A PE firm helped this retailer get on its feet. The credit market isn’t impressed

Private equity (PE) and business development companies (BDC) are often getting lots of criticism as they benefit from tax loopholes.

However, there is also a good number of instances where these firms are highly helpful. They help companies become more efficient and more profitable as they invest and sponsor them.

A great example of this is Academy Sports and Outdoors (ASO). The company was bought by the well-regarded PE firm KKR in 2011 and went public in 2020.

The PE firm has had a significant positive impact on the retailer’s efficiency, profitability, and its balance sheet health.

Yet, credit rating agencies seem to think otherwise due to rising concerns for a recession in the near future.

Let’s take a look at the company from the Uniform Accounting lens and see if a possible recession might stress the payment of its obligations.

We can use Uniform Accounting to put the company’s real profitability up against its obligations and decide for ourselves the true risk of this business.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

PE firms and BDCs are often the subjects of criticism due to perceived benefits from tax loopholes.

But it’s essential to recognize that these firms can also be highly beneficial, helping companies become more efficient and profitable through their investments and sponsorships, as well as providing alternative investment opportunities to investors.

A perfect example of such a success story is Academy Sports and Outdoors (ASO), which was acquired by the famous PE firm KKR in 2011 and went public in 2020.

The company is a retail chain that specializes in providing sporting goods, outdoor equipment, and home entertainment products.

KKR picked the perfect time to cash out on its investment in the company. ASO was a private company sponsored by KKR, and the PE firm helped the company turn into a more efficient retail chain.

Back in 2020, we were at the height of the at-home revolution. Because of the pandemic, everyone was stuck in their homes and was looking for ways to make their homes a better place to live.

Chains like ASO helped people furnish their homes with more entertainment products and the company significantly benefited from doing so.

Additionally, at-home sporting goods and outdoor equipment were doing well as gyms were closed or people were hesitating to go into crowded indoor spaces at that time.

Seeing that opportunity, KKR prepped the company for an IPO, and it sold its entire remaining stake in 2021.

Now, as we have a recession looming, the retail chain is likely to face some tougher years.

That’s why credit rating agencies have soured on the company and totally forgot about the improvements the company had.

S&P rates the company “BB”, implying that it is a high-yield company with significant credit risk and that it has around a 10% chance of going bankrupt in the next few years.

Our opinion is not in line with the rating agencies as we saw that after leaving the private world, ASO has a clean balance sheet.

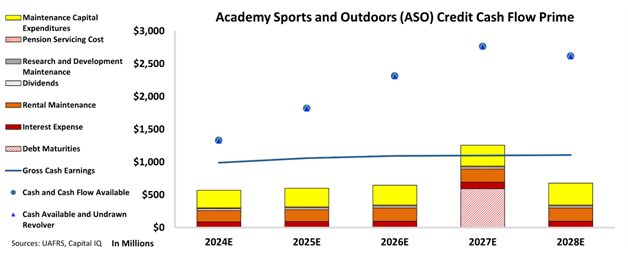

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (“CCFP”) to understand how the company’s obligations match against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart shows that ASO’s cash flows are more than enough to serve all its obligations going forward.

The chart shows that the most recent debt maturity the company has is in 2027. When compared to the company’s cash flows, this debt maturity is not concerning at all.

It can either pay it down easily with its huge cash available or refinance at appealing rates later in time.

In addition, the company has a massive spread between its cash flows and its obligations. This provides significant flexibility for the company in the case of a recession in the near future.

Because of these factors, at Valens, we rate the company “IG4+”. This rating ensures that the company is placed within the investment-grade basket and implies only around a 1% chance of default in the next few years.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Academy Sports and Outdoors, Inc. (ASO:USA) Tearsheet

As the Uniform Accounting tearsheet for Academy Sports and Outdoors, Inc. (ASO:USA) highlights, the Uniform P/E trades at 9.0x, which is below the global corporate average of 18.4x but above its historical P/E of 7.8x.

Low P/Es require low EPS growth to sustain them. In the case of ASO, the company has recently shown a 2% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations, that in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, ASO’s Wall Street analyst-driven forecast is for a -2% and 8% EPS growth in 2024 and 2025, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify ASO’s $51 stock price. These are often referred to as market-embedded expectations.

Furthermore, the company’s earning power in 2022 was 4x the long-run corporate average. Moreover, cash flows and cash on hand 3x its total obligations—including debt maturities and capex maintenance. The company also has an intrinsic credit risk that is 110bps above the risk-free rate.

Overall, this signals a low dividend risk.

Lastly, ASO’s Uniform earnings growth is above its peer averages and is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research