With its commitment to innovation and technology, this tech giant has shown Uniform ROAs of 25%+ levels

India is one of the most in-demand countries for IT and outsourcing services around the globe. This Indian company is benefiting from this trend, and is reflected in the company’s as-reported return on assets (ROA), which are currently at double the cost of capital.

Though at current levels, the firm’s returns are relatively decent, Uniform Accounting shows the company’s strategic business model partnerships actually merit a much more robust profitability.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

Two of the most in-demand services in the technology services space are IT services and Business Process Outsourcing (BPO).

IT services refers to any services offered by a company to automate a business process, capable of executing the needs of the hiring company. An example of these services are cloud services, IT consulting, network security, data management, among others.

Business Process Outsourcing is a practice where a company hires another company to do a specific function, which is essential for the hiring company’s operations. The hired company is responsible for the completion of work related to the assigned business function.

There are a few countries that are well-known hubs for these business practices—the most popular one is India.

India’s global sourcing and IT services market is the biggest around the world, and still growing. In fact, the majority of international companies are sourcing their needs in the Indian IT industry, accounting for 55% of the global service sourcing market in 2019-20.

The country’s location attractiveness as an IT service and BPO provider comes from its large pool of highly-skilled workers and low cost of labor. Moreover, according to a research by National Association of Software Services and Companies (NASSCOM), factors such as IT companies’ quality orientation, 24/7 service, and the country’s investor-friendly tax structure are some of the other reasons why India has become a popular IT and BPO choice.

India’s government has also taken advantage of this technological growth through its Digital India campaign, which aims to make the government’s services digitally available to its citizens through improvement of infrastructure and enhancement of internet connection. Through this, the country’s digital population massively increased, further making it an attractive spot for IT and outsourcing services.

One company that is taking advantage of the country’s location attractiveness is Infosys Limited.

Infosys, established in 1981 by seven engineers and a $250 beginning capital, has gotten to where it is today through its wide range of end-to-end services in IT consulting, business consulting, and business process management.

From its humble beginnings as it started operations in India, Infosys has branched out and established its international offices around the globe. The company currently has operations in the Americas, Asia Pacific, Europe, Middle East, and Africa.

With this worldwide reach, the company was able to pioneer the global delivery model (GDM) which enables them to provide 24/7 services by using their workforce around the globe. This model makes sense for a BPO company like Infosys because it allows them to quickly provide solutions to their clients at any time, leading to increased customer satisfaction. As a result, the company’s brand reputation increased, leading to even more customers.

Infosys also continues to expand its innovative capabilities through partnerships and alliances with major technology companies such as Oracle and Microsoft as well as through investments in startup companies like Trifacta and TidalScale.

Its commitment to innovation does not end there. The company implemented its Zero Distance program, which aims to further innovate and improve the company’s current projects by asking its employees to come up with creative ideas for project solutions.

Additionally, Infosys also implemented the Zero Bench program, which aims to utilize its employees on bench by keeping them involved by asking them to generate innovative solutions and offerings for clients.

Both Zero Distance and Zero Bench programs help the company boost customer satisfaction and win more clients, with its innovative solutions.

Moreover, the company has been strategically applying the “Renew New” program, which comprises the company’s initiative to restructure its customer-base functions, to streamline its sales, and to unify its delivery system.

In line with this program is the Aikido service offerings, which focuses on the optimization of the client’s business through knowledge-based services and design-thinking initiatives as well as the development of AI platforms to assist clients in identifying future business growth opportunities.

Infosys’ dedication to innovation and its investment in technology, partnered with its strategic business model, helped it to expand its customer base and grow organically.

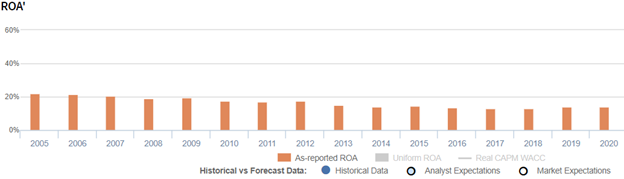

As-reported metrics seem to show that the company’s profitability is at fairly decent levels, with as-reported return on assets (ROA) ranging from 13%-22% for the past sixteen years.

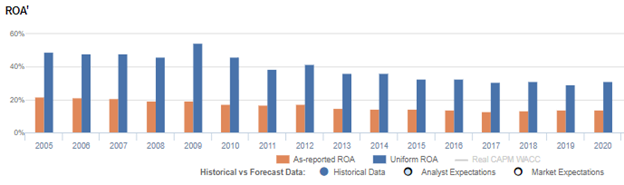

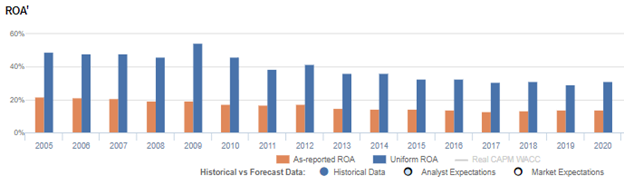

Uniform Accounting, on the other hand, reveals that the company has, in fact, a more robust returns than what as-reported metrics imply. Uniform ROAs actually ranged from 31%-49% in the same timeframe. Furthermore, forecasts are for returns to climb to 50% levels.

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of goodwill on Infosys’ balance sheet. Due to the acquisitions made over the course of its operations, the company’s goodwill sits at about $600 million to $700 million.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of Infosys’ earning power. Adjusting for goodwill, we can see that the company isn’t actually displaying lackluster performance. In fact, it is the opposite, with returns that are more than 2x greater.

Infosys Limited’s profitability is more robust than you think

As-reported metrics are distorting the market’s perception of the firm’s profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight.

Infosys’ Uniform ROA has been higher than its as-reported ROA in the past sixteen years. For example, Uniform ROA was 55% in 2009, while as-reported ROA was only 19%.

The company’s Uniform ROA for the past sixteen years has ranged from 30% to 55%, while as-reported ROA has ranged only from 13% to 22% in the same timeframe.

Specifically, Uniform ROA increased from 49% in 2005 to 55% 2009, before gradually fading to 31% through 2020.

Infosys Limited’s Uniform earnings margins are weaker than you think, but its Uniform asset turns make up for it

Volatility in Uniform ROA has been driven by trends in Uniform earnings margins and to a lesser extent, Uniform asset turns, with peaks and troughs lining up historically with that of Uniform ROA.

After trending at 23% from 2005 to 20010, Uniform margins gradually declined to 16% in 2014, before rebounding to 20% in 2018. It then fell to 15% in 2020.

Meanwhile, Uniform turns trended at 1.9x to 2.3x levels from 2005 to 2016, before fading to 1.6x. It then recovered to 2.0x in 2020.

SUMMARY and Infosys Limited Tearsheet

As the Uniform Accounting tearsheet for Infosys Limited (INFY:IND) highlights, the Uniform P/E trades at 29.4x, which is above the global corporate average of 25.2x, and its own historical average of 21.2x.

High P/Es require high EPS growth to sustain them. That said, in the case of Infosys, the company has recently shown a 3% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Infosys’ Wall Street analyst-driven forecast is a 15% and 13% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Infosys’ INR 1,272 stock price. These are often referred to as market embedded expectations.

The company needs to have Uniform earnings grow by 10% per year over the next three years in order to justify current stock prices. What Wall Street analysts expect for Infosys’ earnings growth is above what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power is 5x the long-run corporate average. Also, cash flows and cash on hand are 3x its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low dividend risk.

To conclude, Infosys’ Uniform earnings growth is below its peer averages but the company is trading above its average peer valuations.

About the Philippine Market Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com