This company is ready to support nearshoring with its railways

The pandemic brought the world’s supply chain problems to light, but the truth is, they have been around long before the pandemic.

We have ignored investments in this area, and now we need more resilient systems to adapt to the new world.

This is why the Supply Chain Supercycle is coming, and we can see it happening through one key indicator: nearshoring.

As manufacturing comes home, transportation companies like Canadian Pacific Railway (TSX:CP) will be ready to provide transportation for this new demand.

With booming demand, the already profitable company has a very good opportunity to improve its business even further.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

The events of the last few years have changed the way the world works. Of course, the working world has changed immensely, making remote work much more common.

However, it also brought to light some of the weaknesses in our global structure. As e-commerce businesses enjoyed booming demand, supply chain issues have turned customer experience into a nightmare.

While customers waited for their orders, lots of manufacturers were waiting for their raw materials. Everyone took a share of the problems that lack of investment in the supply chain created.

We have talked about the Supply Chain Supercycle numerous times. We’ve needed investments in the supply chain for a long time, but the pandemic, and now Russia’s invasion, helped us realize it.

Now, we are looking to rebuild supply chains post-pandemic and in a more uncertain world. That is why we need supply chains to be more resilient.

One popular idea to achieve this is nearshoring. Companies are bringing their manufacturing facilities closer to home to decrease lead times and prevent catastrophic failure.

For the U.S., that means Canada and Mexico are going to be the new hubs for the supply chain. Instead of relying on boats and planes to get goods to the U.S., trains are coming back into fashion.

One big beneficiary of this is Canadian Pacific Railway Limited (TSX:CP). The company operates a transcontinental freight railway in Canada and in the U.S., transporting bulk commodities and retail goods.

The company already had the ability to mirror what the big U.S. railroads do with its railroads across Canada. It has been transporting goods from big ports like Vancouver to the rest of the continent.

With nearshoring speeding up, Canadian Pacific will enjoy surging demand and have more goods to transport.

Additionally, the acquisition of transportation holding company Kansas City Southern gives it a huge exposure to the Mexican railroad, which is an even bigger hub in nearshoring.

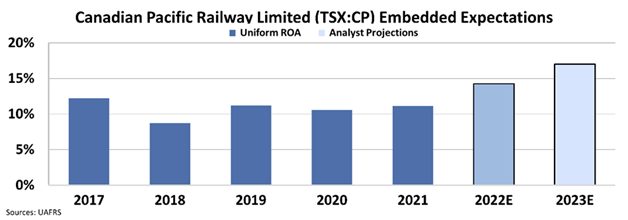

Canadian Pacific’s Uniform return on assets (“ROA”) shows that it had stable returns over the last five years around 10%.

Now, Canadian Pacific Railway has an amazing opportunity to improve profitability, and analysts understand this.

Wall Street analysts forecast Uniform ROA to jump from 11% in 2021 to a would-be record 17% in 2023.

Analysts clearly see what’s coming for the U.S. supply chain. Namely, more of it is moving back to North America.

As the Supply Chain Supercycle plays out, Canadian Pacific’s established position, exposure to big hubs like Canada and Mexico, and access to important ports will help it push a lot more volume through its infrastructure.

That’s why analysts expect the company to have two record years coming up – the supercycle is underway.

SUMMARY and Canadian Pacific Railway Limited Tearsheet

As the Uniform Accounting tearsheet for Canadian Pacific Railway Limited (CP:CAN) highlights, the Uniform P/E trades at 16.7x, which is below the global corporate average of 18.9x and its own historical P/E of 21.7x.

Low P/Es require low EPS growth to sustain them. In the case of Canadian Pacific Railway, the company has recently shown a 8% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Canadian Pacific Railway’s Wall Street analyst-driven forecast is a 1% and 37% EPS growth in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Canadian Pacific Railway’s CAD 92 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 3% annually over the next three years. What Wall Street analysts expect for Canadian Pacific Railway’s earnings growth is below what the current stock market valuation requires in 2022, but above the requirement in 2023.

Furthermore, the company’s earning power in 2021 is 2x the long-run corporate average. Moreover, cash flows and cash on hand are above its total obligations—including debt maturities, capex maintenance, and dividends. Also, the company’s intrinsic credit risk is 90bps above the risk-free rate.

All in all, this signals low dividend risk.

Lastly, Canadian Pacific Railway’s Uniform earnings growth is below its peer averages, and below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research