How 5G implementation will help Ciena prove the rating agencies wrong

As the world continues to move on to the next generation of telecommunication technology, huge investment is needed to build 5G infrastructure.

Companies that provide equipment and services to the telecommunication industry are more than ready to support this infrastructure investment and prepared to benefit from it, such as Ciena Corporation (CIEN).

However, at a time when 5G is on the rise, rating agencies seem to miss the great potential Ciena has for the upcoming years and still see it as a risk. Let’s use Uniform Accounting to put the company’s real profitability up against its obligations and decide for ourselves the true risk of this business.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

The 5G revolution is here, and growth and value investors are looking to get in.

The easiest names to assume will be the big winners in the space are AT&T (T) and Verizon (VZ), as they are the customer-facing network providers who will be servicing 5G capable devices.

However, these companies are racing to the bottom, by competing on razor-thin margins to win consumer share, making them poor investments.

Furthermore, to provide the whopping 65% CAGR of 5G growth over the next decade, these companies have to invest huge sums into 5G infrastructure, which cuts into returns.

The real winners of 5G are the companies who provide or build the infrastructure, and will see demand go up as the cell networks spend big.

One of the providers of this infrastructure to route 5G data around the world is Ciena Corporation (CIEN).

Ciena is one of the most successful and reliable suppliers of networking equipment and software services in the telecommunications industry, and has consistently boosted its profitability over the last 8 years.

Yet, rating agencies put Ciena below investment grade with a BB+ rating, which implies a significant risk of default.

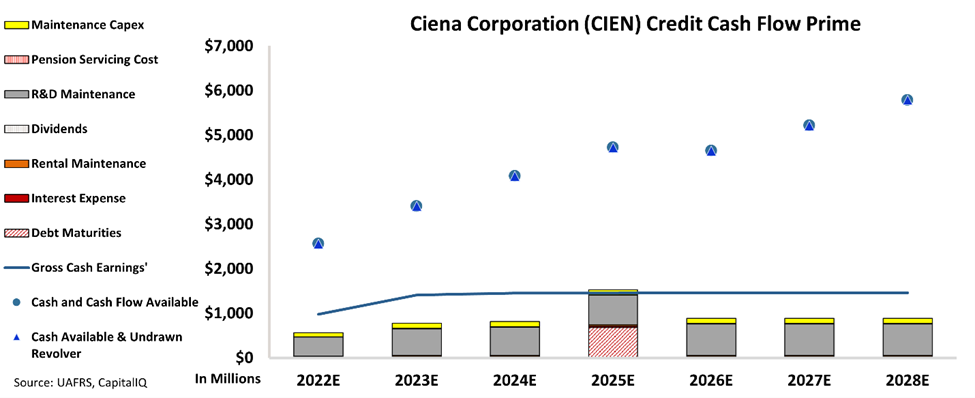

We can figure out if there is a real risk for this high-potential company by examining it through the lens of the Credit Cash Flow Prime (“CCFP”).

In the chart below, the stacked bars represent the firm’s obligations each year for the next seven years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The cash flows of Ciena are almost double all the company’s obligations through 2028. The company also has no debt maturities on its balance sheet for the next 3 years, and has plenty of cash on hand to service its debts in 2025.

Given the strength of its cash flows and balance sheet, we grade Ciena a much safer IG3+ investment-grade credit, which implies just a 1% chance of bankruptcy.

Ciena is yet another company where the credit rating agencies don’t capture the complete story. While we at Valens recognize the flaws with traditional credit ratings, many creditors do not. The BB+ credit ranking is pessimistic and paints a picture of a company that is much riskier than it is in reality.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Ciena Corporation Tearsheet

As the Uniform Accounting tearsheet for Ciena Corporation (CIEN:USA) highlights, the Uniform P/E trades at 15.1x, which is below the global corporate average of 24.0x, but above its historical P/E of 12.7x.

Low P/Es require low EPS growth to sustain them. That said, in the case of Ciena, the company has recently shown a 14% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Ciena’s Wall Street analyst-driven forecast is for a 7% EPS shrinkage and a 26% growth in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Ciena’s $55 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to decline by 9% over the next three years. What Wall Street analysts expect for Ciena’s earnings growth is above what the current stock market valuation requires in 2022 and 2023.

Furthermore, the company’s earning power in 2021 is 2x the long-run corporate average. In addition, cash flows and cash on hand are 4x its total obligations—including debt maturities and capex maintenance. Moreover, intrinsic credit risk is 60bps above the risk free rate.

All in all, this signals a low credit and dividend risk.

Lastly, Ciena’s Uniform earnings growth is above its peer averages, but the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research