This firm is another “roadie” riding industry tailwinds to breakout success

The entire communications equipment industry has benefited greatly from the macroeconomic tailwinds occurring. The rollout of 5G and connectivity of the Internet of Things (IoT) have renewed investor interest in the space.

However, investors continue to only focus on the high level players in this trend. This firm is another in a line of infrastructure providers making this transformation possible.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Today, we are going back to discuss a market theme we have already covered. Despite this, the market still isn’t paying attention.

As we recently discussed in our Broadcom (AVGO) and NetScout Systems (NTCT) articles, investors are looking to invest into the hot new technology trends that have the ability to change the world.

Many of these tailwinds include connectivity from the Internet of Things (IoT), which encompasses the recent 5G rollout as well as home network systems and wide area networks.

However, the news media and investing pundits often focus on the “stars” of the show. These companies may be overvalued, as investors are already pricing in perfection. That is why we have been focusing on the “roadies” of this digital transformation.

One company that is benefiting from many of the same macroeconomic tailwinds highlighted above is CommScope (COMM).

CommScope operates in these same industries. Specifically, the company works to implement infrastructure solutions for communication networks.

As we often highlight in our articles, the distortions between as-reported and Uniform Accounting can lead investors down an incorrect path when analyzing a company.

In CommScope’s case, it is perplexing why people are excited about the trend in 5G and IoT when looking through the lens of as-reported accounting.

Evidently, it would appear no member in the space is currently making any money from their products and services.

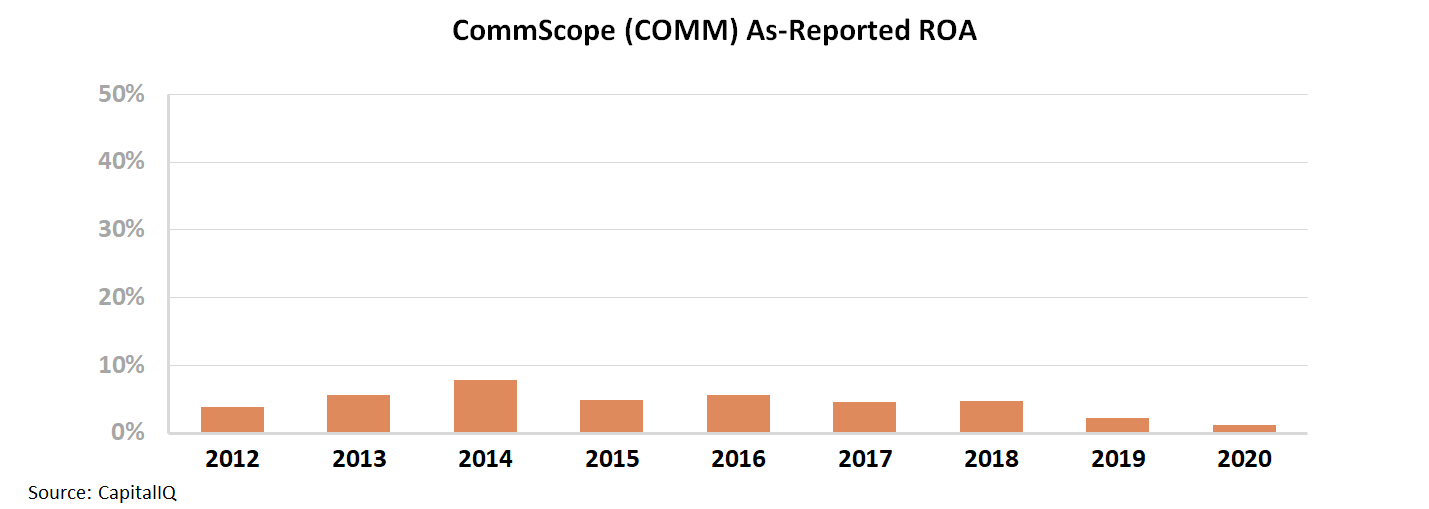

For example, the as-reported metrics of CommScope are weak. Over the past nine years, the firm’s as-reported ROA levels have failed to breach the U.S. corporate average.

Specifically, the ROA levels for this firm have ranged from 1% to 6% from 2012 to 2020, excluding outlier 8% ROA in 2014.

It appears CommScope is barely making any money.

In reality, this is not an accurate picture of CommScope’s performance. After making adjustments around goodwill, amortization, and other line items, it’s clear the firm has higher than average returns.

When looking through a Uniform Accounting lens, it becomes clear that the firm’s business is better than it seems.

As portrayed in the below chart, the firm’s ROA levels have exceeded 8% levels since 2012, reaching a peak of 48% in 2019.

In reality, Uniform Accounting metrics highlight the strong returns CommScope has been generating over the past nine years.

The firm has benefited from macroeconomic tailwinds, specifically in relation to industry trends in the 5G space and the overall IoT market.

We suspect these trends will only gain further traction and lead to further technology advancements within the next few years, positioning CommScope for success.

SUMMARY and CommScope Holding Company, Inc. Tearsheet

As the Uniform Accounting tearsheet for CommScope Holding Company, Inc. (COMM:USA) highlights, the Uniform P/E trades at 10.2x, which is below the global corporate average of 25.2x, but around its own historical average of 8.7x.

Low P/Es require low EPS growth to sustain them. That said, in the case of CommScope, the company has recently shown a 29% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, CommScope’s Wall Street analyst-driven forecast is a 2% EPS shrinkage in 2021 followed by a 3% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify CommScope’s $16 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 12% per year over the next three years. What Wall Street analysts expect for CommScope’s earnings growth is above what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power is 6x the long-run corporate average. Also, intrinsic credit risk is 430bps above the risk-free rate and cash flows and cash on hand are slightly above its total obligations—including debt maturities and capex maintenance. Together, this signals a moderate credit risk.

To conclude, CommScope’s Uniform earnings growth is below its peer averages, but the company is trading around its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research