The brains behind ‘Barbarians at the Gate’ are back with a new target

Starboard Value has a proven history of guiding corporate transformations that have been lucrative for investors.

Like most activist funds, it invests in companies to make changes rather than waiting for the companies to change themselves.

Today, we’ll use Uniform Accounting to perform a detailed portfolio audit on Starboard’s largest holdings, and see what you could learn from the legendary activist.

Also, read to the end to see a detailed Uniform Accounting tearsheet of the fund’s largest holding.

Investor Essentials Daily:

Friday Portfolio Review

Powered by Valens Research

Starboard Value is a notoriously successful hedge fund. Before diving in, let’s start with some backstory…

Peter Cohen is one of the most respected names in the hedge fund universe, but he doesn’t get discussed much in the modern era.

He is most famous for his involvement in the leveraged buyout of RJR Nabisco that was memorialized in Barbarians at the Gate. After holding several senior leadership roles in Wall Street, in particular at what eventually became Lehman Brothers, Cohen founded Ramius Capital in 1994. It went on to become a world-renowned asset manager.

Recognizing that the two independent hedge fund and investment banking worlds were starting to converge, in 2009 Ramius acquired and took the name of Cowen & Company, the investment bank, while also usurping Cowen’s hedge fund operations.

The result was a diversified and powerful Wall Street institution that remains a significant player to this day.

Cohen always had a sharp eye for talent, and so in 2002, he helped found an activist investor firm within Cowen, which eventually became Starboard Value.

Activist firms approach investing with an even more aggressive strategy than typical hedge funds. They attempt to use their investments as influence over the management of a company, pushing or even threatening them with a takeover to take certain actions.

These actions are sometimes at odds with the interests of shareholders, as they can push management teams to prioritize short-term profitability over long-term growth. One particularly ruthless activist fund we’ve covered before, Elliott Management, has made a habit of threatening to use its voting power to publish hit pieces on the CEOs of the companies.

Starboard Value was eventually spun off from the Cowen umbrella into its own company, as the firm no longer needed Cowen’s support. By this point, it was already well established as an activist heavyweight.

Since then, it has had great success. Starboard’s notable deals include pushing AOL to fundamentally change its operations in 2011 and orchestrating the OfficeMax and Office Depot merger in 2013.

Now, in 2021, the company has picked a new fight with Willis Towers Watson (WLTW), a company that also seeks to help management teams improve operations. Following an attempted merger with AOL that was then struck down by regulators, Starboard believes it can help Willis Towers Watson charter a new course.

Jeff Smith, who sits atop the helm at Starboard, believes that his influence can push Willis Towers Watson stock to be about 85% higher over the next three years. Only time will tell if this is to be the case, but what we do know is that Starboard has an impressive record of finding undervalued companies and pushing them to improve their operations or optics to create value.

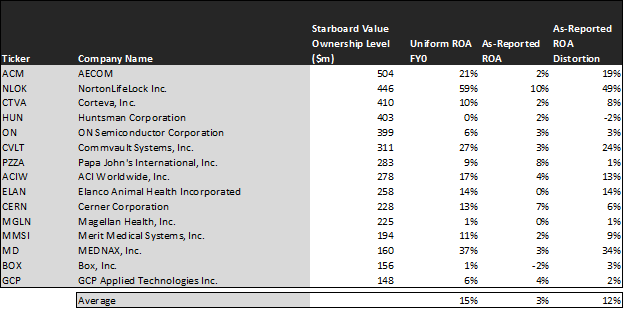

Let’s check up on Starboard’s top fifteen holdings, using Uniform Accounting, to evaluate if its claim of finding companies unappreciated by the market with great potential holds up.

With an average as-reported return on assets (“ROA”) of 3% and a Uniform ROA of 15%, Starboard targets companies with lukewarm-at-best returns.

After all, if it were to target productive technology or healthcare firms with 30% or 40% ROAs, how much of an improvement to operations could its activism really cause?

The most economically productive firm held by Starboard is NortonLifeLock (NLOK), formerly called Symantec, which suffered in 2018 with an audit investigation announcement that led to its stock price shedding a third of its value.

With the Starboard investment, Starboard Value Head of Research Peter A. Feld joined the board and guided the company out of its troubled times. The company retooled by selling its enterprise business to Broadcom and started investing heavily in its consumer business.

Most investors, however, would miss the beauty of the transformation, given that NortonLifeLock’s as-reported ROA is only 10%. In reality, however, the company boasts Uniform ROAs of 59%, with analysts expecting even better productivity over the next several years.

Starboard’s specialty, the firm claims, is in finding undervalued companies. While the degree to which an investment may be undervalued may be difficult to quantify, here at Valens, we have a few tools that can reveal this mispricing.

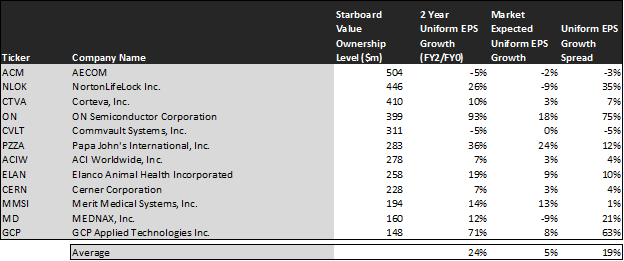

The chart below compares analyst-expected returns with market-expected returns. When there is a severe dislocation between the two, it can often mean the market is failing to understand something about a company. See for yourself:

This chart shows three interesting data points:

- The 2-year Uniform EPS growth represents what Uniform earnings growth is forecast to be over the next two years. The EPS number used is the value of when we take consensus Wall Street estimates and we convert them to the Uniform Accounting framework.

- The market expected Uniform EPS growth is what the market thinks Uniform earnings growth is going to be for the next two years. Here, we show by how much the company needs to grow Uniform earnings in the next 2 years to justify the current stock price of the company. If you’ve been reading our daily analyses and reports for a while, you’ll be familiar with the term embedded expectations. This is the market’s embedded expectations for Uniform earnings growth.

- The Uniform EPS growth spread is the spread between how much the company’s Uniform earnings could grow if the Uniform earnings estimates are right, and what the market expects Uniform earnings growth to be.

The market has priced these companies to grow their earnings base by just 5% over the next two years, exactly in line with average corporate earnings growth.

Analysts, who spend every day studying market conditions and management initiatives to forecast earnings and growth, have a more bullish view. They, on aggregate, are forecasting an average earnings growth of 24% over the next two years.

This creates a favorable setup for investors. Should these analyst estimates come to pass, investors may be pleasantly surprised, initiating buying sprees that push the stocks higher.

One notable example is NortonLifeLock. As mentioned earlier, Starboard encouraged the company’s rebranding and a number of other management initiatives to better streamline the business.

As it is still a work in progress, the market hasn’t fully caught on. While the market is pricing Norton to shrink its earnings by 9% over the next two years, analysts recognize that Starboard’s influence will be a positive catalyst for the firm. Hence, they predict earnings growth of 26% over the same period.

Looking at Starboard’s largest holding, AECOM (ACM), shows a different story. But Starboard’s activism with AECOM has not been unsuccessful. Since its 2019 investment in the engineering firm, shares have more than doubled in value, hence becoming the fund’s largest holding.

Currently, the investment outlook for AECOM seems grim, as analysts expect earnings to shrink. The market, however, is less pessimistic, creating an unattractive setup for investors. In fact, Starboard and AECOM faced an extensive fight over board member seats, suggesting a fair degree of animosity between the activist and the company.

We wouldn’t be surprised to see Starboard liquidate its AECOM position given its stock price run-up and the prolonged tension.

Overall, Embedded Expectations Analysis clearly shows that Starboard has a knack for finding undervalued companies full of hidden potential.

With access to the Valens Research UAFRS database, you could also see Embedded Expectations Analysis for over 25,00 publicly traded companies. Learn more about how to get access here.

Read on to see a detailed tearsheet of Starboard’s largest holding.

SUMMARY and AECOM Tearsheet

As Starboard Value’s largest individual stock holdings, we’re highlighting AECOM’s tearsheet today.

As the Uniform Accounting tearsheet for AECOM (ACM:USA) highlights, its Uniform P/E trades at 26.5x, which is above the global corporate average of 24.3x, but above its own historical average of 19.9x.

High P/Es require high EPS growth to sustain them. In the case of AECOM, the company has recently shown a 12% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that, in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, AECOM’s Wall Street analyst-driven forecast is for EPS to shrink by 44% in 2021, followed by a 61% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify AECOM’s $63 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 1% annually over the next three years. What Wall Street analysts expect for AECOM’s earnings growth is below what the current stock market valuation requires in 2021, but is above that requirement in 2022.

Meanwhile, the company’s earning power is 4x above the long-run corporate averages. Additionally, cash flows and cash on hand consistently exceed nearly 3x its total obligations—including debt maturities, capex maintenance, and dividends. Moreover, AECOM’s intrinsic credit risk is 90 bps above the risk free rate. Together, these signal low operating and credit risks.

Lastly, AECOM’s Uniform earnings growth is below peer averages, but the company is trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research