Ratings Agencies Miss Delta’s Flight To IG

Summary

- Delta Air Lines’ credit risk is materially overstated by CDS markets and overstated by Moody’s.

- CDS is at 305bps, compared to an Intrinsic CDS of only 131bps.

- Moody’s Baa3 rating is four notches too low, given Delta Air Lines’ investment grade cash profile.

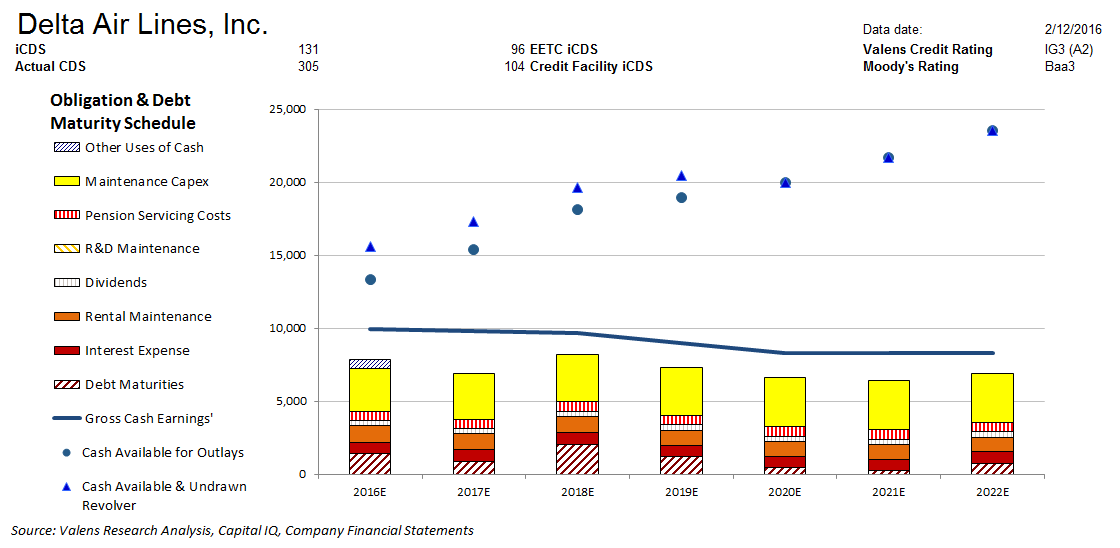

Cash Flow Profile

Moody’s rates Delta Air Lines, Inc. (NYSE:DAL) with a cross-over Baa3 rating. However, Valens rates DAL with an upper medium investment grade IG3 credit rating, or an A2 equivalent using Moody’s ratings scale. DAL’s combined cash flows and cash on hand comfortably outstrip all of their upcoming obligations, including their many debt maturities, driving a rating four notches higher than Moody’s.

CDS markets are also materially overstating DAL’s credit risk, with CDS at 305bps relative to an Intrinsic CDS of only 131bps.

The chart provides a far more comprehensive view of credit fundamentals than traditional ratio-based analyses. By using Uniform Adjusted Financial Reporting Standards based metrics, it shows the cash flow generation and cash obligations related to the credit of the firm, adjusted for non-cash financial statement reporting distortions from GAAP. The blue line indicates the gross cash earnings (UniformFRS adjusted cash flow number) expected to be generated based on consensus analyst estimates and Valens Research’s own in-house research team. The blue dots above that line include the cash available at that time while the blue triangles indicate that same amount plus any existing, available lines of credit.

The colored, stacked bars show the cash obligations of the firm in each year forecast. The most difficult obligations to avoid are at the bottom of each stack, such as interest expense. The obligations with more flexibility to defer year to year, such as pension contributions and maintenance capital expenditures, are at the top of the stacked bars. All of the calculations are adjusted for non-cash distortions that are inherent in GAAP accounting, including the highly problematic and often misused statement of cash flows.

If the company generates and has cash levels that are above their obligations, the risk of default is extremely low. Even if the cash generated yearly is close to the levels of the stacked bars, a company generally has the flexibility to defer payments of various kinds. For example, they can allow assets to age a little longer, or they can cut certain maintenance costs such as maintenance capex. While decisions such as those can create other business concerns, the issue in credit risk is simply this: Does the company have enough cash to service their credit obligations?

DAL’s cash flows comfortably exceed all obligations, including debt maturities that range from $264mn-$2.1bn, through the next seven years. In addition, their current cash on hand stands at $3.4bn, and is expected to build going forward. Thus, the firm should have no issues handling all their obligations even if cash flows were to dip.

Click here to read the article in its entirety at Seeking Alpha.