This energy company can’t afford to ignore green energy any longer

Although this energy producer tells you it is going green, the going is slower than you might think.

If the fossil fuel market gets regulated more heavily in the United States, it may be in trouble. By looking at its upcoming debt obligations, you’ll see exactly why.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

In the last edition of our portfolio review series, we highlighted the iShares Global Clean Energy ETF.

To summarize, as a new IPCC report linking severe weather events around the entire world directly to anthropogenic climate change, which our New England readers have experienced first-hand after the landfall of Hurricane Henri, investors are increasingly looking into the ‘carbon-neutral future.’

From the builders of wind turbines to the developers of solar panel management software or pure-play clean energy producers, ICLN gives investors access to the most successful clean energy firms around the world.

Most of the easy-choice clean energy producers have a spot on the ICLN list. But there is one company that, if you bought its marketing materials, would seem to be an odd exclusion.

That company is the #5 U.S. listed electrical utilities name in terms of market cap, revenue, and EBITDA: American Electric Power (AEP).

Its website homepage shows an electric car charging up, and their news releases page is full of articles about their new wind and solar farms, sustainable finance reports, and ongoing divestitures of their fossil fuel assets.

Despite its “greenwashing” signals, American Electric Power probably doesn’t have a spot on the ICLN list because it isn’t clean enough. Nearly half of its generation fleet still runs on coal, and 70% uses fossil fuels in some regard. Less than 20% if its generation comes from truly renewable sources like wind and solar.

Even its long-term plans are hardly in-line with the other ICLN names. By 2030, the company projects that 40% of its fleet will still run on fossil fuels.

The American government has typically been lenient with the fossil fuel industry, but if the current political makeup of government persists into the middle of the decade, regulatory pressure may begin to strangle the fossil fuel business. Ideas like carbon taxes can very quickly change not just the investor outlook, but also the cash flow obligations that American Electric Power has forecasted.

The major rating agencies, however, don’t appear to be concerned. S&P rates the company as an A-, and Moody’s rates it as Baa2. Although Moody’s is a bit more bearish than S&P, both ratings are generally investible.

Unlike the major agencies, we use Uniform accounting metrics. This gives us a more holistic understanding of a company’s finances. Unsurprisingly, we see a different picture than them.

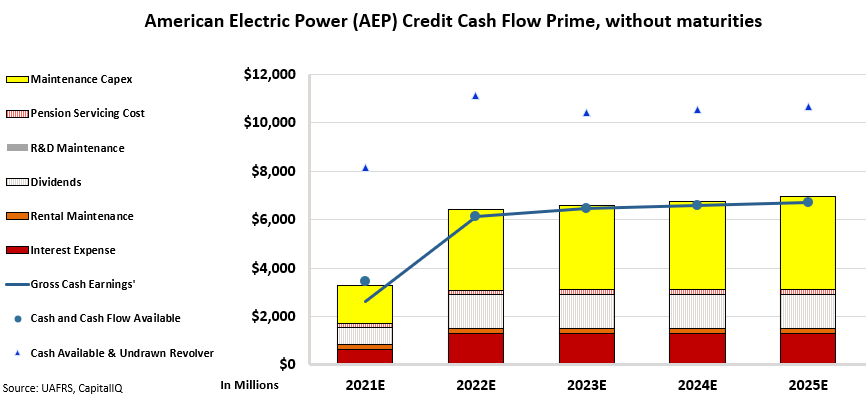

Utility companies typically take on a lot of debt. Using our Credit Cash Flow Prime (CCFP) analysis tool, we can quickly visualize how flexible a company is in the face of unexpected difficulties.

The blue dots represent the cash available to the company, while the blue line represents Uniform earnings. The bars represent the set of obligations the Company must pay off in each subsequent year, with the most easily divertible obligations like maintenance capex stacked towards the top, and unbreakable contractual obligations like debt maturities sitting near the bottom.

Take a look at the five-year CCFP chart for American Electric Power below, without considering debt maturities. In this case, we are assuming that the firm is able to easily and favorably refinance its debt obligations well into the future.

As you can see, even in this rosy scenario, the company has no cash buffer. It is barely able to fully maintain its equipment. See for yourself:

Had this been the real picture, we’d already be raising eyebrows. To turn an economic profit, American Electric Power would need to defer some of its maintenance expenses, allowing equipment to age, and potentially break in the future.

For a utility company, this would be bad. Maintaining the health of aging equipment is paramount to not just future profits, but to worker safety.

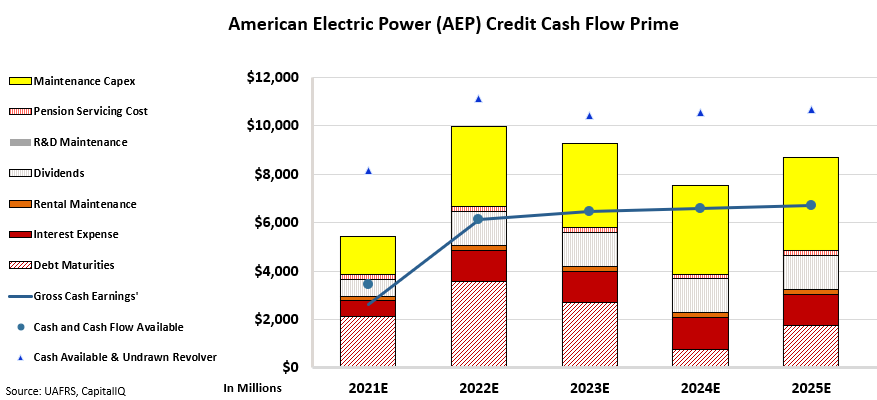

Now let’s look at the more realistic scenario, where American Electric Power cannot easily refinance. Once you consider its debt maturity headwalls, the picture goes from underwhelming to rather dire. See for yourself:

Not only would the company need to defer nearly all of its maintenance capex, it won’t have enough cash to maintain its employee’s pension plans or pay investors the full dividend management has guided for.

Moreover, a heavy ramp into wind and solar facilities will require a lot of capital expenditure, which, under tight finances, may not be as available as management hopes. To meet those goals, the company may need to take on additional leverage, or refinance at unfavorable rates.

As a result, this company receives a Valens credit rating of HY2+, equivalent to a Moody’s B1 or S&P B+ rating, which in the credit world is considered highly speculative.

Equity investors should take note of this sort of analysis. Here at Valens, we’ve learned that studying a company’s debt profile reveals a name’s financial health, which has a direct impact on equity prices.

But that’s just one part of a multi-faceted story. To assemble our Conviction Long List, we also study embedded market expectations, conduct diligent fundamental research, study managements’ incentive structures, and even employ auditory analysis tools to identify when management might be excited about a topic during their earnings calls – or when they might not be telling the whole truth.

Learn how to get access here.

SUMMARY and American Electric Power Company, Inc. Tearsheet

As the Uniform Accounting tearsheet for American Electric Power Company, Inc. (AEP:USA) highlights, the Uniform P/E trades at 40.7x, which is above the global corporate average of 21.9x and its own historical average of 38.9x.

High P/Es require high EPS growth to sustain them. In the case of American Electric Power, the company has recently shown 12% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, American Electric Power’s Wall Street analyst-driven forecast is a 9% EPS decline in 2021 and an 11% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify American Electric Power’s $91 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 14% over the next three years. What Wall Street analysts expect for American Electric Power’s earnings growth is below what the current stock market valuation requires through 2022.

Furthermore, the company’s earning power is below the long-run corporate average. Moreover, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals high credit and dividend risk.

To conclude, American Electric Power’s Uniform earnings growth is in line with its peer averages, but the company is trading above peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research