Qualcomm’s Adjusted ROA Reveals Economic Reality

Summary

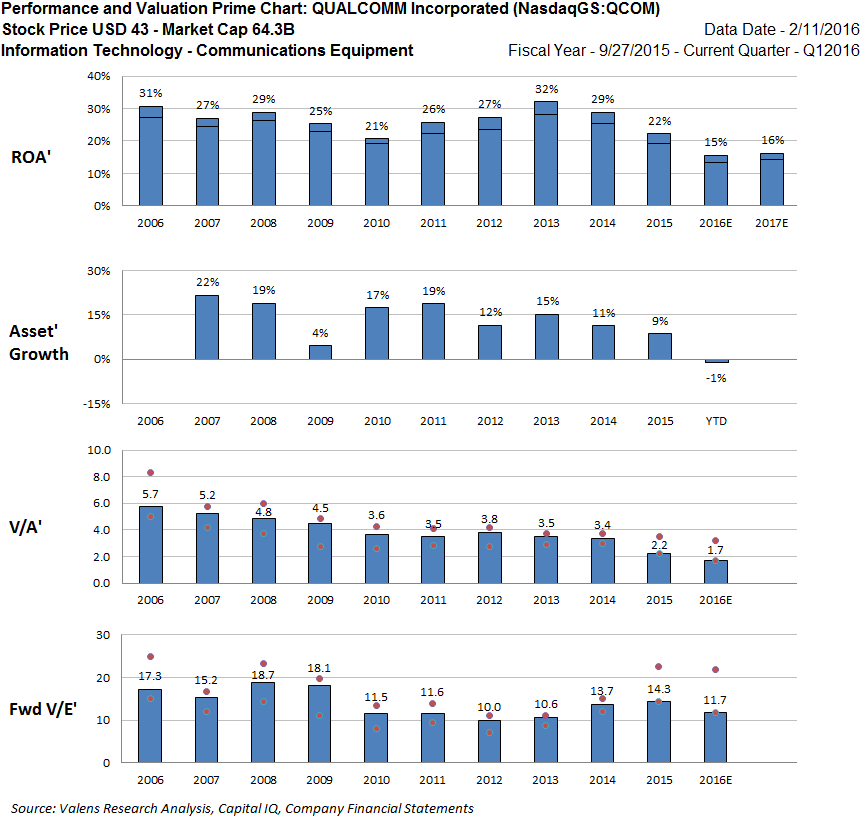

- Using Uniform Adjusted Financial Reporting Standards (UAFRS), QCOM’s Adjusted Return on Assets is 22% in 2015 – significantly higher than the traditional 9% ROA most financial databases report.

- One culprit behind this major distortion is QCOM’s $5.5bn goodwill which inflates the company’s assets, leading to a significant distortion of the firm’s economic reality under GAAP.

- Another culprit is the GAAP accounting for QCOM’s $5.5bn R&D expenditure which deflates the company’s earnings.

Performance and Valuation Prime Chart

The problem with Generally Accepted Accounting Principles (GAAP) is that they create inconsistencies when comparing one company to another and when comparing a company to itself from year to year. By making adjustments, we aim to remove the financial statement distortions and miscategorizations of GAAP. Some of these can be automated through consistently applied formulas. However, many must be made manually. Manual adjustments that cannot be automated include mergers and acquisitions accounting, special charges, business impairments, and others. The practice of creating consistent, apples-to-apples comparable measures of financial performance is often considered either tedious or overly complex by even seasoned financial analysts.

Under GAAP, as-reported financial statements and financial ratios of QCOM do not reflect economic reality. The traditional return on assets computation understates the company’s profitability by incorrectly including certain items. The distortion of both profitability measures and valuation metrics of QCOM were driven by the inclusion of goodwill ($5.5bn), which inflates the firm’s assets, and by incorrectly expensing items like R&D ($5.5bn) and operating leases ($99mn) rather than treating them as part of the company’s investments.

After adjusting for similar issues and a host of other GAAP-based miscategorizations, we calculate QCOM’s UAFRS-based Return on Assets as 22% in 2015. In contrast, most financial databases show a traditional ROA of only 9%. The profitability of QCOM’s operations and equity’s true value are therefore not what traditional metrics originally suggest.

Click here to read the article in its entirety at Seeking Alpha.