R&D Is an Investment, Not an Expense – How capitalizing R&D impacts understanding corporate profitability

Written By: Joel Litman and Rob Spivey

In several recent Seeking Alpha articles Valens has posted, questions about R&D capitalization and R&D investment have come up in the comments section. As such, we felt it was worth writing a post about this issue, the theoretical underpinnings behind it, and how this impacts companies.

In this article, we highlight the impact of these adjustments for companies such as Facebook (FB), Gilead Sciences (GILD), Boeing (BA), and Danaher (DHR). Throughout the article we provide links so that you can see more about how the companies look after we adjust the financial statements. To be able to see how company analysis looks when you make this and other key adjustments to clean up the financial statements, and get a better picture of corporate profitability and valuations, click here. To read more about our adjustments, click here, and to understand how we think about analyzing companies, click here.

The Problem – Should R&D be treated as an expense or an investment?

The problem with Generally Accepted Accounting Principles (GAAP) is that they create inconsistencies when comparing one company to another, and can distort a company’s true historical profitability. By making adjustments, we aim to remove the financial statement distortions and miscategorizations of GAAP. In this article we will discuss why we capitalize R&D in order to see a clearer, more accurate picture of a company’s historical profitability.

Under GAAP, firms are required to expense R&D in the year spent. For many firms, this leads to extensive volatility in profit and return calculations, and to an inadequate measure of assets or invested capital. This doubly impacts return on asset calculations, and not consistently so, thereby creating wildly different calculations of economic profit.

Some would argue that IFRS’s treatment is superior. In IFRS, all research spending is expensed each year. However, development costs are capitalized once the “asset” being developed has met requirements of technical and commercial feasibility to signal that the intangible investment is likely to either be brought to market or sold. This gives the benefit that “successful” R&D is capitalized on the balance sheet, as opposed to expensed. However, the fact is, because IFRS provides more opportunity for the application of judgment, this only adds to the risk of distortion of financial statements as management teams attempt to apply uncertain assumptions to the implied certainty of the financial statements.

R&D is very often not stable from year to year, and this creates material and directionally different changes in profit measures. Many companies in the technology and healthcare sectors succumb to this problem. In the Consumer Discretionary space, R&D expense been growing at 8%+ a year over the past 10 years, but with a 25% standard deviation in growth rates. While Technology firms have seen R&D grow at 10% a year the past decade, we measure a 7% standard deviation among growth rates. This issue is material in many other industries such as in the Healthcare, Industrials, Consumer Discretionary, and Energy sectors.

Without capitalizing R&D, a firm’s earnings can be materially understated because the traditional calculation of Net Income does not recognize the firm’s material investments in R&D as part of its operating investments. This violates one of the core principles of accounting, where expenses should be recognized in the period when the related revenue is incurred. R&D investment is an investment in the long-term cash flow generation of the company, and as such should be capitalized, not expensed. Moreover, the incorrect deduction of R&D investments as expenses makes it near-impossible to objectively compare the firm to its peers and even to its own historical performance.

The solution is to consistently capitalize R&D over a fixed period of years across an industry group, and include that in the asset base. The capitalized R&D would be amortized over the same set of years, effectively smoothing the R&D expense into adjusted earnings. Finally, the capitalized R&D would be carried net of accumulated amortization of R&D, allowing for far better Adjusted Return on Assets (ROA’) measures of profitability.

To thoroughly explain why R&D is more an investment than an expense, and the practical implications of such an adjustment, let us split this explanation into two parts, one theoretical, and one implementation and practicality.

Theoretical Rationale for R&D Capitalization – Pharmasset started investing in Harvoni in 2008, and the drug didn’t come to market till 2014, and the failure of Facebook Slingshot likely still helped with other innovation

If a company builds a factory, two things could happen (to be overly simplistic): they could either end up using that factory to produce widgets which create revenue for the business, or shortly after they build the factory, widget 2.0 from a competitor comes out, and they never use their factory. It would then get mothballed and sit underproductive, until the location becomes part of an inner city gentrification and millennials turn it into lofts. In the meantime (pre-lofts), the company may do a one-off impairment of the value of the factory, or they may invest more capex and retool the factory for something else, but no matter what, they’re not going to go back and expense that capex on a periodic basis for the duration of the time it took them to invest in the factory.

Focusing on two types of businesses, if you think of R&D similarly for pharmaceutical or technology companies, it becomes only natural to think that you should capitalize R&D. A company invests for a period of time in a technology, be it the multi-year R&D investment Facebook has made in Oculus Rift or that Gilead/Pharmasset made in Harvoni, and then they generate revenue from that investment.

Fundamentally, the R&D the company invests in during a quarter does not only create revenue for the quarter where that investment took place. Facebook is still generating revenue from the R&D they spent to develop their newsfeed and ad-embedding into the newsfeed years ago. If a company earns revenue from an investment, then that investment should be expensed/amortized/depreciated at the same time the revenue is recognized. This “matching principal” is supposed to be at the core of accounting, though in this and other places, the implementation of accounting fails to reflect the philosophy. If we just expense the R&D, we’re not recognizing the investment that occurred. For this reason, as IFRS highlights, R&D costs for successful developments need to be capitalized.

However, sometimes a company invests in a technology, like Facebook Slingshot (it’s okay, we don’t remember that either), and it fails. Yet, often, future developments do grow from that investment. Certainly some of that technology that went into Slingshot has contributed to the new Instagram story feature, along with some other healthy copying from Snapchat. Similarly, the knowledge Gilead and Pharmasset had from their R&D investment in a multitude of other failed compounds helped them to identify Harvoni’s active compound.

To understand the total investment needed by the company to create the innovation that succeeds, we need to also capitalize the innovation that fails, or else we give the company too much credit for their success in their R&D investment. We’d only be including the R&D that succeeded, so when we looked at the productivity of that R&D we’d think the company should always invest more R&D, since their successful R&D generates so much revenue. That, of course, would lead to more unproductive R&D, since not all their R&D was historically productive.

By capitalizing all of their R&D, we can look at the total value invested to generate today’s revenue, just like how we look at all the PP&E in which U.S. Steel has invested to generate today’s revenue, both unproductive PP&E that currently is sitting idle, and productive PP&E that is at work creating the high value products that U.S. Steel still produces.

Practical Rationale for R&D Capitalization – Boeing’s massive investment in R&D in 2009 makes comparing their year over year profitability and returns pointless without first capitalizing it

Capitalizing R&D actually is more conservative than expensing it. When an asset is capitalized, it doesn’t just end up on the balance sheet and its impact on the income statement vanishes. Once we have a capitalized R&D asset, we then need to amortize that investment over the useful life of the asset, just like we depreciate PP&E. By capitalizing the R&D, we are growing the balance sheet, by the value of that capitalized R&D, which brings down Adjusted ROA and also impacts Asset Turns.

We also still have an “R&D depreciation expense” impacting the income statement, as we amortize the value of that investment over its life. This smooths the artificial volatility of R&D expense and reflects the R&D investment that management would need in order to maintain today’s operations, separate from the growth R&D investment that the company may have invested incrementally in any given year. This is much the same way depreciation expense is a proxy for maintenance capex, but growth capex above that ends up on the balance sheet and then is depreciated over the life of that investment.

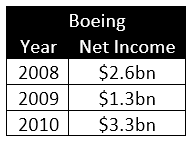

A great example of this is Boeing. It is hard to argue that the multi-year investment they make in a plane like the 787 should be expensed each year, considering they may invest for 10+ years on a plane that then generates revenue for the business the subsequent 20+ years. However, when we do expense, it isn’t just theoretically wrong, it also ends up giving us bad conclusions. Here is the company’s Net Income from 2008-2010:

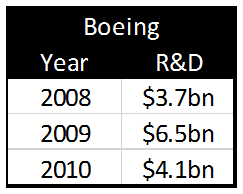

Given the information above, Boeing looks like they had a terrible 2009, which makes perfect sense, since 2009 was the bottom for capital spending globally. But, in actuality, that Net Income trend was entirely related to the timing of Boeing’s R&D investment that was multiple years in the making, and would impact the company for multiple years in the future, not just in the year it was expensed. Here is the company’s R&D expense from 2008-2010:

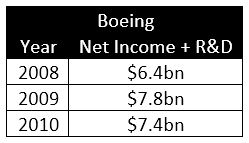

If we adjust their Net Income for that massive volatility in R&D, 2009 was not worse than 2008, it was actually a better year than 2008. For a quick and dirty version of the math, let us just do Net Income + R&D (we’ll show the actual Adjusted Earnings we get in a moment):

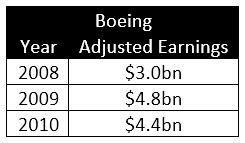

Now of course, as we mentioned above, we need to amortize that R&D investment over its life, we cannot just add it back to Net Income and call it a day. But, even when we include that R&D investment amortization (and the other adjustments we make to clean up accounting distortions), we see the same picture, a company that had substantially better profitability in 2009, not worse:

Again, when we do expense, it isn’t just theoretically wrong, it also ends up giving us bad conclusions. Boeing didn’t have a bad 2009, they invested heavily in 2009 to finish their work on the 787 to position themselves for cash flow generation for the next 15-20 years.

Also, as an aside, the story that Boeing has had phenomenal earnings growth from 2009 to today with Net Income expanding from $1.3bn in 2009 to $3.9bn by 2012 to $5.1bn in 2015 is thrown out when one adjusts for the cyclicality of their R&D investment through their airplane innovation cycle. In actuality, after adjusting for the volatility of Boeing’s R&D investment, Earnings’ has basically ranged from $4.2bn-$4.8bn from 2009-2015, with no actual profitability growth. I’ll now duck as every Boeing bull yells at me about the order book.

More practical examples – Gilead and Danaher

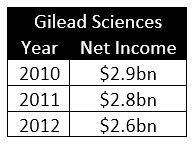

Another excellent example, as previously referenced, is Gilead. As a biotech company, the firm makes considerable investments in R&D as they research various compounds and, through both failure and success, develop life-changing drugs. However, these drugs do not reach patients for years after the research into their basic compounds and chemical structure is done and traditionally expensed, again violating the “matching principle”. This distorts historical profitability, making it impossible to accurately compare their current performance to years prior. For example, here is the company’s Net Income from 2010-2012:

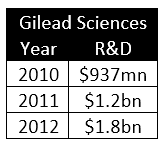

Given just the information above, it appears as if Gilead had seen profitability decline over the course of those three years. However, this trend was in large part related to the firm’s increasing R&D expenses as they began investing more heavily in their pipeline. Here is the company’s R&D expense from 2010-2012:

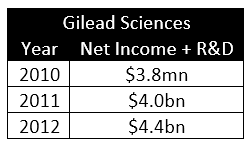

If we adjust their Net Income for that dramatic increase in R&D, the firm has not seen profitability decline, but has instead seen it improve. Again, for a quick version we will begin with just Net Income + R&D:

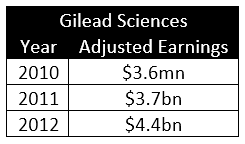

Now, as we’ve mentioned previously, we need to amortize that R&D investment over its life. But even when we include that R&D investment amortization (and the other adjustments we make to clean up accounting distortions), we see the same picture, a company that has improved profitability consistently since 2010:

Again, we can see how failing to capitalize R&D can distort our view of a company’s historical profitability and lead us to make inaccurate conclusions.

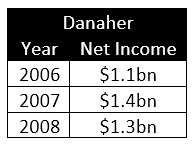

For our third and final example we will look at Danaher. Here is the company’s Net Income from 2006-2008:

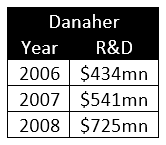

From the information we see above, we may be led to conclude that DHR was just able to maintain its levels of profitability in the face of an oncoming global recession, which may initially seem correct. However, this ignores that material impact of R&D expenses. Here’s the company’s R&D expense from 2006-2008:

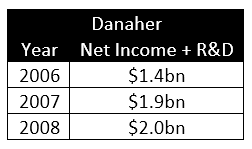

If we adjust their Net Income for that steady increase in R&D, the firm did not see profitability falter in 2008, but instead saw continued improvement. Again, for a quick version we will begin with just Net Income + R&D:

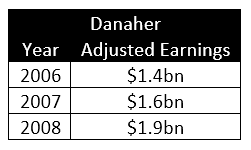

After adjusting for the amortization of R&D investment and other accounting adjustments, we arrive at a similar picture, with improving profitability since 2006:

Danaher didn’t have stagnant profitability from 2006 to 2009, or even a plateau shift in 2007 that stabilized. In fact, they saw earnings growth accelerate each year from 2006-2008. Investors who knew how to see though the distortions in GAAP accounting knew it too, as the stock outperformed the market every year from 2005-2010.

Thus again, we see a different picture than what traditional metrics would show, and we can see how this adjustment helps prevent us from drawing incorrect conclusions.

An Addendum – How do you decide how many years to capitalize R&D for? Does it matter?

If you are going to capitalize R&D, you need to make some estimate for the life of that R&D. When making the determination, the most important issue is that you make sure whatever life you choose for R&D is consistent across a comparable universe. You should not capitalize R&D for four years for one aerospace and defense name, but capitalize it for 15 years for another, or else you lose comparability. The same is true in pharmaceuticals or semiconductors. Of course no one would likely argue the life of R&D in those three industries are the same, but the life of R&D within the industry is likely to be similar.

However, in our framework, we didn’t just pick numbers that “felt right”. We specifically built our analysis off of the work of some of the brightest researchers in the space of valuing Intangible Assets. In particular, part of our framework comes from the analysis of Baruch Lev at NYU, and the work he has done on valuing intangible assets and the persistency of the impact on revenue of a dollar invested in R&D for different industries.

It is unsurprising that after this excellent research, Professor Lev, who is the Philip Bardes Professor of Accounting and Finance at NYU Stern, has moved on to write about the flaws of current accounting standards framework and the issues they create.

Capitalizing R&D solves both theoretical issues with financial statements, and practical issues with financial statement analysis

To recap, R&D is fundamentally an investment. Just because a company needs to invest in R&D to maintain their business doesn’t mean it should be an expense. Companies make investments in their business to maintain their competitive advantages.

CAT invests in a new plant to maintain their operating performance. That doesn’t mean we should expense all their capex in that plant because they had to spend it to maintain their performance, it was still an investment to help produce future cash flows. If an investment is going to impact revenue growth and cash flows for a business beyond the current period, that investment should be capitalized, not expensed.

As such, we should be capitalizing that R&D, and showing it as an asset on the balance sheet. Then, when we run off the R&D investment as the R&D’s benefit to revenue diminishes, we’re still impacting the income statement. This gives a clearer, more conservative view of a company’s true profitability, removing accounting distortions and allowing for fair comparisons between the company’s historical performance and the performance of its peers.