Leverage is great until inflation starts rising, and this household giant is feeling the pain

Companies enjoyed the low cost of debt and access to “cheap money” for a decade, but now, the environment changes.

With the rising interest rates, those companies that used leverage to boost their returns may have a harder time.

The Clorox Company (CLX) is one of them. Returns have consistently increased in the last decade, and the image of this stable business makes credit agencies rate it BBB+.

However, a look at their capital structure shows that the company has a much worse credit risk than what the credit agencies suggest because of the inflationary environment.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Over the last decade, the low cost of debt made companies relaxed about their credit structure. They could access “cheap money” to fund their projects and refinance when needed.

This was not only about being able to find money. But it was about generating higher cash flows as well.

Many high-return and stable companies bought into the idea of taking on leverage to boost cash flow to shareholders, while also upping dividends at the same time.

While the big size and high return on assets (“ROA”) of these companies gave them confidence that this could be managed, the financial environment we have right now threatens their stability.

Now, there is the risk of inflation starting to disrupt their profit margins and spiking interest rates making those cash flow buffers less reliable.

A great example of this is Clorox (CLX).

It manufactures consumer and professional products that are used in cleaning, laundry, and grilling. The company also offers home care products such as water filtration systems and digestive health products.

It seems like this company should have a stable business with its diverse set of offerings. Actually, its Uniform Earnings has consistently increased from 2011 to 2021.

However, a look at Clorox’s balance sheet shows that this income is supported mostly by debt, which raises questions about its credit health.

Credit agencies think that Clorox deserves a BBB+ rating, saying there is a less-than 2% risk of default in the next five years.

But with a lot of leverage on the balance sheet, and rising interest rates making that more expensive, we want to have a look at this company’s credit structure for ourselves.

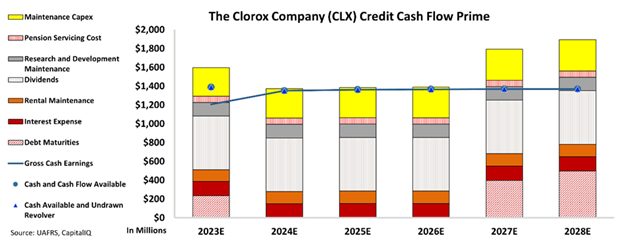

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (CCFP) to understand the company’s obligations matched against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart shows that The Clorox Company’s cash flows are only just enough to match all obligations each year going forward until 2027 at the current level of interest rates.

Assuming that the interest rates will be stable may not be realistic. If they go up, there is a risk that demand will be affected, and profits will dip.

This scenario would require the company to make tough decisions for its dividend and focus on being able to pay down its debt.

We have to keep in mind the profitability of that scenario, and the default risk if it does happen.

That’s why Clorox gets an HY2 rating from Valens, which corresponds to a much riskier credit rating considering the company’s fragility to rising interest rates and high financial and operating obligations.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and The Clorox Company Tearsheet

As the Uniform Accounting tearsheet for The Clorox Company (CLX) highlights, the Uniform P/E trades at 35.9x, which is above the global corporate average of 17.8x but slightly below its historical P/E of 36.4x.

High P/Es require high EPS growth to sustain them. In the case of Clorox, the company has recently shown a -43% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Clorox’s Wall Street analyst-driven forecast is for a -6% and 29% EPS growth in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Clorox’s $136 stock price. These are often referred to as market embedded expectations.

Furthermore, the company’s earning power in 2022 is 2x the long-run corporate average. However, cash flows and cash on hand are below its total obligations—including debt maturities and capex maintenance. The company also has an intrinsic credit risk that is 230bps above the risk-free rate.

Overall, this signals a moderate credit and dividend risk.

Lastly, Clorox’s Uniform earnings growth is in line with its peer averages and is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research