Inflation is Again Hitting Headlines, But Will it Torpedo Portfolios?

Over the past forty years, the Federal Reserve has been able to keep the U.S. inflation level at a low consistent rate. This has been a boon for the stock market, keeping valuations high.

Now, the large stimulus package and the reopening of the economy has meant short-term inflation is starting to spike, worrying investors that valuations could tumble.

The question now is if inflation rates will stay high and impact the markets, or come back to earth and have little impact on the market recovery.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

Walking through the aisles of a supermarket, or shopping for a computer online, it’s easy to think of prices as static. Despite this, thanks to monetary policy from the Federal Reserve and the nature of growing demand, prices climb slowly but steadily every year.

This phenomenon, often misunderstood or complicated by analysts, is inflation. Over the past few months, fears of inflation have been stoked by pundits. Speculation of future price climbs has meant it has taken over headlines once again.

The replacement value of a home, or how much it would be to rebuild with similar materials, has climbed by 20% year-over-year, highlighting the immense scarcity of lumber, screws, and fastenings.

Executives of the Coca-Cola Company (KO) are telling investors they will have to raise the price of a Coke in the near future. Chipotle (CMG) has bumped up the prices of its menu across the board, citing input costs climbing.

Even the steady, dependable, and sensitive to price change industry of consumer goods is forced into action. Procter & Gamble (PG) is raising the price of many consumer products in its sizable portfolio.

Tracking these kinds of home goods and more is the consumer inflation index, which rose by 5% in May. Meanwhile, the producer inflation index, the rate at which companies have seen the price of their inputs rise, was even more severe, up 6% in April.

With supply chains stretched taut, it makes sense inflation is at its worst the further back in the value chain investors look. This is why in the world’s factory of China the inflation rate is even more worrying.

Input inflation in China was a full-throated 9% in May, the largest jump in thirteen years. Back across the Pacific, the sudden gap-up in inflation has seen a lot of demand for political reform around the minimum wage and a lack of willing employees to work minimum wage jobs.

The last time the minimum wage was set in 2009, it was locked in at $7.25. However, thanks to inflation peaking over the past few years, $7.25 today is only worth $5.78 in 2009 dollars, or 20% less.

Other than this year, inflation has been low and steady. These huge swings in purchasing power are why inflation has a huge number of consequences in economics, politics, and the stock market.

If you are a steady reader of the Investor Essentials Daily, you will know on our Monday articles on the economy we have covered inflation before.

Back in April, we highlighted how inflation levels directly impact investor’s returns. At higher inflation rates, money is worth less in the future than it is today. As investors put their money away to get a return at a later date, all else being equal valuations have to be cheaper in a higher inflation environment to earn the same returns.

This means the price to earnings (P/E) ratio of the market will settle at a different level if the long-term inflation rate changes. The key word here is long-term. The Federal Reserve and many economists believe this period of inflation to be driven by supply chain issues and heightened demand as the economy is reopening. This means the rate should return to normal after 2021.

Meanwhile, the CEO of Honeywell believes inflation “is here and it is probably a lot more pronounced [than] people think.”

Even though inflation will mean nominal profits grow faster, if they grow faster at a lower P/E, it will hold back equity appreciation significantly.

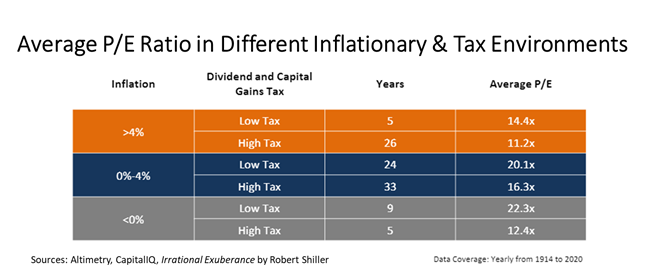

As this chart below shows, if high rates of inflation above 4% are here to stay, P/E ratios will plummet from around 20x all of the way down to 14.4x.

However, if this inflation proves to be transitory, then the markets will be unaffected and can stay near 20x levels. For inflation to batter valuations, it needs to consistently depress the value of the dollar over the next few years.

For now, investors should by no means panic and sell out of the market on fears of inflation destroying their portfolio. Currently, there is little evidence inflation is here to stay for the long-haul.

However, investors should be aware of the potential risks which could develop over the next year. If inflation looks to be more permanent, our readers will be the first to know.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research