With Uniform ROAs largely over 20%, this company proves that betting on a growing industry’s pickaxe seller is always the right call

Investing in companies who are suppliers to a particular industry, or what are called “pickaxe sellers,” is often a smart move. The logic is, instead of betting on which business makes the greater product, bet on the one supplying the materials for the product—that way, you win regardless.

This company is a supplier to the growing semiconductor industry. Its business is constantly in demand from chip manufacturers who are continually developing more advanced tech, especially now from companies at the forefront of big tech trends.

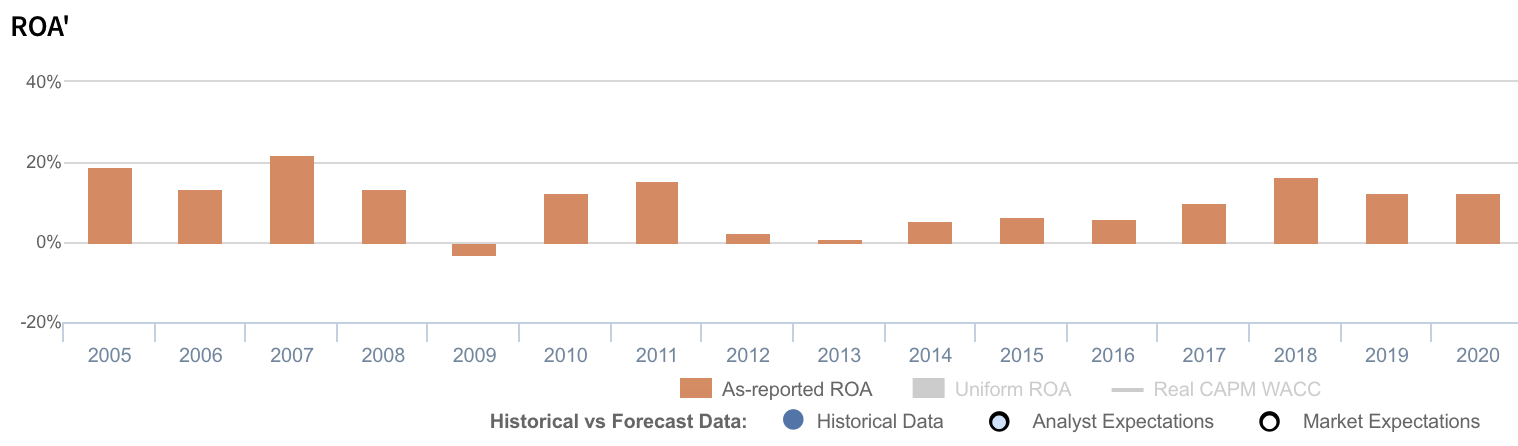

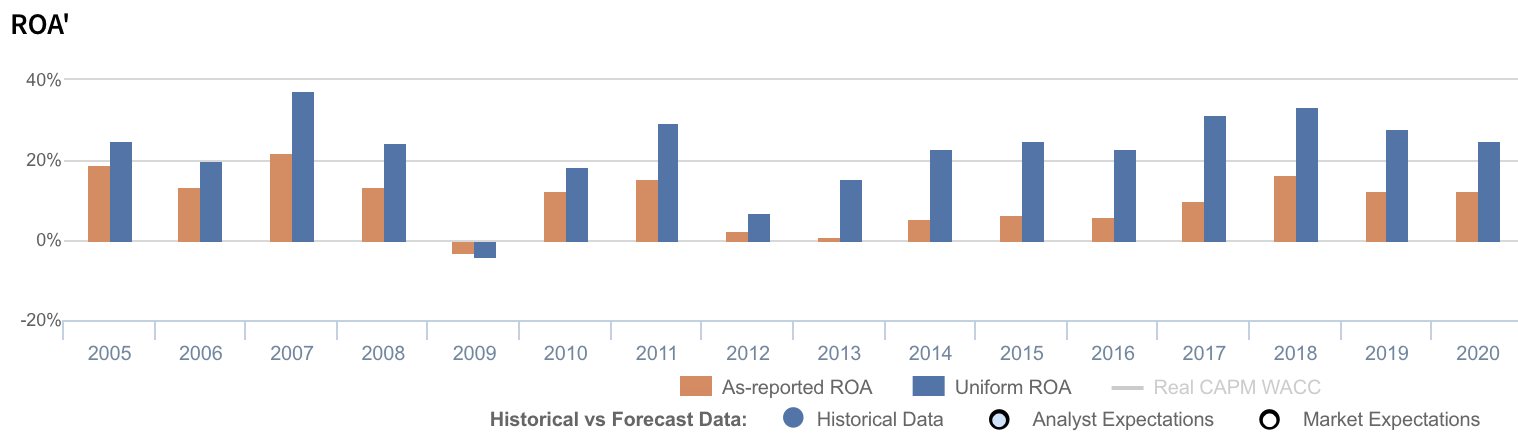

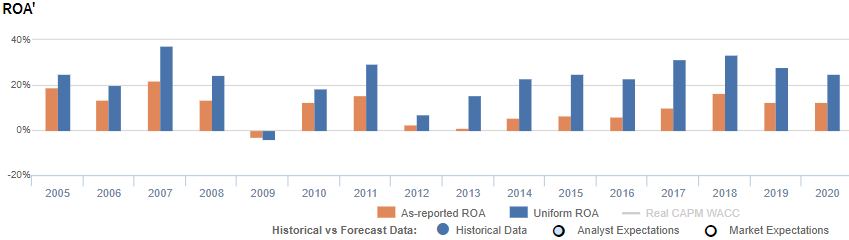

While as-reported metrics show only a business with lackluster returns, Uniform Accounting reveals the opposite, with Uniform ROAs mainly over 20%, as expected from a “pickaxe seller.”

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

One of the best companies to invest in is the one selling the pickaxes, not the one mining the gold—this solid investment advice is better understood in context of the California Gold Rush.

In 1848, gold was struck at Sutter’s Mill in California. News of the discovery had people across the U.S., and even abroad migrating to the state, in search of gold. Thus began the seven-year long gold rush.

Gold mining is a tough business. Not only do you have to worry about the low probability that you’d ever find a meaningful amount of gold, you also have to worry about surviving finding gold, or someone else pushing you out.

While everyone else was focused on mining, people like Levi Strauss and Samuel Brannan went into the business of supplying the miners. Strauss sold durable trousers and other dry goods, while Brannan sold pickaxes and shovels.

There is no guarantee that gold will be found, but one thing’s for sure: there will always be people mining. Strauss and Brannan’s businesses were phenomenal because no matter who finds or sells the most gold, their products will constantly be in demand.

This is why investing in “pickaxe sellers” is a great investment play.

Instead of investing in oil producers like Exxon Mobil or electric vehicle (EV) manufacturers like Tesla, it may be better to put your money in Schlumberger (oil and gas services) or Panasonic (EV batteries) who are suppliers to those industries.

Similarly, Lam Research (LRCX) is one of those great pickaxe sellers.

The company is a supplier to some of the biggest names in the semiconductor industry. Its products are mainly used as part of the wafer fabrication process, specifically applied for critical components such as transistors, memory storage, and interconnects.

Lam Research’s solutions also help solve a problem posited by Moore’s Law—an observation that the number of transistors in a single chip would double every two years or so. For that to work, the transistors would have to continuously shrink in size to fit in the chip.

It has been increasingly more difficult for semiconductor manufacturers to pack in more and more transistors because it takes a lot of time to develop the technology needed, as well as R&D spend.

The company’s 3D NAND solution is an innovative workaround to this problem. Instead of shrinking the transistors to fit, 3D NAND allows chip manufacturers to stack them vertically to increase capacity.

Lam Research continues to develop new chip architecture and advanced solutions to enable new technology to progress. Plus, with the advent of big tech trends such as 5G and cloud computing, the company stands to win big as a supplier to the semiconductor industry.

Being a pickaxe seller, expectations are for outsized returns. However, Lam Research’s returns have been lackluster, with as-reported return on assets (ROA) mostly at cost-of-capital levels at best, with a few years where returns periodically spiked before falling back to weaker levels.

After Uniform Accounting adjustments are made, we can see that the company is in fact a high-return business, with ROAs at over 20% levels, save for a few periods of downturn.

One source of the distortion between Uniform and as-reported ROAs comes from as-reported metrics incorrectly treating R&D as an expense.

R&D is an investment in the long-term cash flow generation of the company. By recording R&D as an expense, this violates one of the core principles of accounting, which is that expenses should be recognized in the period when the related revenue is incurred.

Since as-reported accounting records R&D on the income statement instead of as an investment on the balance sheet, net income can become materially understated.

Lam Research materially spends on R&D to offer better equipment and tools to provide solutions for storage-semiconductor manufacturers like increasing storage density on chips, improving quality and consistency of chips, and reducing production times.

The company’s R&D spend has consistently been around $1.2 billion, or 60% of total operating costs, significantly distorting the company’s profitability.

After the necessary adjustments, we can see that Lam Research’s Uniform ROAs are actually significantly higher than as-reported ROAs. Without this adjustment, it appears that the firm is having less success with its R&D investments than it really is, leading to poorer valuations.

Lam Research’s earning power is actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think the company is a much weaker business than real economic metrics highlight.

Lam Research’s Uniform ROA has actually been higher than its as-reported ROA in fifteen of the past sixteen years. For example, as-reported ROA was 13% in 2020, but its Uniform ROA is actually almost twice that at 25%.

Specifically, Lam Research’s Uniform ROA has ranged from -4% to 38% in the past sixteen years while as-reported ROA ranged only from -3% to 22% in the same timeframe.

After declining from 25% in 2005 to 20% in 2006, Uniform ROA rebounded to a peak of 38% in 2007 before dropping to -4% in 2009. Then, it subsequently recovered to 33% in 2018 before contracting to 25% in 2020.

Lam Research’s Uniform earnings margins are generally weaker than you think, but its Uniform asset turns make up for it

Volatility in Lam Research’s Uniform ROA has been driven by trends in both Uniform earnings margins and Uniform asset turns.

Uniform margins sustained 20%-28% levels in 2005-2008, before sharply declining to a low of -7% in 2009 and subsequently recovering to 26% in 2020.

Meanwhile, Uniform turns maintained 0.9x-1.4x levels in 2005-2008, before declining to 0.5x in 2009. Thereafter, Uniform turns expanded to 1.3x in 2018, before contracting to 1.0x in 2020.

At current valuations, markets are pricing in expectations for Uniform margins to reverse recent improvements and for Uniform turns to stabilize near current levels.

SUMMARY and Lam Research Corporation Tearsheet

As the Uniform Accounting tearsheet for Lam Research Corporation (LRCX) highlights, its Uniform P/E trades at 19.0x, which is below corporate average valuation levels, but above its own recent history.

Low P/Es require low EPS growth to sustain them. In the case of Lam Research, the company has recently shown a 10% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Lam Research’s Wall Street analyst-driven forecast is a 50% and 6% EPS growth in 2021 and 2022, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Lam Research’s $492 stock price. These are often referred to as market embedded expectations.

The company needs Uniform earnings to grow 6% each year over the next three years to justify current prices. What Wall Street analysts expect for Lam Research’s earnings growth is above what the current stock market valuation requires in 2021, and in line with its requirement in 2022.

Furthermore, the company’s earning power is 4x the corporate average. Moreover, cash flows and cash on hand are nearly 4x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Lam Research’s Uniform earnings growth is in line with its peer averages in 2021, and the company is also trading in line with average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com