Investing in digital safety

CrowdStrike (CRWD) is a leading provider of cloud-native endpoint protection, serving over 50% of the Fortune 500 and numerous government agencies globally.

Its Falcon platform, powered by AI/ML analytics, detects sophisticated threats in real time, handling over 3 trillion events weekly.

The company has high cash reserves, and no debt maturing in the next five years.

This, along with the growth in cybersecurity spending and the demand for managed security services, positions CrowdStrike for continued market share gains and profitable growth.

Despite these factors, rating agencies have concerns over CrowdStrike’s financial health caused by the company not posting a positive income since its 2019 IPO.

Today, we’re exploring CrowdStrike’s credit risk through the lens of Uniform Accounting to determine the accuracy of rating agencies’ assessments of the company.

We can use Uniform Accounting to put the company’s real profitability up against its obligations and decide for ourselves the true risk of this business.

Also below is a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Friday Credit Insights

Powered by Valens Research

CrowdStrike (CRWD) has established itself as the leading provider of cloud-native endpoint protection through its Falcon platform.

Founded in 2011, the company pioneered the concept of endpoint detection and response (“EDR”) delivered as a cloud service.

Falcon collects over 3 trillion endpoint-related events per week from customers spanning all major industries and the public sector.

Its AI/ML-powered analytics detect even the most sophisticated threats in real time. This differentiated technology has fueled CrowdStrike’s rapid growth.

The company now serves over 50% of the Fortune 500 and many government agencies worldwide. In fiscal 2023, CrowdStrike’s customer count surpassed 2023.

Average contract values and net dollar retention rates consistently top 130%, evidence of expansion within the installed base. CrowdStrike’s solutions have become mission-critical for security operations, creating high switching costs.

Rather than take on debt, CrowdStrike has primarily relied on equity markets to fund operations and acquisitions like Humio in 2021.

This conservative strategy provides flexibility. For example, at the IPO, CrowdStrike raised $600 million through a stock offering to capitalize on accelerated digital transformation trends. It avoided the riskier approach of borrowing when credit was tightening.

CrowdStrike’s large cash reserves can fund several years of operating expenses and CAPEX even without new sales. This mitigates downside risks compared to less liquid or more leveraged firms.

The balance sheet also gives CrowdStrike capacity for strategic investments. In 2023, it acquired Bionic Stork to enhance its endpoint workload protection capabilities. Such deals expand the platform without stretching the financial profile.

However, the rating agencies are concerned about the company not posting a positive income since its IPO in 2019.

S&P gave the company a “BB+” rating, indicating a significant risk of default at nearly 10% over the next five years. It also puts the company in the high-yield basket.

Given its solid financial standing, we believe CrowdStrike deserves a more secure rating.

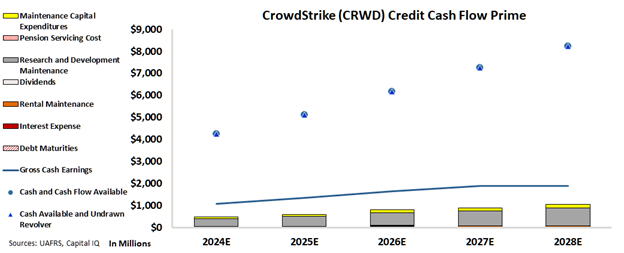

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (“CCFP”) to understand how the company’s obligations match against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart shows that CrowdStrike’s cash flows alone are more than enough to serve all its obligations going forward.

The chart indicates that the company is on solid financial ground and is likely to easily fulfill its obligations in the next five years.

The company has no debt maturing in the next five years and its substantial cash flows and cash on hand should easily cover all of its obligations.

Remote work proliferation and digital initiatives are driving 10-15% annual growth in global cybersecurity spending through 2027. Emerging threats like ransomware are also fueling demand for managed security services.

As the market leader in the high-growth EDR space and with its AI/ML advantages, CrowdStrike is well-positioned to continue taking share. This favorable backdrop enhances its ability to deliver consistent profitable growth.

Our review of CrowdStrike shows that the company has a low risk of default, contrary to what rating agencies indicate.

Therefore, we are assigning an “IG3+” rating to the company, which places it in the investment-grade basket, with a risk of default of about 1%.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and CrowdStrike Holdings, Inc. (CRWD:USA) Tearsheet

As the Uniform Accounting tearsheet for CrowdStrike Holdings, Inc. (CRWD:USA) highlights, the Uniform P/E trades at 115.4x, which is above the global corporate average of 22.9x but below its historical P/E of 139.8x.

High P/Es require high EPS growth to sustain them. In the case of CrowdStrike Holdings, Inc., the company has recently shown a 99% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations, that in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, CrowdStrike Holdings, Inc.’s Wall Street analyst-driven forecast is a 68% and 23% EPS growth in 2024 and 2025, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify CrowdStrike Holdings, Inc.’s $324 stock price. These are often referred to as market-embedded expectations.

Furthermore, the company’s earning power in 2023 was 3x the long-run corporate average. Moreover, cash flows and cash on hand are 5x its total obligations—including debt maturities and capex maintenance. The company also has an intrinsic credit risk that is 30bps above the risk-free rate.

Overall, this signals a low credit risk.

Lastly, CrowdStrike Holdings, Inc.’s Uniform earnings growth is above its peer averages and is trading within its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research