Semiconductors are nowhere to be found, but that’s not stopping this critical supplier

Inflation fears have been front and center for the past several months. The price of everything from used cars to lumber has been ballooning higher, as a result of supply shortages across the world.

In no industry has supply shortages been more acute than the semiconductor sector. Yet, credit rating agencies are completely missing how this supply shortage is a big benefit for some players in the space.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Inflation has been a constant concern for investors over the past several months, something we here at Valens have covered several times recently.

It seems like every month, investors get new consumer price index data showing a dramatic rise in prices across the board. The CPI increased 5.4% in June, the largest gain since 2008, with core CPI increasing 4.5%, the largest move since 1991.

These record numbers have stoked investor fears that rising prices will cause interest rates to follow, or that governments trying to large debt loads on their balance sheets will let currencies devalue.

However, investor fears are mostly misplaced. Recent inflation has not been caused by too much money chasing too few goods, like during the 60s and 70s. Instead, it has resulted from dramatic short-term supply and demand mismatches due to the pandemic.

The best example of this earlier this year was how lumber rocketed higher in price, due to a spike in demand and a lack of supply to meet it. But then, as lumber production ramped back up, prices fell back down, showing the spike in inflation was truly transitory.

Another market with dramatic supply and demand mismatches we have covered before is the semiconductor industry when talking about Amkor Technology (AMKR).

Unlike in lumber, where meeting supply just required current sawmills and loggers to ramp up capacity, for semiconductors, entire new factories need to be constructed just to keep up with the booming demand.

There is another difference to lumber as well. While building these plants takes time, the demand for semiconductors isn’t going away anytime soon.

That means a lot of chip equipment makers are going to have a long order book of demand for the foreseeable future, which should help dampen what historically is a cyclical industry, and at minimum give several years of high cash flow visibility.

However, the rating agencies don’t appear to comprehend this transformation. We already highlighted how they’re missing the picture with Amkor, but now we have found another mismatch.

Cohu (COHU), like Amkor, makes semi-chip test and inspection equipment for chip and circuit board makers, which will be a booming industry for the foreseeable future.

Despite this clear demand for Cohu’s products, S&P rates the company as a B+ high yield credit, with a 25% risk of default in the next 5 years.

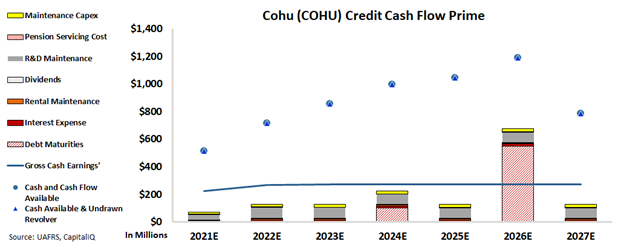

Looking at our credit cashflow prime (CCFP) framework, we can get to the heart of the firm’s true credit risk and see how the rating agencies are completely off base.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

Looking at the CCFP, we can see how just Cohu’s cash flows well exceed all operating obligations in each year. The company also has ample cash on its balance sheet, with no debt coming due until 2026.

Cohu can easily cover all obligations for the foreseeable future, but S&P rates it as a B+ high yield credit, which makes no sense.

Using the CCFP analysis, Valens rates Cohu as crossover XO credit. This rating corresponds with an expected default rate of around 2% within the next five years, a more realistic projection once a holistic understanding of the company’s risk is taken into account.

With such a blanket bearish outlook of a booming industry, investors relying on the ratings agencies are missing out on a plethora of potential investment opportunities.

SUMMARY and Cohu, Inc. Tearsheet

As the Uniform Accounting tearsheet for Cohu, Inc. (COHU:USA) highlights, the Uniform P/E trades at 9.8x, which is below the global corporate average of 23.7x and its own historical average of 12.1x.

Low P/Es require low EPS growth to sustain them. In the case of Cohu, the company has recently shown 52% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Cohu’s Wall Street analyst-driven forecast is a 163% EPS growth in 2021 and 27% EPS decline in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Cohu’s $35.4 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink 1% over the next three years. What Wall Street analysts expect for Cohu’s earnings growth is above what the current stock market valuation requires in 2021 but below the requirement in 2022.

Furthermore, the company’s earning power is 2x the long-run corporate average. Moreover, cash flows and cash on hand are 2x its total obligations—including debt maturities, capex maintenance, and dividends. However, intrinsic credit risk of 650bps is above the risk-free rate. Together, this signals a high credit risk.

To conclude, Cohu’s Uniform earnings growth is above its peer averages and the company is trading below peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research