With an immaterial Uniform earnings margin, this company might not yet be ready to go and ship meaningful returns

Business tailwinds play an important part in analyzing a company’s future performance. Also, it is equally important to consider the company’s ability to capitalize on its tailwinds.

This shipping company is expected to reach record-high profitability, driven by its increasingly important industry. That said, its past performance shows how it has been unable to take advantage of industry tailwinds, which Uniform Accounting is able to explain more clearly.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

The logistics industry is one of the few industries that have been unhampered by the COVID-19 pandemic. People realized early that maintaining the flow of goods open is essential to keep the economy going.

In some ways, the industry has been boosted by the current environment with the boom in e-commerce. Last month’s article mentioned how LBC Express Holdings, Inc. (LBC:PHL) is benefiting from the e-commerce tailwind, with the introduction of their cash on delivery and cash on pick-up services.

One might find it safe to assume that other logistics companies are benefiting from similar trends. In reality, not everyone will be well-equipped to take advantage of industry tailwinds while mitigating industry headwinds.

2GO Group, Inc. (2GO:PHL) is one of the main players in the logistics market, specializing in the shipping side of the industry. Market expectations are implying that the firm’s profitability will reach new peaks in the next couple of years.

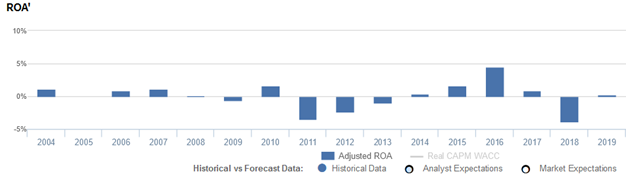

However, 2GO Group has yet to prove it can generate economic value. Looking at its historical Uniform ROA performance, the company has failed each year to exceed the 6% global cost of capital.

2GO Group’s muted profitability is partially due to its revenue mix. Aside from providing freight and logistic services, it also offers passenger transportation and ferries under the 2GO Travel business.

The company’s exposure to the tourism industry has made itself susceptible to cyclical fluctuations, including the current COVID-19 pandemic. In fact, the firm attributes its net loss so far in 2020 to its significantly lower travel revenue, as a result of the ongoing travel restrictions.

Another reason for 2GO Group’s weak profitability has been its failure to manage costs. Heavy net losses in 2011 and 2018 were driven by high fuel expenses for their vessel fleet.

Coupled with intense competition and freight pricing being externally set by the Philippine Liner Shipping Association (PLSA), 2GO Group’s Uniform earnings margins have been as volatile as its Uniform ROA.

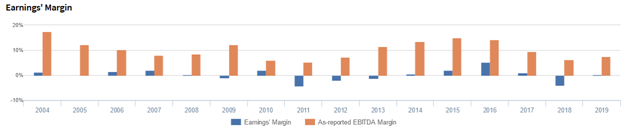

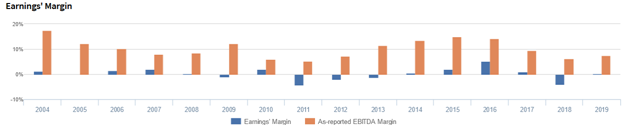

However, the as-reported metrics are showing the company to be more cost-efficient than in reality. In 2019, as-reported EBITDA margin was 8%, while Uniform earnings margin was actually immaterial.

One of the main factors bloating the company’s earnings is how the Philippine Financial Reporting Standards (PFRS) treats depreciation.

In one of our past articles, we’ve talked about the distortion caused by failing to adjust Property, Plant, and Equipment (PP&E) for inflation. Allowing the distortion materially understates the firm’s fixed assets over time and, in doing so, similarly understates the depreciation a company charges on the income statement.

When adjusting PP&E for inflation, 2GO Group has actually been recognizing PHP 2.4 billion less in fixed assets. This, in turn, has led the firm to charge PHP 274 million less in depreciation expenses, making it appear more profitable than it really is.

By applying this adjustment together with other necessary adjustments that Valens makes, we arrive at 2GO Group’s TRUE earnings margin of 0.2% in 2019, not 7.5%.

2GO Group’s recent earning power is weaker than you think

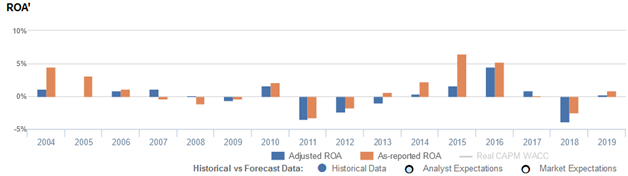

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much stronger business than real economic metrics highlight.

2GO Group’s Uniform ROA has actually been lower than its as-reported ROA in thirteen of the past sixteen years. Most recently, as-reported ROA was 1% in 2019, but Uniform ROA shows profitability to be actually immaterial.

Through Uniform Accounting, we can see that the company has maintained below 6% cost-of-capital ROAs since 2004, ranging from -4% to 5%.

2GO Group’s margins are weaker than you think

2GO Group’s muted profitability has been driven primarily by weak earnings margins, a key driver of profitability.

In the past sixteen years, Uniform earnings margin has fallen to as low as -4% and has never exceeded 5%. Meanwhile, as-reported EBITDA margin has never fallen below 5%, reaching as high as 18%.

As-reported metrics have been making the firm appear to be a more cost-efficient business than real economic metrics show.

SUMMARY and 2GO Group, Inc. Tearsheet

As the Uniform Accounting tearsheet for 2GO Group highlights, the Uniform P/E trades at -75.0x, which is well below corporate average valuation levels and its own history.

Negative P/Es implies negative EPS growth. In the case of 2GO Group, the company has recently shown a 74% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, 2GO Group’s sell-side analyst-driven forecast calls for a 176% Uniform EPS growth in 2020 followed by a 1% decline in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify 2GO Group’s PHP 8.44 stock price. These are often referred to as market embedded expectations.

The company needs its EPS to grow by 99% each year over the next three years to justify current valuations. What sell-side analysts expect for 2GO Group’s earnings growth is above what the current stock market valuation requires in 2020, but below in 2021.

Furthermore, the company’s earning power is below the long-run corporate average. Additionally, cash flows and cash on hand will be below its total obligations starting 2021—including debt maturities, capex maintenance, and dividends. Together, this signals high credit and dividend risk.

To conclude, 2GO Group’s Uniform earnings growth is well above peer averages in 2020, and the company is trading well below its peer average valuations.

About the Philippine Markets Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com