With more than 174 million active buyers, this company proves that it can manage auctions and listings, along with Uniform ROAs of 20%+ levels

Strict quarantine measures implemented by governments globally have adversely impacted small and individual non-essential retailers. As a solution, some of these businesses have shifted to online retailing in order to survive.

This company has managed to capture a sizable portion of this retail shift. In the past, it has succeeded in this space thanks to the flexibility of its transaction methods—through auctions and fixed-price listings.

As-reported metrics portray that this hasn’t been much of an advantage, given below cost of capital returns, but TRUE UAFRS-based (Uniform) analysis shows that it has actually helped the company maintain robust return on assets (ROAs) of over 20%.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

Widespread retail closures due to the pandemic have led to a dramatic shift in consumer spending behavior, moving much of that spending from physical to online purchases.

As expected, e-commerce sales have accelerated considerably over the past few months, with online retailers Amazon (AMZN) and eBay (EBAY) benefitting from the current spending environment.

eBay alone has seen a 3.5 million increase in the number of active buyers from Q1 2019, now standing at about 174 million.

Meanwhile, sellers—mostly small retail stores and individuals—have also flocked to the website to survive through the lockdown. Hardware stores, toy shops, and fashion retailers, among others, turned to the site to continue operations as physical purchases of non-essentials are deprioritized.

eBay has always had success in pulling buyers and sellers in because of the mix of their transaction methods. Their mix of fixed prices and auctions gives their customers more spending/selling flexibility.

eBay, which was first called The AuctionWeb, was the pioneer of online person-to-person auction trading. It was a purely auction-based website offering a few used items for sale. Previously, such transactions were only done through an auction house, collectibles shows, flea markets, or garage sales.

eBay provided an online marketplace that makes it more convenient and faster for buyers and sellers to trade goods, leading to a surge in transactions on the site.

eBay has since grown into a multi-billion-dollar business that allows people to sell everything from rare collectibles to jets and yachts.

Furthermore, the company has evolved into a business where transactions can also be executed through a fixed-price sale, similar to what Amazon does.

Though eBay has other sources of revenues, ebay.com, which is a part of the Marketplace segment, is where most of its revenues are sourced. The company’s profitability is dependent on the fees it collects from the sellers. Initially, a listing fee is charged on every item posted.

There are, however, specific tranches where a minimum number of listings have to be reached before the sellers can have a corresponding number of free listings. After which, the company will demand a fixed payment charge for every subsequent listing.

eBay also charges a commission fee on top of the listing fee. The “final value fee” ranges from about 3%-10% of the sale price depending on the product category.

Since revenues are tied to transaction fees, it is critical that the company boosts its average sales price, or the number of items sold on the site.

Fortunately, its auction-style and fixed-price business models do well in terms of capturing the niche market of merchandisers and customers looking to buy and sell unique items that cannot be found on normal marketplaces.

Besides the Marketplace, eBay has also made a number of acquisitions to further increase their revenue streams.

Most notable of these were Paypal, which was acquired in 2002 and subsequently spun off in 2015, and Stubhub, which was acquired in 2002 but was divested a few months ago.

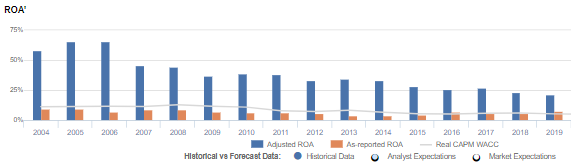

As-reported ROAs have ranged from 4%-7% in the past eight years, indicating that these acquisitions were generating insufficient returns.

In reality, the company’s profitability is much stronger, with Uniform ROAs actually staying above 20%.

The distortion comes from as-reported metrics failing to consider the amount of goodwill on eBay’s balance sheet, which is substantial given their many acquisitions in recent years.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of eBay’s earning power. Adjusting for goodwill, returns are actually 3x-6x greater.

However, market expectations are for ROA levels to fade slightly from 20%+ levels due to short-term COVID headwinds and long-term competitive pressures across their business.

Even so, the company’s focus on their auction-based business model and ability to corner the market of buyers and sellers looking for unique items would likely sustain its profitability in the long-term. ROAs are not likely to drop massively as market expectations would suggest. As such, equity upside is warranted.

eBay’s earning power is actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

eBay’s Uniform ROA has actually been higher than its as-reported ROA in the past sixteen years. For example, as-reported ROA was 7% in 2019, but its Uniform ROA was actually 3x higher at 21%. When Uniform ROA peaked at 66% in 2006, as-reported ROA was at a meager 7%.

Through Uniform Accounting, we can see that the company’s true ROAs have actually been much higher. eBay’s Uniform ROA for the past sixteen years has ranged from 21% to 66%, while as-reported ROA ranged only from 4% to 10% in the same timeframe.

After dropping from 66% in 2006 to 46% in 2007, Uniform ROA further decreased to 28% in 2015. Afterwards, Uniform ROA reached new low levels at 21% in 2019.

eBay’s margins are weaker than you think, but it is offset by the trend in Uniform asset turns

eBay’s improving profitability has been driven by trends in both Uniform earnings margins and Uniform asset turns.

From 2004-2006, Uniform earnings margins remained stable at 26% to 29% levels. It then declined to 21% in 2007, before bouncing back to 27% levels in 2010. Thereafter, Uniform margins remained stable at 24%-26% levels through 2015 before decreasing to 22% in 2019.

Meanwhile, Uniform asset turns fell from a peak of 2.5x to 1.5x from 2006-2010. It further declined to 1.1x in 2016, and decreased to 1.0x in 2019.

At current valuations, markets are pricing in expectations for continued declines in both Uniform margins and Uniform turns, which is likely too bearish, considering the firm’s strong economic moats.

SUMMARY and eBay Inc. Tearsheet

As the Uniform Accounting tearsheet for eBay Inc. (EBAY) highlights, the Uniform P/E trades at 15.3x, which is below corporate average valuation levels, but around its own recent history.

Low P/Es require low EPS growth to sustain them. In the case of eBay, the company has recently shown a 13% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, eBay’s Wall Street analyst-driven forecast is a 3% and 15% growth in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify eBay’s $43 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 6% each year over the next three years and still justify current prices. What Wall Street analysts expect for eBay’s earnings growth is above what the current stock market valuation requires in 2020 and 2021.

The company’s earning power is 4x the corporate average. Also, cash flows are 2x higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, eBay’s Uniform earnings growth is above peer averages in 2020. However, the company is trading below average peer valuations.

About the Philippine Markets Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com