AutoZone has reached new highs in 2022…just as we predicted last year

The last couple of years have seen a surge in demand for short-distance travel. Due to restricted air-travel and pandemic related restrictions, travel by car became the dominant mode of transportation.

As a result, demand for associated parts and service for automotives spiked, putting AutoZone (AZO) right in the midst of those tailwinds.

Like we predicted last year, AutoZone was primed for upside and has done well on realizing its potential.

Today, we are going to look closer at AutoZone using a Uniform Accounting lens to get a better idea of its true profitability and how well it has done since we examined it last year.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

As cities locked down due to the pandemic and typical social interactions were restricted, people ventured beyond their concrete jungles to more remote locations.

With most air travel restricted, many folks had to change their travel plans. Instead of faraway vacations, many people started exploring more local options and made use of cars, which is part of the reason demand for cars rose so suddenly.

However, new car production was constricted as factories needed to enact social distancing measures while semiconductor shortages capped total production as well. As a result, used cars experienced a major surge in demand, and in certain markets, prices of used vehicles exceeded those of new cars.

Last year, we talked about how one specific industry, the spare parts companies, would benefit from the surge in demand in used cars. Specifically, we highlighted AutoZone (AZO) as the name to ride these tailwinds.

Looking back a year later, AutoZone is up almost 50% since our original article publication date, thanks to impressive demand tailwinds in their business.

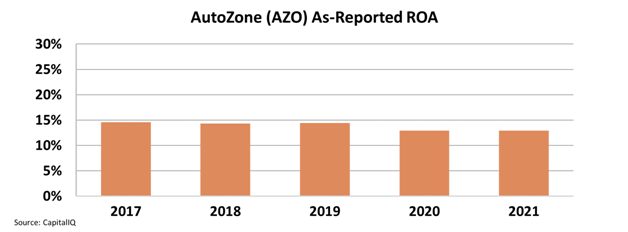

However, when we look at as-reported metrics, it looks like its profitability was actually down last year, not up.

With lower profitability amongst strong tailwinds in the industry, investors are led to believe that the company didn’t participate at all, and the stock rally has been driven on irrational theme investing instead of strong fundamentals.

The company has seen declining GAAP profitability since 2017, with as-reported ROA falling to market-level returns of 13% in 2021.

As reported metrics make it look like this is a company that hasn’t capitalized on the strong tailwinds the industry has seen over the past few years.

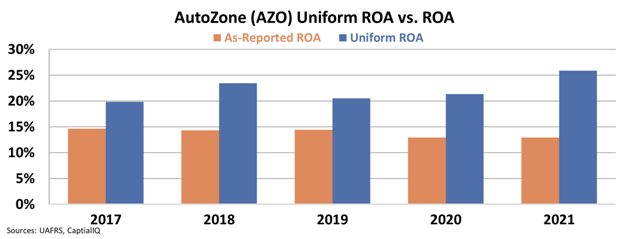

Once we take a closer look at AutoZone’s profitability using Uniform Accounting, we can see the reality of the company’s profitability.

The stock has actually surged thanks to these tailwinds creating material value in the business. Uniform returns reached an all time high in 2021, jumping from 21% in 2020 to 26% in 2021.

AutoZone has emerged as a key supplier of auto parts, just as we’d expect in the midst of a new automotive surge.

Thanks to the power of Uniform Accounting, we can see the real, material impact the used car part demand had on AutoZone. It is with this insight into the actual drivers of corporate profitability that Valens is able to find compelling investment opportunities before the rest of the market catches on.

SUMMARY and AutoZone, Inc. Tearsheet

As the Uniform Accounting tearsheet for AutoZone, Inc. (AZO:USA) highlights, the Uniform P/E trades at 23.0x, which is around the global corporate average of 24.0x, but above its own historical P/E of 19.6x.

Moderate P/Es require moderate EPS growth to sustain them. In the case of AutoZone, the company has recently shown a 30% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, AutoZone’s Wall Street analyst-driven forecast is a 14% and 2% EPS growth in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify AutoZone’s $2,165 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 2% annually over the next three years. What Wall Street analysts expect for AutoZone’s earnings growth is above what the current stock market valuation requires through 2023.

Furthermore, the company’s earning power in 2020 is 4x the long-run corporate average. Moreover, cash flows and cash on hand are almost twice its total obligations—including debt maturities and capex maintenance. Additionally, intrinsic credit risk is 60bps above the risk-free rate. All in all, this signals low credit risk.

Lastly, AutoZone’s Uniform earnings growth is below its peer averages, and the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research