other hand, reveals the strength of SolarEdge’s profitability more accurately, showing Uniform ROAs ranging from 21%-32% over the same timeframe.

What as-reported metrics fail to do is to consider excess cash on the balance sheet. While most companies inherently need some level of cash to operate, the portion of that balance that is earning limited or no return—or excess cash—ends up diluting as-reported ROAs.

The purpose of removing excess cash is to see what the true operating ROA of the firm is. Removing excess cash allows investors to see through the distortions that come from management carrying much more cash on the balance sheet than what is operationally required.

In the case of SolarEdge, the company has a substantial cash balance amounting to roughly $1 billion, about half its total assets. Having too much cash on the books inflates the asset base and causes profitability to look weaker than it really is.

Adjusting for excess cash, we can see that SolarEdge’s Uniform ROAs are actually 3x-5x higher than as-reported ROAs.

SolarEdge’s earning power is significantly more robust than you think it is

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think the company is a much weaker business than real economic metrics highlight.

SolarEdge’s Uniform ROA has actually been higher than its as-reported ROA in the past seven years. For example, Uniform ROA was at 21% in 2020 while as-reported ROA was at 4%.

Historically, SolarEdge’s as-reported ROA has ranged from -46% to 11% in the past seven years while Uniform ROA has ranged from -42% to 31% in the same timeframe.

As a provider of power optimizers and inverters in the rapidly growing solar energy market, SolarEdge has historically seen improving profitability. Since 2014, Uniform ROA has steadily expanded from a low of -42% to a peak of 31%-32% in 2017-2019. Thereafter, Uniform ROA compressed to 21% in 2020.

SolarEdge’s Uniform earnings margin is weaker than you think, but its Uniform asset turns make up for it

Uniform ROA expansion has been driven by improving Uniform earnings margins, slightly offset by declining Uniform asset turns.

Since 2014, Uniform margins have steadily improved from -15% in 2014 to 15% in 2020. Meanwhile, Uniform turns have declined from 2.9x highs in 2014-2015 to 1.4x in 2020.

At current valuations, the market is pricing in expectations for both Uniform margins and Uniform turns to improve.

SUMMARY and SolarEdge Technologies, Inc. Tearsheet

As the Uniform Accounting tearsheet for SolarEdge Technologies, Inc. (SEDG:USA) highlights, the Uniform P/E trades at 44.7x, which is above the global corporate average of 23.7x and its own historical P/E of 33.0x.

High P/Es require high EPS growth to sustain them. In the case of SolarEdge, the company has recently shown a 16% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, SolarEdge Wall Street analyst-driven forecast is a 17% and 38% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify SolarEdge’s $249 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 26% annually over the next three years. What Wall Street analysts expect for SolarEdge’s earnings growth is below what the current stock market valuation requires in 2021, but above that requirement in 2022.

Furthermore, the company’s earning power is 3x the long-run corporate average. Also, cash flows and cash on hand are above its total obligations—including debt maturities and capex maintenance. Together, this signals low credit risk.

That said, SolarEdge’s Uniform earnings growth is below its peer averages. However, the company is trading above peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com