Why the heavyweight activist hedge fund’s latest move is raising eyebrows

Among the hedge fund universe, Paul Singer’s Elliott Management employs some of the most aggressive tactics out there. Elliott has toyed with governments, uprooted the largest corporations, and struck fear into the hearts of management teams.

Singer’s latest investment has a different tone to it, and it’s raising eyebrows. Today, we will try to better understand the fund’s strategy using undistorted Uniform Accounting metrics.

In addition to examining the portfolio, we’re including a deeper look into the fund’s largest current holding, providing you with the current Uniform Accounting Performance and Valuation Tearsheet for that company.

Investor Essentials Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

Those who have been reading the Investor Essentials Daily for some time may remember our prior piece on Elliott Management.

Hedge funds normally operate in the background, cashing in on some brilliant strategy they’d prefer to keep behind closed doors. Elliott, in contrast, is more like the Kool Aid Man: Kicking through walls, grabbing everyone’s attention, and making a scene.

As a result, the fund shows up in the news rather frequently, and it appears Elliott is about to stir the pot once more. It’s what it does best.

But first, some background.

Elliott Management is the pet project of lawyer-turned-investor Paul Singer. His early success came from a willingness to actually read the fine print, potentially a byproduct of his legal roots.

His claim to fame, however, was his activist investing strategy.

Rather than passively buying stock in companies he believed in, Singer bought stock in companies that were mismanaged and underperforming. And he didn’t just buy a few shares. He would buy a large enough stake to have influence over the board of directors.

It is for this stage of the process that Singer earned his reputation as “the most feared investor in the world”.

Sometimes he’d launch PR campaigns to get the CEO fired. Sometimes he’d force a sale of the firm to a competitor, or sell off underperforming assets to improve the short-term profitability (at the expense of longer-term goals).

Elliott was ultimately behind the restructurings of WorldCom, TWA, and Enron. The fund fought hard to oppose a Samsung merger, eventually leading to the impeachment of the South Korean President. But none of Singer’s work was as jaw-dropping as his exploitation of countries on the brink of collapse.

In 1999, Elliott bought $600 million worth of Argentine government bonds for pennies on the dollar. The country got hit by several economic collapses that involved violent protests, mass poverty, and government corruption that eventually caused most of the other bondholders to back out of the holding pool, but not Elliott.

Elliott waged a decades-long legal battle as it attempted to seize Argentinian assets, eventually culminating in a guns-drawn altercation as the hedge fund tried to seize an Argentinian naval vessel.

Eventually, Singer and Argentina reached a settlement in 2016 that netted the fund 1,270% on its investment. The message to the world was clear: Paul Singer never backs down.

These aggressive tactics have paid off. Singer’s fund has had only two negative years, and every dollar invested at its onset would today be worth nearly $200.

Knowing this, imagine what Dropbox (DBX) CEO Drew Houston felt last month as he learned that Elliott Management had quietly amassed a 10% stake in the firm, becoming the second largest shareholder.

You might be surprised to learn that Houston probably felt fine. That’s because this time, the circumstances seem to be different.

Houston retains more than 70% voting power within Dropbox’s corporate structure. A 10% stake earns Elliott a seat at the table, but it’s far from the head. The fund won’t be able to draw on its usual playbook of uprooting management or driving a radically different M&A strategy.

This move leaves the corporate world scratching its head. Singer is unlikely to suddenly adopt an invest-and-rest philosophy. He will certainly attempt to enact change, but this time, there are a few theories as to how it will happen or what it will look like.

Despite Houston’s ownership level, we can piece together some of Elliott’s reasoning.

We’ve written about the at-home revolution extensively. Companies that facilitated a more pleasurable, productive, and fulfilling life at home have seen their stocks soar while others have stagnated.

Dropbox, which provides consumer cloud storage and file sharing, should have been along for the ride. But since its 2018 IPO, the stock is only up 7%. ROA in 2020 was a lackluster 3%. The company seems like it could use a kick in the rear to change things up.

In reality, once we look at the company on a Uniform accounting basis, we see a true Uniform ROA of 18%.

Given the puzzling nature of this particular investment, let’s look at Elliott’s holdings on a higher level. We have conducted a portfolio audit of the fund’s thirteen largest holdings that are traded on American exchanges.

Take a look at its portfolio:

Even when looking at this set of companies using Uniform accounting metrics, which remove distortions inherent to the Generally Accepted Accounting Principles (GAAP), we see a collection of companies that return below the American corporate average.

If any other fund put its investors’ capital in the hands of these lackluster firms, we’d raise an eyebrow. But because we are evaluating Elliott, these metrics show us that the fund is keeping to its bread-and-butter tactics.

While Elliott’s largest holding Dell (DELL), in reality, has a robust operating profit of 41%, many of these holdings hover near or below corporate averages. Evergy (EVGR), of which Elliott holds $676 million, is an underperforming renewable energy firm that hasn’t even generated returns above the cost of since 2005.

Moreover, it actually overstates its margins on an as-reported basis. Elliott acquired a massive stake in the firm early last year, and immediately began to dictate an aggressive M&A strategy to kickstart growth.

Nielsen (NLSN) is another prime example. Its Uniform ROA has been in a steady nosedive since 2010, falling from 40% levels to just 13% in 2020. Elliott has appointed its own board member and facilitated a spinoff of its media business in an attempt to correct the course.

Beyond just looking at economic productivity and ways the business could be improved, Elliott looks long and hard at valuations before investing. The fund has no business investing in firms that are already expensive because they typically already have performance already baked into what the market expects.

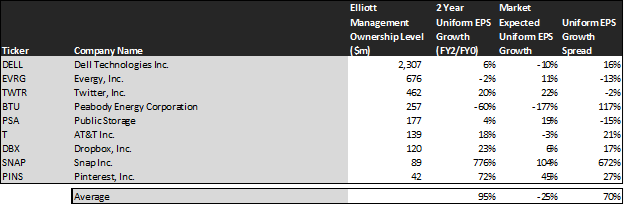

Take a look at the following chart, which shows the market expectations for earnings to justify the current share prices:

This chart shows three interesting data points:

- The 2-year Uniform EPS growth represents what Uniform earnings growth is forecast to be over the next two years. The EPS number used is the value of when we take consensus Wall Street estimates and we convert them to the Uniform Accounting framework.

- The market expected Uniform EPS growth is what the market thinks Uniform earnings growth is going to be for the next two years. Here, we show by how much the company needs to grow Uniform earnings in the next 2 years to justify the current stock price of the company. If you’ve been reading our daily analyses and reports for a while, you’ll be familiar with the term embedded expectations. This is the market’s embedded expectations for Uniform earnings growth.

- The Uniform EPS growth spread is the spread between how much the company’s Uniform earnings could grow if the Uniform earnings estimates are right, and what the market expects Uniform earnings growth to be.

This chart may be the best tell-all for why Elliott Management is so successful.

The companies Elliott holds are priced for their earnings to shrink over two years, while analysts who work every day to project sales and market conditions think earnings will double on average.

Even when excluding the clear outlier, Snapchat (SNAP), there is around a 20 percentage-point spread between what analysts expect and what the market expects.

At the end of the day, we at Valens believe an under-valued portfolio like this is what all investors should strive to achieve, because it opens the door to positive surprises that investors weren’t already expecting.

Elliott gets there in quite a unique way. Whereas most investors seek to find “hidden gems” that have not yet been discovered, Elliott chooses to find rough stones and polish them into gems itself.

To read more about Elliott’s largest holding, see the Dell Technologies tearsheet below.

SUMMARY and Dell Technologies Tearsheet

As Elliott Investment Management’s largest individual stock holding, we’re highlighting Dell Technologies’ tearsheet today.

As our Uniform Accounting tearsheet for Dell Technologies Inc. (DELL:USA) highlights, its Uniform P/E trades at 10.2x, which is below the global corporate average of 23.7x, but around its own historical average of 9.1x.

Low P/Es require low, and even negative, EPS growth to sustain them. That said, in the case of Dell Technologies, the company has recently shown a 14% Uniform EPS growth.

While Wall Street stock recommendations and valuations poorly track reality, Wall Street analysts have a strong grasp on near-term financial forecasts like revenue and earnings.

As such, we use Wall Street GAAP earnings estimates as a starting point for our Uniform earnings forecasts. When we do this, Dell Technologies’ Wall Street analyst-driven forecast is a 11% EPS growth in 2022, followed by a 1% EPS growth in 2023.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify Dell Technologies’ $92 stock price. These are often referred to as market embedded expectations.

What Wall Street analysts expect for Dell Technologies’ earnings growth is above what the current stock market valuation requires through 2023.

The company’s earnings power is 7x corporate averages, and cash flows and cash on hand consistently exceed obligations, signaling that there is low cash flow risk to the company’s operations and credit profile in the future.

To conclude, Dell Technologies’ Uniform earnings growth is in line with averages, but the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research