Breaking down one of the most volatile furniture stocks

Nobody’s sure what to think about the housing market.

On one hand, sky high interest rates have substantially slowed down home buying activity. On the other, because nobody is selling their homes, new home sales have actually been decently strong.

And no matter how bad things get, some folks will need to buy homes. And with a new home comes the need for furnishings.

Today, we’ll cover one home furnishing stock that has taken a beating this year, and we’ll explain why if it’s able to survive a barrage of short sellers and credit pressures, it could have solid demand if we enter a recession.

Also below, is the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

There have been many talks about the U.S. economy in the last few years. We discussed stimulus packages, inflation, interest rates, and many more topics.

One of the more recent discussions was how high mortgage rates were going to kill the housing market and the residential construction industry. Well, that hasn’t really happened…

As we talked about before, home construction is still seeing high demand against the initial odds.

Homeowners are not selling their homes to protect their cheap mortgage. Some people still have to buy homes for various reasons. They might be getting married, having kids, they may have recently graduated, or they may have relocated because of work.

For these reasons, it’s impossible for all home sales to completely disappear.

And when you move into a new house, you need to furnish that house.

However, prices of everything have been surging. In an inflationary environment, new homeowners are trying to explore more economical alternatives when it comes to furnishing their homes.

In this case, buying a home might be a “stickier” cost than furnishing the home. Folks seem to be trading down their furnishing choices to more cost-effective solutions.

Big Lots (BIG) emerges as a frontrunner in this domain. Being one of the leading home discount retailers, the company stands as the go-to destination for those seeking affordable furniture options.

The attractiveness of Big Lots lies in its ability to offer budget-friendly furnishing choices without compromising on quality or aesthetics. As consumers navigate the complex terrain of fluctuating prices, the company provides affordability and practicality.

The resiliency of new home sales combined with high sustained inflation means that the demand for Big Lots’ product catalog remains strong.

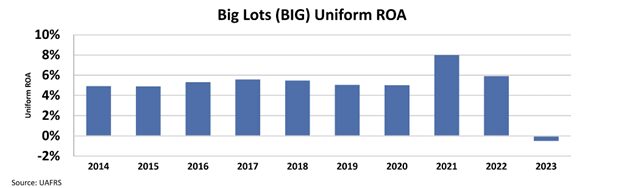

We can see how this demand affected the company’s operations after the pandemic.

Big Lots has averaged a Uniform return on assets (“ROA”) of around 5% between 2014 and 2020. As inflation started surging in 2021, the demand for their products skyrocketed, and ROA reached 8%.

Fiscal 2023 was tougher… SG&A costs skyrocketed, and the company recognized a $70 million impairment charge related to underperforming stores.

Since then though, management has been in cleaning mode.

The company has done a good job getting rid of its worst performing stores, which did hurt sales. Revenue fell about 15% last quarter.

That said, it was a necessary move. It was able to substantially trim SG&A costs, which were nearly 55% of sales, down to just 40% of sales.

At the same time, management got a lot of cash thanks to a sale leaseback agreement on one of its biggest distribution centers.

So today, the company looks like it’s in a lot better position from a capital structure and efficiency perspective. It has cash, it cut costs, and it has trimmed the business to focus on its most efficient stores.

And as we mentioned, with folks still needing to buy homes, and the potential for a recession to force households to trade down, Big Lots could have more customers in the next year than the market expects.

The company is heavily shorted today… which is part of why the stock has been so volatile. It still doesn’t look like it’s in the clear quite yet. It has made smart moves to improve liquidity. That said, the next few quarters could still be rocky.

If it’s able to keep afloat through the remainder of the year, it could be a beneficiary of the trade down effect. That said, we’d keep an eye from the sidelines today.

SUMMARY and Big Lots Tearsheet

As the Uniform Accounting tearsheet for Big Lots, Inc.(BIG:USA) highlights, the Uniform P/E trades at -9.3x, which is below its corporate average of 18.4x and its historical P/E of 183.6x.

Negative P/Es only require low EPS growth to sustain them. In the case of Big Lots, the company has recently shown a 119% shrinkage in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Big Lots’ Wall Street analyst-driven forecast is a 1,020% EPS growth in 2024 and a 62% EPS shrinkage in 2025.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Big Lots’ $6 stock price. These are often referred to as market embedded expectations.

Furthermore, the company’s earning power is below its long-run corporate average. Moreover, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends.

All in all, this signals high credit risk.

Lastly, Big Lots’ Uniform earnings growth is above its peer averages but below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research