Venturing into leisure gaming helped this real estate developer win a Uniform ROA of 16%, not cost-of-capital returns that as-reported metrics suggest

This property developer shifted its focus in the real estate business and ventured into casino and gaming to take advantage of the growing market.

By adding gaming to its portfolio, the company has seen improvements in its Uniform ROA in recent years. However, as-reported consistently show weak returns.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Gambling had already established itself in the Philippines as early as the sixteenth century. However, there were no exact records on when it actually started. Some say it was initiated by the Chinese since the two countries were in close proximity.

As centuries went by, gambling developed from betting on cock fights and horse races to card games and casinos. Eventually, the rapid proliferation of illegal gambling such as Jueteng and Masiao led the government to intervene by establishing the Philippine Amusement and Gaming Corporation (PAGCOR) through a Presidential Decree in 1969.

The Philippine casino and gaming market has been on the rise ever since. One significant contributor to this growth is the amendment of constitutional restrictions on foreign ownership in 2010, making gambling casinos open to majority foreign equity ownership in the Foreign Investment Negative List (FINL).

Since then, the Philippine casino and gaming market has become one of the biggest in the region. The market has expanded at a robust pace, with a gross gaming revenue (GGR) CAGR of 14.87% from PHP 62.13 billion in 2010 to PHP 248.5 billion in 2019.

The growing gambling and gaming market has made PAGCOR the largest contributor of revenue to the government. In February 2020, PAGCOR reported that GGR hit PHP 248.5 billion in 2019, which is a 15.1% improvement over 2018 and nearly 41% higher than 2017.

Most of the Philippine government’s total GGR every year comes from Manila’s Entertainment City, the home of the four famous integrated casino resorts: Resorts World, Okada Manila, Solaire, and City of Dreams.

Today’s company is one of the owners and the developer of famous casino resorts, specifically City of Dreams.

Formerly an oil and exploration company, Belle Corporation (BEL:PHL) took on a new direction by shifting its business to property development.

The company became known in the early ‘90s up to the early 2000s for developing the once barren mountains of Tagaytay into one of the premium mountain resort destinations, Tagaytay Highlands. This premium residential project covers three provinces—Batangas, Cavite, and Laguna—and also includes a portfolio of assets, namely Golf and Country Clubs, Highlands Homes, Midlands Homes, and Greenlands Homes.

Though the real estate business was already a profitable one, the company decided to venture into the gaming industry to further diversify its business. In 2010, Belle Corporation acquired Premium Leisure & Amusement, Inc. (PLAI), a grantee by the PAGCOR of a license to operate integrated resorts and casinos.

To strengthen its position in the industry, the company, together with PLAI, decided to enter into a partnership agreement with Melco Resorts and Entertainment in 2012, where Belle Corporation contributed land and property for the venture that Melco will operate.

Three years later, City of Dreams Manila was launched and it became one of the most popular tourist resorts in the Entertainment City.

Now, most of Belle Corporation’s revenues come from City of Dreams’ lease and gaming income, which constitutes around 75% of the total revenue for the fiscal year 2019.

From 2013 to 2018, Belle Corporation’s revenue grew at an average of 79% thanks to the country’s increasing international tourist arrivals, with holiday and leisure being the highest percentage in terms of purpose of visits.

However, when the pandemic forced the Philippines to implement one of the longest lockdowns in the world, the country’s tourism business suffered, taking the gaming industry with it.

With casinos closed because of the pandemic, Belle Corporation is able to weather this storm mainly by depending on the lease income on their agreement with Melco and their exclusive golf and country clubs.

Now that the government has started to relax its community quarantine and with tourism gradually reopening, Belle Corporation is starting to recover.

From being a niche company in the real estate industry to becoming one of the most successful conglomerates in the tourism and gaming industries, Belle Corporation was able to make a name for itself by securing diversification opportunities that could help drive its overall growth.

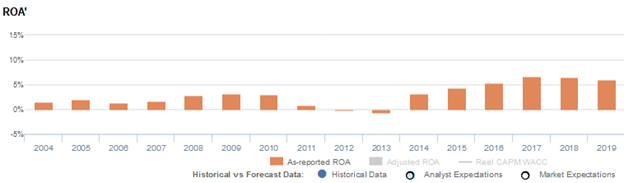

However, as-reported metrics show that focusing on its diversification strategy hasn’t been that rewarding for the developer, with return on assets (ROAs) only reaching a peak of 7% in the past six years.

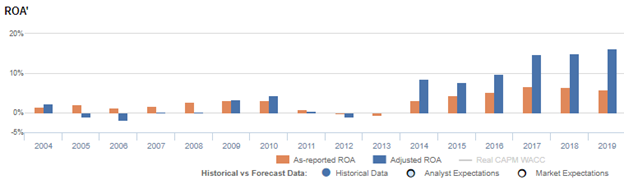

In reality, Belle’s highly diverse portfolio has led to strong, improving Uniform returns of more than 16%.

One of the said distortions stems from how Philippine Financial Reporting Standards (PFRS) classifies interest expense.

According to PFRS, interest expense is an operating cash flow, but in reality, interest expense represents the cost of debt and is actually a financing cash flow. As such, in Uniform Accounting, interest expense is rightfully added back to earnings.

When we add the PHP 479 million interest expense back to earnings, along with many necessary adjustments, Uniform ROA increases to 16%, far higher than the company’s as-reported ROA of 6%.

Belle Corporation’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think Belle Corporation’s profitability has been weaker than real economic metrics have highlighted in nine of the past sixteen years.

In reality, Belle Corporation’s true profitability has been higher than as-reported ROA in most years. Specifically, Uniform ROA was 16% in 2019, significantly lower than as-reported ROA of 6%.

After ranging from -2% to 4% levels in 2004-2013, Uniform ROA expanded to 10% in 2014, before declining to 9% in 2015. Thereafter, Uniform ROA gradually improved to 16% in 2019.

In contrast, after ranging from -1% to 3% in 2004-2014, as-reported ROA slowly increased to 7% levels in 2017-2018, before compressing to 6% in 2019.

Belle Corporation’s earnings margin is weaker than you think

Trends in Uniform ROA have been primarily driven by trends in Uniform earnings margin.

As-reported margins contracted from 48% in 2004 to 35% in 2006, before expanding to 44% levels in 2010. It then declined to its lowest levels at -64% in 2013, before recovering to 61%-69% levels in 2014-2019.

Meanwhile, Uniform margins declined from a 18% in 2004 to a low of -76% in 2006, before improving back to 30% in 2010. However, Uniform margins dipped again to -39% in 2012 and then rebounded to 37%-76% levels in 2014-2019.

Looking at the firm’s margins alone, as-reported metrics are making the firm appear to be a more cost efficient business than is accurate.

SUMMARY and Belle Corporation Tearsheet

As the Uniform Accounting tearsheet for Belle Corporation (BEL:PHL) highlights, it trades at a Uniform P/E of 17.2x, below the global corporate average of 25.2x, but above its historical average of 14.9x.

Low P/Es require low EPS growth to sustain them. In the case of Belle Corporation, the company has recently shown a 30% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Belle Corporation’s sell-side analyst-driven forecast calls for an 82% Uniform EPS decline in 2020 followed by a 2% Uniform EPS growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Belle Corporation’s PHP 1.68 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 32% each year over the next three years and still justify current valuations. What sell-side analysts expect for Belle Corporation’s earnings growth is below what the current stock market valuation requires in 2020, but above its requirement in 2021.

Furthermore, the company’s earning power is almost 3x the long-run corporate average, but cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a high credit and dividend risk.

To conclude, Belle Corporation’s Uniform earnings growth is below peer averages, but the company is trading in line with peer average valuations.

About the Philippine Markets Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!.

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com