With a TRUE earning power of 16%, can this company cool off consumers and concerned investors at the same time?

According to PAGASA, the past few days have been some of the hottest days so far in 2020. PAGASA even expects such levels to continue throughout the rest of May.

This company is benefiting from the rising temperatures, especially in major cities in the Philippines. Its consistently robust UAFRS-based (Uniform) profitability reflects how essential its products have become to Filipinos.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippines-listed Focus

Powered by Valens Research

Electric air conditioning as we know it today was originally intended for a different purpose.

In 1902, American engineer Willis Carrier created the first electrical air conditioning unit to prevent pages from wrinkling at a printing plant.

Seeing how this invention could benefit residences and other industries, he soon started his own company, Carrier Engineering Corporation.

Known today as Carrier Global Corporation (CARR:USA), it is still one of the largest air conditioning companies in the world.

However, it took some time for the appliance to achieve widespread use. High manufacturing costs and its complex technology made air conditioning units a luxury of the rich.

Especially in the Philippines, where only a handful can afford air conditioning at home despite the need to combat the warm climate. As such, the market for air conditioning developed sluggishly during the early 20th century.

It took a couple of decades and further technological advancements before the industry was lucrative enough for businesses to enter.

In 1962, Concepcion Industrial Corporation (CIC:PHL) was incorporated to test the Philippine air conditioning market.

In their first year, the company negotiated an exclusive license to distribute Carrier products in the Philippines.

With an already established global brand, the business found success. In 1977, the company added another licensed brand to their portfolio with Kelvinator.

It was only in 1987 when it finally launched its own brand, Condura. In total, it took the company 25 years to build its expertise, grow its customer base to a sizable number, and start its own air conditioning production.

While it took some time for them to grow, their long-term strategy did pay off.

Today, the firm is the largest provider of air conditioning in the country and has since expanded its product lineup to include a wider range of appliances, dominating the refrigerator business as well.

More importantly, demand for air conditioning is growing fast. The International Energy Agency predicts global air conditioning demand to triple by 2050, as the income of emerging economies continues to rise.

Realizing these favorable tailwinds early on, Concepcion Industrial went public in 2013 to grow the export side of the business. It aimed to have its revenues be equally composed of local and export sales.

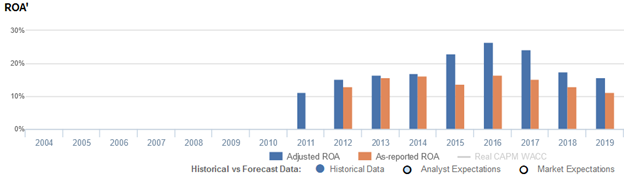

However, as-reported data suggests that the company has performed worse since its IPO, with as-reported ROA falling from 16% in 2014 to just 11% in 2019.

With Uniform Accounting, we see a completely different trend. In reality, the company has not performed worse, with 2019 Uniform earning power of 16% near 2014 levels of 17%.

Much of the difference between as-reported and Uniform accounting lies in how the minority interest or the non-controlling ownership of subsidiaries is treated.

As a form of equity, minority interest occurs when companies other than the parent company gain less than 50% ownership of a subsidiary, in exchange for capital.

As such, any transaction that takes place related to non-controlling interest is a financing cash flow and is not part of the core operations of the business. Therefore, minority interest expense is added back to earnings.

In 2019, the company’s minority interest expense of PHP 483 million is equal to half of as-reported net income of PHP 947 million. Adding this back and with the many other adjustments Valens makes, we arrive at the firm’s TRUE earnings of PHP 1.5 billion and Uniform earning power of 16%.

Concepcion Industrial’s earning power is stronger than you think

Through Uniform Accounting, we see that as-reported metrics significantly distort the firm’s profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than what real economic metrics reveal.

Uniform ROA has actually been higher than as-reported ROA for the past eight years. In 2019, Uniform ROA was 16%, significantly higher than as-reported ROA of 11%.

The company’s Uniform ROA steadily rose from 15% in 2012 to a peak of 26% in 2016, before fading to 16% in 2019.

Meanwhile, as-reported ROA only improved from 13% in 2012 to 17% in 2014, before dipping to 14% in 2015. While as-reported ROA did recover to 16% in 2016, it has since faded to just 11% in 2019.

Concepcion Industrial is a more efficient business than you think

Similarly, as-reported metrics significantly distort the firm’s asset efficiency, a key driver of profitability.

In 2019, as-reported asset turnover was 1.2x compared to Uniform asset turns of 1.6x, making the company appear to be a less efficient business than real economic metrics highlight.

Moreover, as-reported asset turnover has been lower than Uniform turns each year for the past six years, distorting the market’s perception of the firm’s historical asset efficiency level.

SUMMARY and Concepcion Industrial Corporation Tearsheet

As our Uniform Accounting tearsheet for Concepcion Industrial highlights, Uniform P/E currently trades at 8.5x, which is far below the market average and the company’s historical average.

Low P/Es require low EPS growth to sustain them. In the case of Concepcion Industrial, the company has recently shown a 4% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, Concepcion Industrial’s sell-side analyst-driven forecast calls for 9% Uniform earnings growth in 2020, followed by 13% Uniform earnings growth in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify PHP 23.40 per share. These are often referred to as market embedded expectations.

The company’s Uniform earnings could shrink by about 15% in each of the next three years and it will still meet current market valuations.

What sell-side analysts expect for the company’s earnings growth is far above what the current stock market valuation requires.

In addition, the company’s earning power is 3x the corporate average, and the company has low dividend risk, with cash flow and cash on hand materially above their debt obligations within the next five years.

To conclude, Concepcion Industrial’s Uniform earnings growth is near peer averages in 2020, but the company is trading below peer average valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com