Dying industries like this might offer great recession protection

Companies in dying industries are usually ignored by investors. That is exactly why there are good opportunities lying there.

One of these seemingly dying companies is Ennis (EBF). It is an incredibly old printing business dating back to 1909.

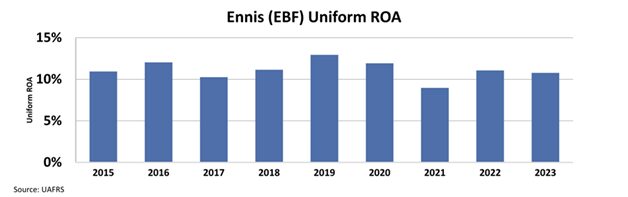

It is a difficult industry to innovate and is not exactly a high-growth one. However, despite the high pace of digitalization, Ennis has managed to be an incredibly stable business generating around 10% each year for the last eight years.

The market focuses on the industry and fails to see the sustainability of Ennis’ returns. This results in undervaluation and creates an opportunity for investors.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Not all businesses in dying industries are bad.

They are mostly ignored because of the nature of their industry, but that is what turns them into opportunities.

Just last week, we covered how News Corporation (NWSA) might be a slowly dying business. Yet, it does not mean it is doomed to be able to pay its debts like credit agencies think. It has plenty of cash flow to cover its obligations.

It is possible to find such misunderstood businesses. Ennis (EBF) is another great example.

The company dates back to 1909…

It is true that it is an incredibly sleepy business—the company runs printing shops…

That is hardly a high-growth industry. Things have been moving online for a long time and the pandemic was the biggest hit.

We had to do everything from our homes. Work, entertainment, and eating all transitioned to digital all of a sudden.

This was pretty bad for a paper-heavy business such as Ennis. With companies working either hybrid or fully remote and shopping being done mostly on e-commerce, it struggles to grow and get more clients.

That said, the clients it does have are pretty stable. It can print all kinds of things, from promotional materials to custom signs and banners.

The company’s historical profitability is proof of its stability. Despite the exceptionally fast digitalization efforts all over the world in the last couple of years, Ennis’ ROA has been consistently around 10%.

This is the stability one would want in a recession scenario. Heading into a possible recession, we would expect investors to move more into names like this.

And yet, we see the opposite. The market thinks this is a boring name in a dying industry that is not going to be able to sustain these returns going forward.

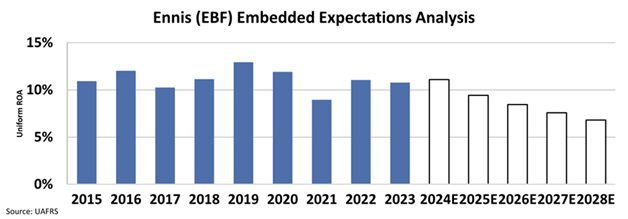

We can see this through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects the company’s ROA to fall significantly to 7%, the lowest it would be in the last eight years.

The market definitely doesn’t see the sustainability of Ennis’ returns.

Even though it is in a dying industry, the company has proved its ability to make money and it does not seem like that is going to change in the near future.

Especially when we are potentially heading into a recession, highly-stable names like Ennis could be a good place to put your money.

SUMMARY and Ennis, Inc. Tearsheet

As the Uniform Accounting tearsheet for Ennis, Inc. (EBF:USA) highlights, the Uniform P/E trades at 14.1x, which is below the corporate average of 18.4x but around its historical P/E of 14.3x.

Low P/Es require low EPS growth to sustain them. In the case of Ennis, the company has recently shown a 23% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Ennis’ Wall Street analyst-driven forecast is a 1% EPS shrinkage in 2023 and an immaterial growth in 2024.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Ennis’ $20.54 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 9% annually over the next three years. What Wall Street analysts expect for Ennis’ earnings growth is above what the current stock market valuation requires in 2023 but immaterial in 2024.

Furthermore, the company’s earning power is 2x its long-run corporate average. Moreover, cash flows and cash on hand are 3x its total obligations—including debt maturities, capex maintenance, and dividends. Also, the company’s intrinsic credit risk is 140bps above the risk-free rate.

All in all, this signals low dividend risk.

Lastly, Ennis’ Uniform earnings growth is in line with its peer averages and its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research