You might find that the “Google of South Korea” is more profitable than what is reported, with a TRUE earning power of 31%!

This Korean technology company is an online search engine and portal site that also provides online advertising and content creation. Thanks to its live streaming platform and mobile services applications, the company has been able to expand its reach around the world.

However, as-reported metrics show muted profitability even with the company’s efforts to widen its presence in the market. Uniform Accounting paints an entirely different picture, with Uniform return on assets (ROA) higher than what is reported.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

Everything is just a click away.

Nowadays, information is usually at the tip of our fingers. Whenever we want or need to know something, all we have to do is search online.

Need to know the definition of a word you never encountered before? Search it on an online dictionary. Want to order that food you saw in a commercial? Buy it online and have it delivered to you. Looking for movies that will suit your taste? Just download or stream it online.

For the times when you don’t know exactly where to look for the things you need, a search engine is available to help you.

A web search engine is a tool that helps internet users look for information on the World Wide Web (WWW) by searching through a database of information that matches the user’s query.

In the United States, the internet search industry giant Google holds more than 90% of the web search market. Its significance to modern lifestyle is evident in its inclusion in our conversational language. Statements like “just google it” or “I googled the movie” act as replacements for searching for or looking something up online.

Despite Google’s dominance worldwide, it still hasn’t managed to come up on top in South Korea.

Sometimes called the “Google of South Korea,” Naver Corporation is the country’s largest web search engine. It is also the first Korean web service provider to develop and use its own comprehensive search engine.

Naver’s founders established the company because they could not find a search engine that had enough quality data in the Korean language. Naver then became the default Korean “internet homepage” with features like the Naver Cafe and Blog, dictionary and encyclopedia, and news.

To remain relevant to South Koreans, Naver continues to develop various tools to add to its search engine base.

In 2002, Naver formed its first Q&A webpage called Knowledge iN. Users could post questions and receive answers from other users. This allowed the platform to gather user-generated content, expanding the amount of relevant information available in Korea. Knowledge iN is even credited as the inspiration for Yahoo! Answers.

More recently, Naver developed V Live, their live streaming platform that connects K-Pop fans around the world through hosting various shows and concerts through their app. With the emergence of Hallyu, the app has gained more than 80 million downloads worldwide.

Naver has since evolved to a global information and communications technology (ICT) brand that also provides mobile services such as LINE messenger, SNOW video app, and its digital comics platform Naver Webtoon.

The company plans for an overseas expansion for Webtoon by centralizing its comics distribution to its U.S.-based subsidiary, Webtoon Entertainment. To gain more users worldwide, Naver also plans to expand its messenger app LINE, with its upcoming merger with Softbank Group, parent company of Yahoo! Japan.

Considering the expanding presence of the company’s offerings worldwide, as well as its ability to do this effectively, its as-reported returns of 5% in 2019 is weaker than what it should really be.

Naver’s real economic profitability is better reflected with Uniform Accounting adjustments, which shows its TRUE earning power.

What as-reported metrics fail to do is to consider the company’s excess cash on the balance sheet. While most companies inherently need some level of cash to operate, the portion of that balance that is earning limited or no return—or excess cash—ends up diluting as-reported ROAs.

If excess cash remains included in the company’s asset base in computing its performance metrics, the company’s profitability and capital efficiency may appear weaker than it actually is.

Over the past nine years, Naver has had a significant amount of excess cash sitting idly in its balance sheet, ranging from 18% to 48% of its unadjusted total assets.

After excess cash and other significant adjustments are made, the company actually had a 31% Uniform ROA in 2019, which is almost 8x stronger than their as-reported ROA of 4%.

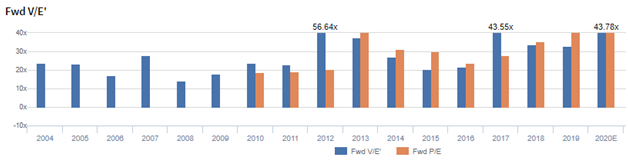

Naver’s valuations are cheaper than corporate averages

Naver Corporation (035420:KOR) currently trades above corporate averages at a 43.8x Uniform P/E (blue bars), slightly below its as-reported P/E of 47.8x (orange bars).

At these levels, the market is pricing in expectations for Uniform ROA to improve to 102% in 2024, accompanied by 9% Uniform asset growth going forward.

Analysts have less bullish expectations, projecting Uniform ROA to increase at 92% levels in 2021, accompanied by a 5% Uniform asset shrinkage.

Naver’s profitability is much better than you think it is

As-reported metrics are distorting the market’s perception of the firm’s profitability.

If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight.

Naver’s Uniform ROA has actually been higher than its as-reported ROA in the past nine years. For example, as-reported ROA is 4% in 2019, significantly lower than its Uniform ROA of 31%. When Uniform ROA peaked at 130% in 2010, as-reported ROA was just at 21%. The company’s Uniform ROA for the past sixteen years has ranged from 19% to 130%, while as-reported ROA ranged only from 4% to 35% in the same timeframe.

From 69% in 2004, Uniform ROA gradually improved to 128% in 2007, before falling to 74% in 2009. Afterwards, Uniform ROA recovered to 130% in 2019, before compressing to 20% in 2013, and bouncing back to 122% in 2017. Uniform ROA declined to 31% in 2019.

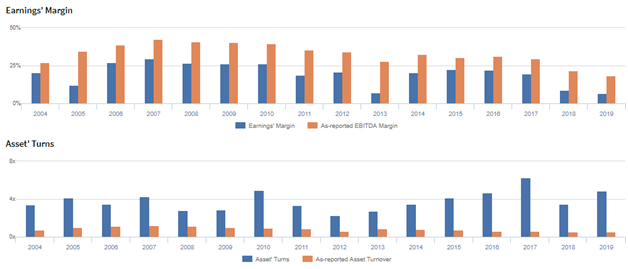

Naver’s Uniform earnings margins are weaker than what you think but its robust Uniform asset turns make up for it

Volatility in Uniform ROA has been driven by trends in Uniform asset turns, slightly offset by trends in Uniform earnings margins, with peaks and troughs lining up historically with that of Uniform ROA.

Uniform earnings margins fell from 21% in 2004 to 12% in 2005, before recovering to 30% in 2007. It then gradually compressed to 7% in 2013, before improving to 23% in 2015 and fading back to 7% in 2019.

Meanwhile, Uniform asset turns increased from 3.4x in 2005 to 4.9x in 2010, before fading to 2.3x in 2012. It then recovered to 6.3x in 2017 before compressing to 4.8x in 2019.

SUMMARY and Naver Corporation Tearsheet

As the Uniform Accounting tearsheet for Naver Corporation (035420:KOR) highlights, the Uniform P/E trades at 43.8x, which is above corporate average valuation levels and its own recent history.

High P/Es require high EPS growth to sustain them. In the case of Naver, the company has recently shown a 15% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Korean International Financial Reporting Standards (K-IFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Naver’s sell-side analyst-driven forecast is a 52% and 47% earnings growth in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Naver’s KRW 269,000 stock price. These are often referred to as market embedded expectations.

In order to justify current market expectations, Naver would need to have Uniform earnings grow by 32% each year over the next three years. What sell-side analysts expect for Naver’s earnings growth is above what the current stock market valuation requires in 2020 and 2021.

The company’s earning power is 5x the corporate average. Also, cash flows are almost 5x higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Naver’s Uniform earnings growth is above its peer averages in 2019. The company is also trading above average peer valuations.

About the Philippine Market Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com