“Boring” doesn’t mean risky. This wire company is minting cash

The United States has underinvested in infrastructure for many years. As the pandemic subsided, companies couldn’t push off investments anymore, so we’re finally starting to see reinvestment.

Not only the big tech companies or massive construction companies will benefit from the renewed infrastructure, but also certain suppliers to those tech and infrastructure companies, like Atkore (ATKR).

However, credit rating agencies do not realize its importance and rate the company with a very high chance of default.

Let’s evaluate the company’s credit risk using Uniform Accounting and see what rating agencies are missing.

We can use Uniform Accounting to put the company’s real profitability up against its obligations and decide for ourselves the true risk of this business.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

We mentioned many times how important it is to renew our infrastructure based on modern technological developments.

The United States has overlooked these infrastructure investments for a long period, and new technologies have been developed like IoT and 5G. In addition, the pandemic proved to us how insufficient our supply chains are.

That is why nationwide massive investments are needed to get in line with new technological developments and to strengthen our supply chains. At Valens, we call this trend the “supply-chain supercycle”.

However, when we mention these investments, most people think about how big tech names, large communication network providers, or massive construction companies will benefit from them.

They are not the only one who gets the benefit, in fact, they’ll be the ones that spend the most.

Among the big winners of these investments will be the suppliers of essential products or services needed to build this new infrastructure.

One of these essential suppliers is Atkore. The company makes value-add wires, along with the components that help companies organize and connect those wires.

If you are thinking about building warehouses or factories as part of the supply chain supercycle, you need the wire trays and conduits that Atkore makes.

That means it has had and is going to continue to have strong demand for its products. It will also be crucial for providing one of the most needed materials to develop IoT and 5G technologies.

Yet, credit rating agencies are rating the name like it has a high credit risk with a 10% chance of going bankrupt in the next 5 years.

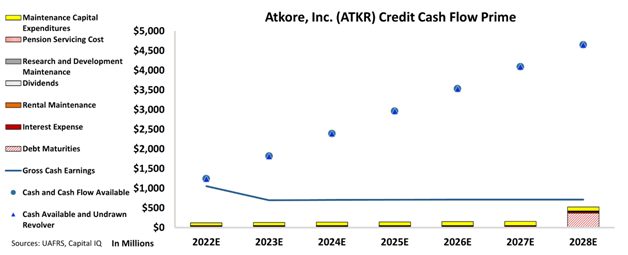

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (“CCFP”) to understand the company’s obligations matched against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart shows that Atkore’s cash flows are much more than enough to cover all its obligations going forward.

The company is a big cash machine and it does not have any debt headwalls coming in the near future. It continues to grow on the increased demand for its essential products.

Taking these factors into account, it makes no sense to think of a company like this to have a significant credit risk with a BB rating from S&P.

Here at Valens, we understand the essential positioning of the company and its potential. Thus we give it an IG3+ rating which is much lower than what credit rating agencies suggest.

An IG3+ rating implies approximately a 1% chance of default which is much more reasonable for Atkore.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Atkore, Inc. Tearsheet

As the Uniform Accounting tearsheet for Atkore, Inc. (ATKR:USA) highlights, the Uniform P/E trades at 9.0x, which is below the global corporate average of 18.4x, but above its historical P/E of 5.8x.

Low P/Es require low EPS growth to sustain them. In the case of Atkore, the company has recently shown a 64% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Atkore’s Wall Street analyst-driven forecast is for a -35% and 1% EPS growth in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Atkore’s $117 stock price. These are often referred to as market embedded expectations.

Furthermore, the company’s earning power in 2022 was 11x the long-run corporate average. Moreover, cash flows and cash on hand are more than 7x its total obligations—including debt maturities and capex maintenance. The company also has an intrinsic credit risk that is 200bps above the risk-free rate.

Overall, this signals a moderate credit risk.

Lastly, Atkore’s Uniform earnings growth is below its peer averages and is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research