With the sustained popularity of sports culture, this apparel company might just further swoosh past at double the ROAs that the market thinks.

In the Philippines, basketball is everywhere—on the streets, on courts, and in stadiums.

If you watch enough games, you might notice that this brand of footwear is a local favorite among basketball players.

But these were first made for running before they ever became a basketball staple.

Through a series of “Demand Creation” marketing strategies, this company has established itself as a powerhouse not only in running and basketball shoes, but also with multiple apparel across other sports.

These strategies propelled the company’s stock price from $20 a decade ago to $102 currently. The as-reported ROAs don’t justify that, but the Uniform ROAs do.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

Every country has a favorite sport. For France, it’s football. For India, it’s cricket. For the Philippines, it’s basketball.

When you think of basketball, you might immediately associate it with it being a man’s game. During the American colonial period however, when basketball first came to the Philippines, it was actually introduced as a woman’s game.

Unfortunately, due to ideological conflict, the popularity of women’s basketball in the Philippines eventually faded away.

In 1910, five years after the sport’s arrival, the first men’s national team was formed. The team won their first Far Eastern Championship Games in 1913.

Throughout the decades, basketball continued to evolve into a cultural phenomenon that transcended time and philosophy.

Filipinos would use this sport as an escape, as a means for socializing, and enjoyment. As a result, the country became a business opportunity for athletic apparel companies around the globe.

In 1998, Nike entered the Philippine basketball market and took the country by storm.

But Nike didn’t begin with serving the basketball community in mind.

Phil Knight, then still a student at Stanford University, was tasked to write a business plan for a school project. Being a track athlete, naturally, his project focused on shoes—running shoes, to be exact.

He postulated that Japanese-made shoes would be more cost-efficient given the cheap labor, enabling them to compete with then giants Puma and Adidas. So he tested it out.

Together with his coach Bowerman, Knight opened Blue Ribbon Sports, an import distributor of the Japanese Onitsuka track shoe.

The partnership with the foreign company proved to be a wild success.

Demand flourished. New designs became hits. Sales boomed.

But eventually, the relationship between the two companies turned sour and Blue Ribbon Sports split up.

The company needed a brand new identity, one that was stronger.

After consultations with a few acquaintances, Knight hesitantly settled on the “swoosh” as the company logo and “Nike” as its name, not knowing that these would eventually be one of the world’s most instantly recognizable and valuable brands.

Nike continued to market its hit designs and created another shoe with the “waffle” sole, which at that time was an innovative and original creation in the shoe world.

The continued success of these designs enabled the growth that paved that way for the company’s IPO in 1980.

Since then, Nike has ramped up its marketing efforts to establish the multi-billion business that it is today.

First, it was their iconic slogan “Just Do It.” Their North American market share went up from 18% to 43% with just this campaign alone.

Then, their celebrity endorsements cemented their leadership in the industry. They’ve signed celebrities from Michael Jordan to Kobe Bryant in basketball, to other sports with Tiger Woods (golf), Serena Williams (tennis), and Cristiano Ronaldo (football).

Nike doesn’t just sell its products; it sells a lifestyle.

Most of the company’s marketing campaigns focus on an appeal to the consumer’s emotions. It frames its products in a way that tells a story.

Everyone has a story—the company acts as an avenue to inspire people that they’re a hero in their own stories.

With the company’s diversification of its products across multiple sports and their brilliant marketing initiatives, or what they call “Demand Creation,” it’s no wonder that Nike has gone from being a penny stock to being a blue chip stock currently trading at new highs.

Nike’s earning power is actually more robust than you think

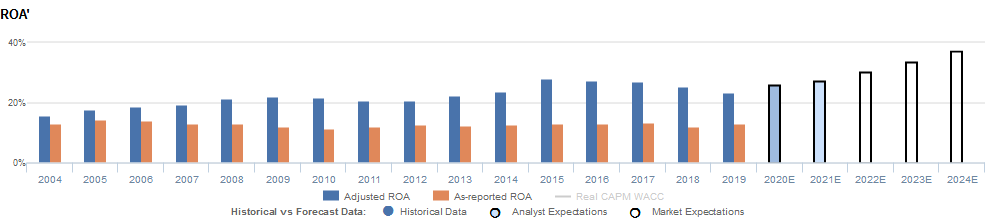

As-reported metrics significantly understate Nike, Inc’s (NKE:USA) profitability. For example, as-reported ROA for NKE was 13% in 2019, materially lower than Uniform ROA of 24%, making NKE appear to be a much weaker business than real economic metrics highlight.

Moreover, as-reported ROA has slightly decreased from 14% in 2005 to current 13% levels, while Uniform ROA has expanded from 18% to 24% over the same period, significantly distorting the market’s perception of the firm’s historical profitability trends.

Historically, NKE has seen robust, overall improving profitability. Uniform ROA increased from 16% in 2004 to 21%-22% levels in 2008-2013. It then expanded to peak 27%-28% levels from 2015-2017, before falling to 24% in 2019.

Nike’s earnings margins are overstated while asset turns are understated

Historical Uniform ROA expansion was driven by improvements in both Uniform earnings margin and Uniform asset turns, while recent declines were driven by declining Uniform earnings margins.

After seeing Uniform earnings margins gradually increase from 8% in 2004 to a plateau of 10%-11% from 2009-2014, it expanded further to 12% levels in 2015-2018, before contracting back to 10% in 2019.

Meanwhile, since improving from 1.9x in 2004 to 2.0x-2.1x levels in 2005-2013, Uniform asset turns expanded further to a peak of 2.4x in 2015, before declining to 2.2x in 2018 and expanding back to 2.3x in 2019.

At current valuations, markets are pricing in expectations for both Uniform earnings margins and Uniform asset turns to expand to record highs.

SUMMARY and Nike Tearsheet

As the Uniform Accounting tearsheet for Nike, Inc. (NKE:USA) highlights, the Uniform P/E trades at a very high 32.0x, well above corporate average valuation levels and its own recent history.

High P/Es require high EPS growth to sustain them. In the case of Nike, the company has recently shown only -1% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Nike’s Wall Street analyst-driven forecast is 22% and 13% into 2020 and 2021, respectively.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $98 per share. These are often referred to as market embedded expectations.

In order to meet the current market valuation levels of Nike, the company would have to see Uniform earnings grow by 13% each year over the next three years.

What Wall Street analysts expect for Nike’s earnings growth rises significantly above what the current stock market valuation requires.

To conclude, Nike’s Uniform earnings growth is in line with peer averages in 2020, with the company also trading at average peer valuations.

The company’s earning power, based on its Uniform return on assets calculation, is above average as well. Together, this signals low cash flow risk relative to the current dividend level in the future.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com