This Tiger Cub’s legacy was shaped by a legendary psychoanalyst

Those who have seen the Showtime drama Billions but don’t have a deep working knowledge of the financial world may be surprised to learn the show actually does a good job of approximating the 1980s hedge fund universe.

Today, we are going to examine a fund with ties to the hedge fund world Billions is referencing. By examining the fund’s portfolio, we can see if it is using better accounting data with UAFRS, or stuck with as-reported metrics.

In addition to examining the portfolio, we’re including a deeper look into the fund’s largest current holding, providing you with the current Uniform Accounting Performance and Valuation Tearsheet for that company.

Investor Essentials Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

In the show Billions, one of the main characters, Wendy Rhoades, is clearly pulled directly out of another hedge fund story. In the show, she plays the role of a psychiatrist-by-trade who uses her deep understanding of human nature to help build Bobby Axelrod’s fund from the ground up.

This should remind people in the hedge fund universe of the late Dr. Aaron Stern, a psychoanalyst who helped Julian Robertson build his own hedge fund, Tiger Management, from scratch.

Stern was responsible for a talent acquisition strategy that Robertson may owe his fund’s success to. As the fund grew, Stern functioned as Robertson’s right-hand-man, advising him at every step.

Tiger management performed exceptionally between 1980 and 2000, with average annual returns net of fees greater than 25%. But its role within the hedge fund world is much more pronounced.

Those who worked at Tiger went on to create their own funds, becoming known as the “Tiger Cubs.” And those that emerged from Tiger Cub funds became known as “Tiger Grandcubs.” There are now trillions of dollars under management that can be linked back to Tiger Management.

Funds tend to have a parabolic nature—they post strong returns for some number of years but then fade into irrelevance as their strategy becomes obsolete. The reason for this is that inventing a brilliant strategy is hard, but changing it to keep up with the times is a whole new ball game.

The Tiger Cubs, however, have bucked this trend by matching the performance of the overall hedge fund universe even to this day. This may be a byproduct of how Aaron Stern directed Julian Robertson to hire.

Those who are familiar with the hedge fund industry today may think of firms like Two Sigma, Citadel, or Jane Street, who have been hiring math PhDs and talented data scientists. But Tiger Management led the way in creating the stereotype that these well-known quant funds are breaking.

Stern understood that once a person reaches a certain IQ benchmark, incremental raw intelligence was no longer the value-add you might think it to be.

Instead, he found the “special sauce” in other aspects of an applicant’s personality. He loved hiring extraverted guys who played a lot of sports, as their competitive nature is what drives them to pull the extra mile at work.

He also hired generalists instead of specialists. He preferred people who understood multiple angles for every story, could get on well with their teammates, and were willing to ask tough questions even to those in authority.

As the cubs built their own funds, it became clear that Stern’s philosophy had legs to it.

You might recognize names like Lee Ainslie (Maverick Capital), William Bollinger (Edgerton Capital), Steve Mandel (Lone Pine Capital), and Andreas Halvorsen (Viking Global Investors).

All of them had been filtered through Aaron Stern’s hiring philosophy. Now, they sit atop the modern hedge fund world.

One other notable fund to emerge from Tiger Capital was Coatue Management, led by ex-Tiger managing director Phillipe Laffront.

Through this privately-held fund with $48 billion AUM, Laffront operates both in the private equity and public equity markets, focusing on high-growth technology companies. This could be indirectly compared to Cathie Wood’s ARK fund, but with a much more pronounced private equity component.

The fund has generated nearly $10 billion excess capital since its 1999 founding, having made notable investments in firms like Snapchat (SNAP), ByteDance, Doordash (DASH), and Spotify (SPOT).

By looking at its investments on a Uniform accounting framework rather than using as-reported figures, we can get a much better sense of their true economic productivity.

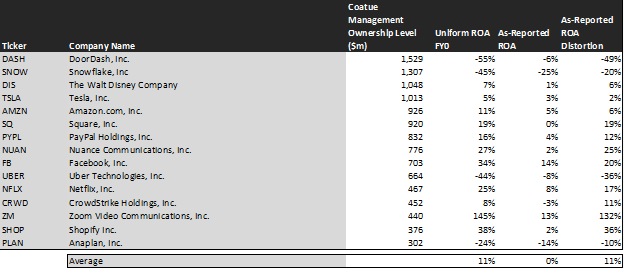

We’ve conducted a portfolio audit of Coatue Management’s top equity holdings, based on its most recent 13-F, focusing on their public, non-financial company holdings.

Uniform Accounting metrics highlight the company’s public equity investments are a mixed bag in terms of as-reported distortions, mostly because its two largest holdings (DASH and SNOW) are still in a rapid growth phase looking to dominate their markets before achieving profitability.

For the rest of its top holdings, however, Uniform Accounting metrics show that these companies are much higher quality and have higher potential than most would realize.

See for yourself below.

When equally weighing these names, we can see that the average as-reported ROA is immaterial. But even when considering the growth-phase companies (DASH, SNOW, and UBER) within this portfolio, Uniform Accounting paints a better picture, with an average ROA of 11%.

Let’s look at the fund’s largest holding, DoorDash (DASH), as an example. If you looked only at its as-reported metrics, you would see an ROA of -6%. Although this is already unfavorable, after removing the distortions inherent with GAAP accounting, we see that DoorDash has a Uniform ROA of -55%. DoorDash is not a firm that only just falls short of breaking even, it is a company that is hemorrhaging money.

Other firms in this portfolio experience the GAAP distortions in the other direction. PayPal (PYPL), for example, has an as-reported ROA of 4%, well below the cost of capital. In reality, its true Uniform ROA is 16%. PayPal is a robust firm that has consistently returned double or triple the cost of capital since going public, and has far better asset utilization than it reports.

Finding companies where as-reported metrics mis-represent their economic productivity is not the only key to extracting alpha. Those companies also need to be significantly undervalued by the market.

Coatue is also investing in companies that the market has lower expectations for, which increases the chance of significant upside turnarounds.

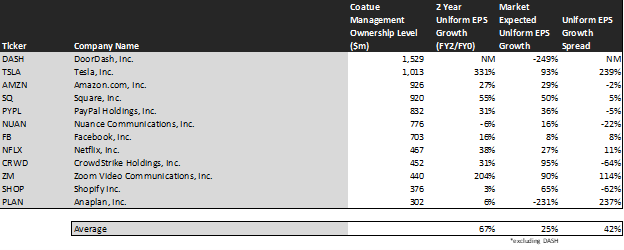

This chart shows three interesting data points:

– The first datapoint is what Uniform earnings growth is forecast to be over the next two years, when we take consensus Wall Street estimates and we convert them to the Uniform Accounting framework. This represents the Uniform earnings growth the company is likely to have, the next two years.

– The second datapoint is what the market thinks Uniform earnings growth is going to be for the next two years. Here, we are showing how much the company needs to grow Uniform earnings in the next 2 years to justify the current stock price of the company. If you’ve been reading our daily and our reports for a while, you’ll be familiar with the term embedded expectations. This is the market’s embedded expectations for Uniform earnings growth.

– The final datapoint is the spread between how much the company’s Uniform earnings could grow if the Uniform Accounting adjusted earnings estimates are right, and what the market expects Uniform earnings growth to be.

The average company in the U.S. is forecast to have 5% annual Uniform Accounting earnings growth over the next 2 years. Coatue’s holdings are forecasted by analysts to grow by 67%, well above average.

This is well above the growth the market is currently pricing in. The market expects earnings to grow by 25% for the next two years.

One example of a company in the Coatue portfolio that has mispriced growth potential is Tesla Motors (TSLA). Analysts covering TSLA who work every day to forecast sales and growth have 331% Uniform earnings growth built in, but the market is pricing earnings to grow only by 93%.

Anaplan (PLAN) also has massive dislocations built in. While analysts expect the firm to grow earnings by 6%, at current levels the market expects earnings to shrink by 231% over two years.

Across these securities, there is an average 42% dislocation that is favorable for Coatue. Another example of a firm with such a large dislocation is Morgan Stanley’s MACG.X, which you can read about here.

Like Coatue, MACG.X invests in high-growth technology firms, but features an average dislocation of 120%, while also holding firms whose financials are more severely distorted by GAAP accounting.

Many of the securities that Coatue holds have strong upside potential, but their largest holdings may be preventing them from taking investor capital as far as it can go. DoorDash (DASH) is the worst offender, with market expectations far higher than those of industry analysts, and economic productivity that is over-stated by their reported financials.

DoorDash, Inc. Tearsheet

As Coatue’s largest individual stock holding, we’re also highlighting the tearsheet of DoorDash today.

As our Uniform Accounting tearsheet for DoorDash, Inc. (DASH:USA) highlights, its Uniform P/E trades at 631.4x, which is well above the global corporate average valuation of 23.7x and its own historical valuation of 185.4x.

High P/Es require high EPS growth to sustain them. In the case of DoorDash, the company recently had a 287% Uniform EPS growth.

While Wall Street stock recommendations and valuations poorly track reality, Wall Street analysts have a strong grasp on near-term financial forecasts like revenue and earnings.

As such, we use Wall Street GAAP earnings estimates as a starting point for our Uniform earnings forecasts. When we do this, we can see that DoorDash is forecast to see a Uniform EPS shrinkage of 96% and 618% in 2020 and 2021, respectively.

The company’s earnings power is well below corporate averages. However, cash flows and cash on hand consistently exceed obligations, indicating a low credit risk.

To conclude, Lowe’s Uniform earnings growth is well below peer averages, but is trading well above peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research