With its massive scale and financial capacity, this pharma giant was able to keep a steady stream of R&D investments, leading to Uniform ROAs of 18%+

This pharmaceutical industry leader successfully made a name for itself through the development of some of the most popular drugs and treatments consumers know now. It further expanded its portfolio by focusing primarily on strengthening its investments in research and development.

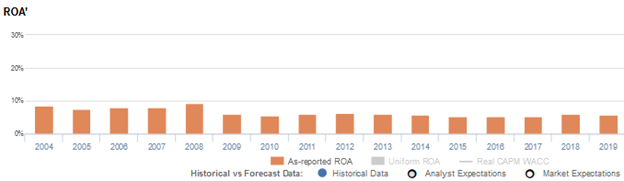

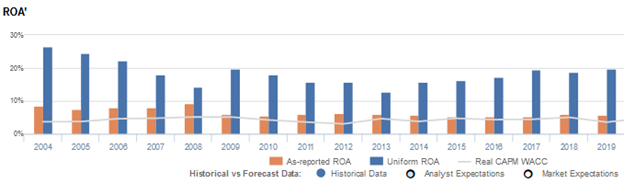

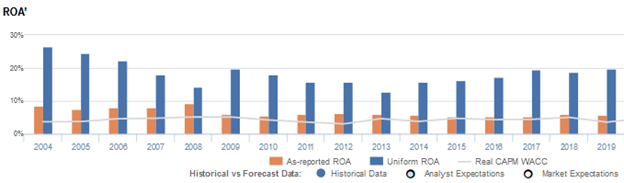

Looking at as-reported metrics, it seems that using this strategy has helped the company peak at a profitability of only 9%. However, TRUE UAFRS-based (Uniform) analysis shows that the company’s diverse drug portfolio and consistent R&D investments has actually helped it reach Uniform ROAs north of 18%.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

In the days of yore, magic and religion were prominently intertwined with ancient medical solutions. Some civilizations performed various rituals or recited prayers to heal the sick, other civilizations relied on plants (a practice called herbalism), and others used a combination of both.

Medicine has evolved greatly since then—the invention of the microscope, stethoscope, x-ray, and other equipment have paved the way for medical breakthroughs that significantly improved the modern quality of life.

One of these breakthroughs is the development of vaccines.

In the late 1700s, Edward Jenner observed that people who had cowpox were immune to smallpox. His observation was proven to be true upon inoculating a person using the cowpox virus, who then became immune to smallpox.

The smallpox vaccine was the first vaccine to be developed against a contagious disease. After some modifications later, Jenner’s breakthrough vaccine eventually eradicated smallpox, making it the first and only disease to ever be eradicated completely.

Vaccines have always played a crucial role in preventing or curing certain diseases. It’s especially more crucial now considering how we’re in the middle of a pandemic, fighting COVID-19.

Fortunately, scientists and big pharmaceutical companies from all over the globe have been working tirelessly over the past year to develop a vaccine against the coronavirus. Pfizer (PFE), in collaboration with BioNTech, was the first among these companies to come out with a vaccine with a 95% efficacy rate.

Originally a chemical manufacturing company, Pfizer has become one of the world’s largest pharmaceutical companies with the largest privately funded research organization.

The company works on the development of drugs, vaccines, and healthcare equipment, and specializes in the fields of immunology, oncology, neurology, as well as in generics. Its portfolio consists of hundreds of pharmaceutical products that it markets and sells globally.

In particular, Pfizer has sold about 200 million doses of its coronavirus vaccine to the U.S. government alone, with its partner firm, BioNTech, planning to produce about 1.3 billion doses throughout 2021.

Pfizer continues to expand its portfolio through continuous research and development activities. The company has about eight R&D laboratories in the U.S., employing around 1,500 scientists who oversee more than 500,000 lab tests and 36 clinical trials currently.

To improve its treatment and trial research, it has also partnered with companies that specialize in AI technology. With Saama Technologies’ Life Science Analytics Cloud (LSAC) platform, for example, Pfizer was able to delve deeper into identifying inefficiencies and making improvements in its clinical data mining processes.

Overall, being one of the largest pharmaceutical companies in the world does have its advantages. Pfizer’s massive scale and financial capacity have allowed it to sustain a steady stream of R&D activities that have kept its drug pipeline full.

However, as-reported metrics don’t exactly show an established giant leading the pharmaceutical industry—return on assets (ROAs) have fallen from 9% in 2008 to only 5%-6% in recent years.

In reality, its highly diverse drug portfolio consisting of blockbuster drugs like Advil and Robitussin, and robust R&D investments have led to strong, improving Uniform returns of more than 18%.

One source of the distortion between Uniform and as-reported ROAs comes from as-reported metrics incorrectly treating R&D as an expense.

R&D is an investment in the long-term cash flow generation of the company. Recording R&D as an expense violates one of the core principles of accounting, which is that expenses should be recognized in the period when the related revenue is incurred.

Since as-reported accounting records R&D on the income statement, as opposed to recording it as an investment on the balance sheet, net income can become materially understated.

Pfizer materially spends on R&D as it continues to make investments to expand its product portfolio. The company’s R&D spend has consistently been around 25% of total operating costs, significantly distorting the company’s profitability.

After adjustments, we can see that Pfizer’s Uniform ROA is, in fact, positive and is materially higher than as-reported ROAs. Without this adjustment, it appears that the firm is having less success with its R&D investments than it really is, leading to poorer valuations.

Pfizer’s earning power is actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

Pfizer’s Uniform ROA has actually been higher than its as-reported ROA in the past sixteen years. For example, as-reported ROA was 6% in 2019, but its Uniform ROA was actually more than thrice that at 20%. When Uniform ROA peaked at 26% in 2004, as-reported ROA was only at 9%.

Through Uniform Accounting, we can see that the company’s true ROAs have actually been much higher. Pfizer’s Uniform ROA for the past sixteen years has ranged from 13% to 26%, while as-reported ROA ranged only from 5% to 9% over the same timeframe.

Pfizer’s Uniform earnings margins are generally weaker than you think, but its Uniform asset turns slightly make up for it

Pfizer’s trends have been primarily driven by trends in Uniform earnings margin and to a lesser extent, Uniform asset turns.

After falling from 39% in 2004 to 26% in 2008, Uniform margins rebounded to a peak of 42% in 2009. However, Uniform Margins then faded to 26% in 2013, and subsequently recovered back to 39% in 2019.

Meanwhile, Uniform Turns remained stable at 0.7x levels in 2004-2005, before declining to 0.5x-0.6x levels through 2019.

At current valuations, the market is pricing in expectations for a compression in Uniform margins, coupled with further stability in Uniform turns.

SUMMARY and Pfizer’s Tearsheet

As the Uniform Accounting tearsheet for Pfizer Inc. (PFE) highlights, its Uniform P/E trades at 11.7x, which is below the global corporate average of 25.2x, but around its historical average of 13.2x.

Low P/Es require low EPS growth to sustain them. In the case of Pfizer, the company has recently shown a 3% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Pfizer’s Wall Street analyst-driven forecast is a 29% EPS growth and a 16% EPS decline in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Pfizer’s $36 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 10% each year over the next three years and still justify current prices. What Wall Street analysts expect for Pfizer’s earnings growth is above what the current stock market valuation requires in 2020, but below its requirement in 2021.

Furthermore, the company’s earning power is 3x the corporate average. However, cash flows and cash on hand are 2x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low credit and dividend risk.

To conclude, Pfizer’s Uniform earnings growth is above peer averages, but the company is trading below average peer valuations.

About the Philippine Markets Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com