When Cash is Not Cash and Why

Updated April 21, 2020

The Statement of Cash Flows – Is Not

Investors, other analysts, and management often rely on cash flows reported in the financials as a foundation of performance analysis and valuation. Unfortunately, those cash flows are not what they appear to be.

Many use the statement of cash flows (such as “cash flows from operations”) for judging earnings quality, measuring performance, and as key elements of discounted cash flow analysis. The cash flows reported from operations, however, are not truly from operations. Cash flows for financing do not accurately report the company’s financing activities. Cash flows reported for investing simply are not what the financials would purport.

If care is not taken to adjust for the distortions, valuations, etc., then financial decisions based on them are suspect at best.

Cash Flows from Operations

As reported, “cash flows from operations” includes many things that simply aren’t from operations. For instance, one of the major components is changes in working capital. Let’s repeat that… changes in working capital. The fact the word “capital” is used implies correctly that working capital is part of capital invested. In ROIC calculations (return on invested capital), the denominator, invested capital, includes elements of working capital, such as accounts receivable and inventory. And under Uniform Adjusted Financial Reporting Standards, when we talk about “capital”, we are referring to the company’s UAFRS-based (Uniform) assets, and so ROIC is the same as Uniform ROA (ROA’) in that regard.

Despite how the finance world thinks of capital invested, somehow the statement of cash flows does not include changes in working capital as changes in the capital activities of the business. Instead, an increase in working capital, such as inventory, is seen as a negative operating cash flow. The investing activities of the firm, as reported in the statement of cash flows, do not reflect the increase and decrease in the operating assets of the firm, unfortunately. Instead, it’s treated more like an expense, just like a cost of goods sold number.

Here’s a specific example:

Cash Flows, Year One

Imagine you invest money in a new company called Super-Lemon to build a lemonade stand business:

- You provide Super-Lemon capital of $200 during the year

- With that $200, Super-Lemon purchases $100 of fixed capital, a lemonade stand

- Super-Lemon purchases $100 of working capital, in lemons and sugar

- At year end, the business is holding onto those assets, gearing up for the next year’s sales

First question: How much have you and Super-Lemon invested in the Lemonade business? The obvious answer, and also the correct answer, is $200. The $200 of capital invested was spent on fixed and working capital totaling $200. One would have to agree.

Unfortunately, financial statements built under generally accepted accounting principles (GAAP) would not. At the end of the year of investment, Super-Lemon would have to report the following in its statement of cash flows:

| • | Cash Flows Used in Operations | ($ 100) |

| • | Cash Flows Used for Investing Activities | ($ 100) |

According to the statement of cash flows, the operations of the business already lost $100, for nothing other than investing in inventory. Yet, is that really the right way to think of the business? No lemonade was sold at a loss, and no expenses were incurred by the business. Neither analysts nor management would think so poorly of the business.

The fact that Super-Lemon purchased inventory is part of the capitalization of its business, not a cash outflow for shoddy business management. This may partly explain why inventory is called “working capital.” No one calls it “working expenses” or “working expenditures.”

Super-Lemon invested capital of $100 in inventory. It didn’t lose $100 in “operations” as the statement of cash flows would report.

Cash Flows from Operations, Year Two

Roll forward to year two and the problem continues.

- In the flowing year, Super-Lemon sells all $100 of the inventory for exactly $100 in price

- Super-Lemon did not replenish the inventory that it sold

So, Super-Lemon didn’t sell at a profit. In fact, it sold its lemons-and-sugar inventory for exactly what it had paid. In other words, the company liquidated its inventory.

The term, “liquidated” is more than a convenient pun for a lemonade stand case study. In this case, it actually describes the corporate action. When a business sells off its inventory without replenishment, it is left unable to operate. In reality, it is liquidating the business.

Meanwhile, what would the statement of cash flows report?

| • Cash Flows from Operations | $100 |

This financial statement line item attempts to convince us that it was a good year operationally since the $100 lost in the previous year in operations has now been recovered. However, this is not how any manager nor investor would think about the quality of Super-Lemon.

In this case, the $100 of positive operating cash flow was simply a reduction in invested capital. In fact, the “operations” of the business generated no positive cash flow as cost of goods sold matched revenues. Under GAAP, companies in liquidation can show higher operating cash flows when they are actually disposing of working capital (and a multitude of other ways that do reflect reality). In truth, they are really divesting pieces of the company.

Return ON Investment versus Return OF Investment

As a company sells off inventory, any amount received up to the cost of the goods sold is really an act of dis-investment in the business. When the company repurchases inventory, it is then reinvesting capital called working capital.

Reductions in inventory represent the potential return OF capital. Meanwhile, any cash generated above and beyond the cost of inventory could be considered a return ON capital. Good cash flow analysis will always highlight this distinction and adjust for it.

Far More Than Working Capital Issues

As stated, investments and disinvestments in working capital are notoriously missing from the investing activity section of the statement of cash flows. Other problems exist too.

One issue is the treatment of research and development expenses in the cash flow statement. While R&D expenditures are clearly investments in the future of the organization, it is nowhere to be found in the so-called “Investing” section of the statement of cash flows. It improperly remains a reduction of cash flow from operations, which makes little sense.

When a business reduces its R&D activities, it will report increasing cash flows from operations. When a business steps up its investments in R&D for the future of the company, those same financials will report lower operational cash flows that year. It is really the antithesis of the way an investor or manager would think about the activities of an innovative business.

Renting Activities

A more complex example occurs when firms rent in order to acquire assets for use in the business. The actual rental payment is a financing cash flow in lieu of purchasing the asset. Renting assets is essentially a substitute for buying assets with debt.

In some cases, the accountants even recognize this economic reality and require firms to record the asset on the balance sheet along with an assumed debt balance indicated by the rental payment levels. When that happens, in good common sense, the operating, investing, and financing cash flows are recorded in a sensible way in the categories of the statement of cash flows.

However, the accounting rules that require the “booking” of rented assets are very easy to avoid. In other words, it is fairly easy for a company to structure its rental agreements such that it won’t recognize rented assets as balance sheet assets if management doesn’t want to. This can be accomplished by the rental agreement structure alone, with little or no change to the annual cash expenditures to rent the asset. The assets remain “off-balance-sheet” as does the implicit associated debt.

When the capitalization of rented assets is avoided, the cash flow statement reflects rent expense as operating costs with no impact to financing or investing activities, despite the obvious nature of “renting” an asset. So, two companies with nearly identical rental activities can show financial statements with entirely different cash flow statements.

So, Interest Expense is Not for Financing Debt?

One of the great mysteries of the common-sense universe is how cash flows for financing activities can include dividends to shareholders but not include interest paid on debt. “Cash used for/from financing activities” as shown in the financials has little to do with the economic reality of business financing. How can it, if it doesn’t even include interest costs to service capital raised through debt?

Many other items are missing or strangely included as financing cash flows that are just as mysterious as this. The cash flow levels reported simply do not represent how managers think when examining how a company finances its business. It certainly doesn’t represent how investors think when considering a firm’s capitalization.

Double-Entry Accounting Means Double the Trouble

Every debit has an equal and opposite credit. If the cash flow statement incorrectly picks up investing activities, it is also incorrectly classifying something else. If investing activities are too high, it means operating and financing activities are in error in the opposite direction.

Other more notorious misclassifications in the cash flow statement can come from pension accounting, stock option accounting, and asset write-offs.

Implications of the Cash Flow Statement Misclassifications

In order to understand the true economics of a business, understanding the nature of the cash flow activity is a necessity. One must reclassify cash flow activities in ways that reflect their true nature.

Operational inflows and outflows should be treated as operational cash flows. When capital is invested in a business, they ought to be identified accurately as investing activities. Debt and capital raising decisions should be reflected in financing activities. It seems so obvious, but errors occur in analyses every day.

Examples included in this article show just how directionally bad the distortions can be. With just a small set of adjustments, big differences arise. The differences are not only material, but inconsistently distorted from year to year, even across companies within the same industry.

Be very wary of financial and strategic analysis that does not overtly take these issues into consideration. Study the true nature of the cash flows of the business. Question common thinking and replace it with common sense. When obvious distortions are cleared, we can reveal the true nature of the business and a superior starting place for financial decision-making.

Appendix

Cash Flow Analysis Examples

In each of the following examples, we show actual operating cash flow calculations UAFRS-based earnings (E’) is the computation for the real operating cash flows of a company. The computation begins with net income, makes several important adjustments, and finally tabulates the earnings’.

Shown immediately below that line is cash flow from operations (CFFO). This is the amount, exactly as reported in the GAAP audited financial statements of the firm.

In each example, note the material differences between E’ and the reported CFFO; however, of larger concern is how year-to-year changes in CFFO can be directionally inconsistent with changes in the E’. The problems with CFFO are mentioned in the article, “When Cash Is Not Cash and Why.”

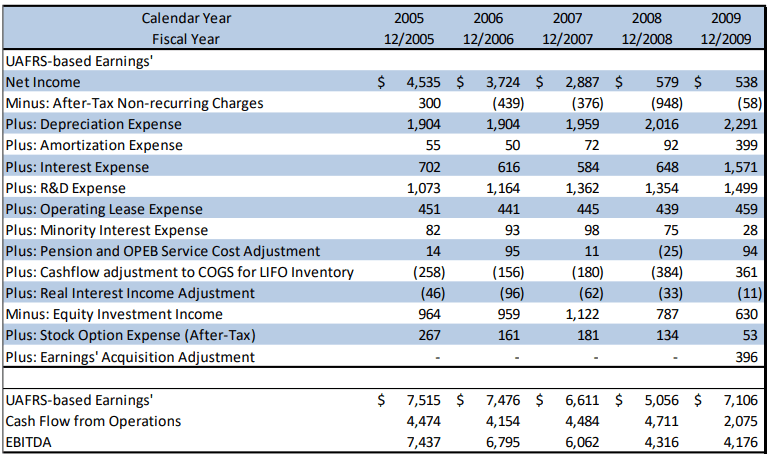

Dow Chemical (DOW:USA)

- From 2006 to 2007, DOW’s real E’ dropped 9%. Meanwhile, CFFO reported an increase of 8%

- Again from 2007 to 2008, E’ dropped 24% while CFFO increased 5%

- From 2008 to 2009, DOW saw increasing real E’, while CFFO reported a decrease, owing to its misclassifications

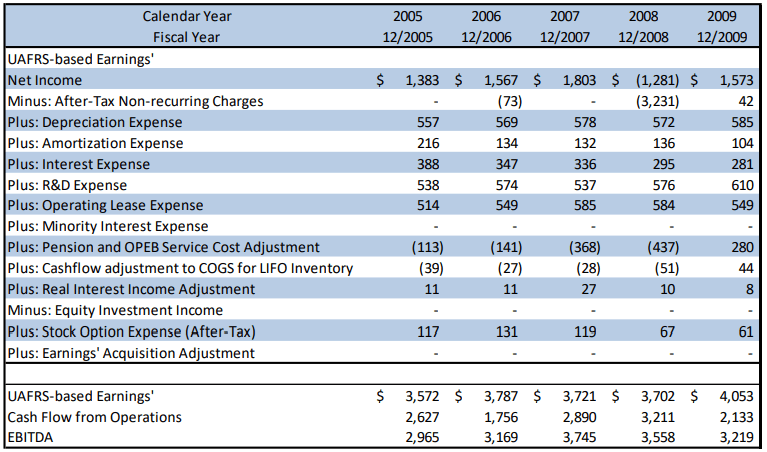

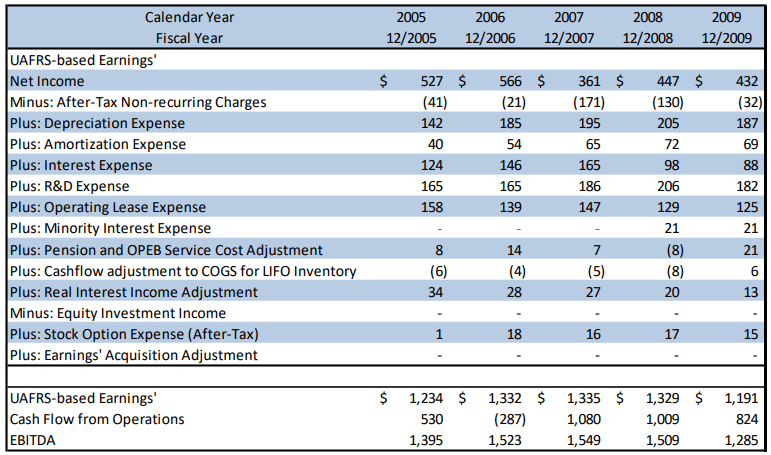

Northrop Grumman Corporation (NOC:USA)

- From 2005 to 2009, real E’ showed steady levels at Northrop Grumman

- Meanwhile, reported CFFO showed wild year-to-year fluctuations, jumping up and down throughout the period with no consistency

- Dramatic increases in rent and R&D contributed to the problems with CFFO. Also, pension expenses that include significant cash flows need to be removed from any operational cash flow calculation; otherwise, it can be greatly distorted, as in the reported CFFO calculation

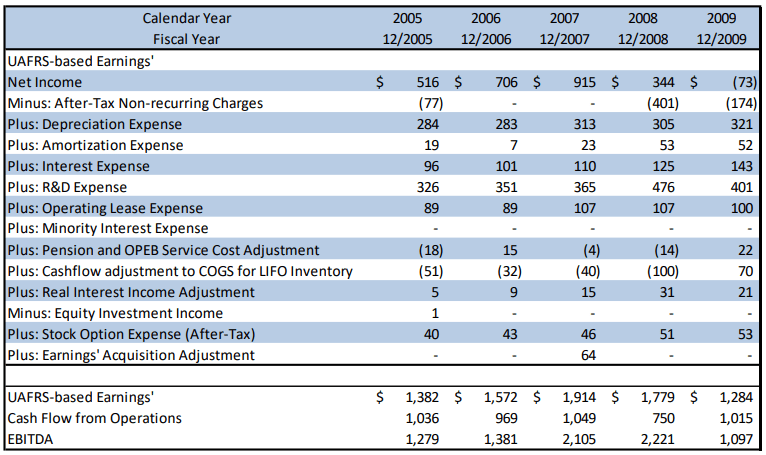

TextronInc.Inc. (TXT:USA)

- From 2007-2008, Textron’s real E’ slightly decreased, while its reported CFFO decreased massively

- The following period, 2008-2009, Textron’s E’ decreased nearly 30% and its CFFO increased 35%

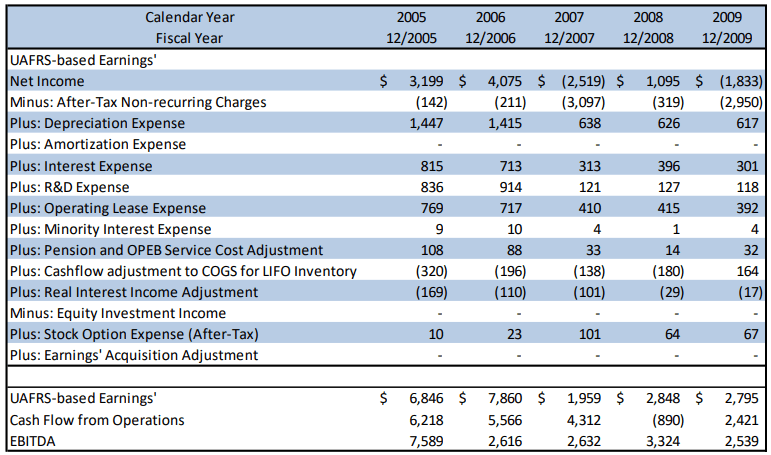

Tyco International (TYC:USA)

- From 2005-2009, TYC’s E’ and CFFO moved in different directions in every year but one. Note in from 2007 to 2008 E’ increased 45% while CFFO decreased 121%

- The discrepancies could stem from any one of several adjustments that CFFO would need to make, but does not, in order to be reliable

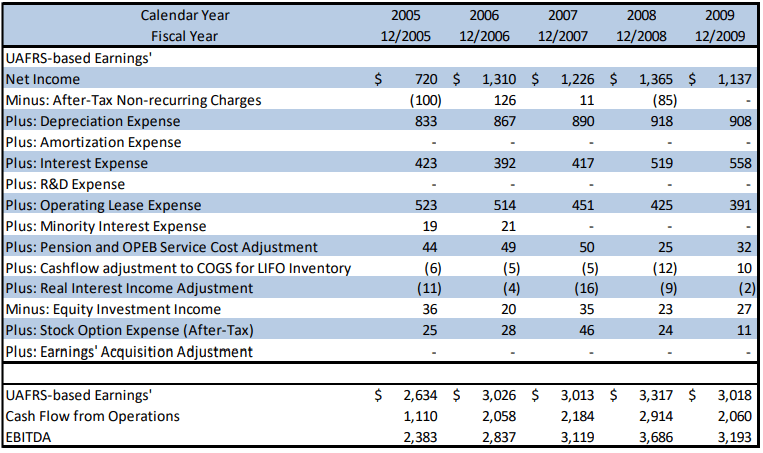

Pitney Bowes Inc. (PBI:USA)

- For the period 2005-2009, PBI’s real E’ have been steady. However, reported CFFO shows massive swings

- Changes in working capital balances are investing and disinvesting activities. These changes are included in CFFO, making it an unreliable figure as it shows a volatility in operations that doesn’t really exist

CSX Corp. (CSX:USA)

- From 2005-2009, CSX’s real E’ has been relatively stable

- Meanwhile, reported CFFO has been volatile, owing to how investing and financing activities are buried in the calculation

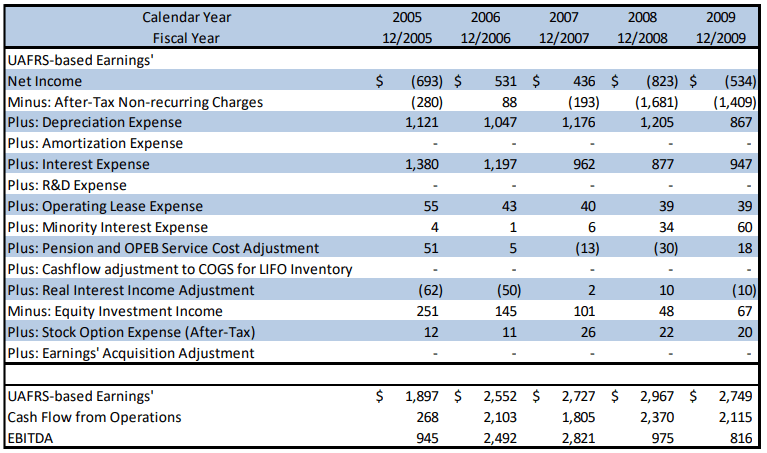

El Paso Corp (EP:USA)

- Differences in real E’ and those reported for El Paso stem from a number of issues, not the least of which is the inclusion of interest expense in CFFO as operations instead of financing

- From 2005-2007, EP’s E’ remained stable while CFFO increased significantly