Credit agencies miss the vitality of this semiconductor company’s products

Statistics show that technology grows at a faster pace than ever before and spending follows. Government and businesses work together to improve and grant funds, which benefits the creators of technology, especially semiconductor companies. Today, a wave of spending is sweeping the semiconductor industry.

One of the biggest companies in the space is Lattice Semiconductor Corporation (LSCC). Though its products and services are vital, the credit agencies seem to think otherwise by rating the company BB.

We can use Uniform Accounting to compare the company’s obligations with its cash flows and decide for ourselves the true risk of the business.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Technology develops at a faster pace than ever before.

The global distribution of startups shows that most of them operate in the technology sector. The number of startups continues to climb thanks to the ‘innovation dynamo’ that is going on in the United States.

In 2021, a record 5.4 million applications were filed to form new businesses, a 53% increase from 2019.

Additionally, business and government spending on technology continues to surge. It rose from $1.2 trillion in 2012 to $1.8 trillion in 2020.

US-based technology companies are happy with this trend, but there is one set of companies that will benefit from it even more: semiconductor companies…

They constitute an essential part of the modern economy, supplying most of the major innovators.

One big and seemingly misunderstood company in the semiconductor space is Lattice Semiconductor Corporation (LSCC).

The company specializes in the design and manufacturing of low-power, field programmable gate arrays (“FPGA”), needed components in communications, computing, industrial, automotive, and consumer markets.

The products that Lattice Semiconductor supplies are critical for these industries, but it seems that the credit agencies fail to understand this reality.

They think there is a 10% chance that the company will go bankrupt, rating it a BB. Looking at the fundamentals of the market, this rating seems absurd.

Although the facts are clear, it is always wise to check the financial stance of Lattice Semiconductor to be sure of its risk of default.

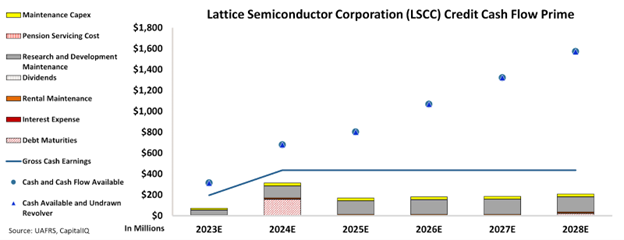

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (CCFP) to understand the company’s obligations matched against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next six years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The chart proves that Lattice Semiconductor has a much safer credit profile than credit agencies suggest.

The CCFP shows that the company’s cash flows consistently exceed operating and financial obligations for the next six years.

Not only will this company have no problems with its current obligations, but it will also have room to invest more heavily in the business.

As a result, Lattice Semiconductor gets an IG3+ rating from Valens. This corresponds to a default risk that is less than 2%, which makes much more sense when we can see the company’s cash flows and liabilities.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Lattice Semiconductor Corporation Tearsheet

As the Uniform Accounting tearsheet for Lattice Semiconductor Corporation (LSCC:USA) highlights, the Uniform P/E trades at 38.0x, which is above the global corporate average of 19.3x, but below its historical P/E of 53.6x.

High P/Es require high EPS growth to sustain them. In the case of Lattice Semiconductor, the company has recently shown a 109% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Lattice Semiconductor’s Wall Street analyst-driven forecast is for a 79% and 19% EPS growth in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Lattice Semiconductor’s $57 stock price. These are often referred to as market embedded expectations.

Furthermore, the company’s earning power in 2021 is 3x the long-run corporate average. However, cash flows and cash on hand are more than 3x its total obligations—including debt maturities and capex maintenance. The company also has an intrinsic credit risk that is 90bps above the risk-free rate.

Overall, this signals a low credit risk.

Lastly, Lattice Semiconductor’s Uniform earnings growth is above its peer averages, and is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research