Rating agencies are mistaken about this dying business

There’s no doubt that print journalism is a dying industry. Almost everyone is getting their news from online sources or mobile applications nowadays.

This kills the demand for traditional media tools like printing, publishing, and broadcasting.

Because of this, rating agencies are highly concerned about these businesses and rated one of the leading ones, the News Corporation (NWSA), with a high chance of bankruptcy over the next few years.

Little do they know that the company is heavily invested in digital assets and is far from the average traditional media company.

Let’s have a look at the company using Uniform Accounting and see if it’s as risky as rating agencies suggest.

We can use Uniform Accounting to put the company’s real profitability up against its obligations and decide for ourselves the true risk of this business.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Print journalism is a melting ice cube business.

It used to be the biggest and best source for getting news. Back then, the fastest way to learn about something was in the morning newspaper.

However, the world has changed along with the media industry. The industry moved online, and now, the news flows are even faster than traditional print and broadcast media.

People can reach news in a matter of minutes from their smartphones, instead of waiting for the morning newspapers or the evening news on TV.

Additionally, so much media is free these days, and traditional media outlets are struggling to find ways to protect their edge as well.

All these factors show that these traditional media businesses have completely lost their competitive edge.

News Corporation (NWSA) is no exception to this.

It mostly owns lots of legacy publishing and broadcasting businesses left over after the 21st Century Fox brand was spun out.

Because of its reputation and the leftover traditional printing business, rating agencies don’t think highly of the company.

They expect that this business will keep whittling away and it won’t be able to pay off its obligations in the future.

That is why S&P gave a BB+ rating to the company, implying around a 10% chance of bankruptcy over the next few years and placing it in the risky high-yield basket.

But as it happens, the company has more modern media assets than rating agencies realize.

News Corporation owns about 27% of Hulu, a massive streaming platform. It also owns digital content ownership groups like Storyful that owns the rights to online videos, which provides a more stable revenue stream for the company.

Because of that, the company should not be evaluated the same way as the other pure-play print journalism companies. And accordingly, it should have a safer credit risk assessment.

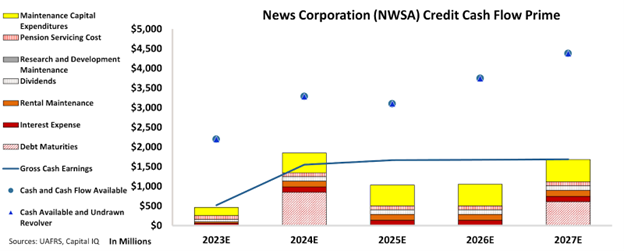

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (“CCFP”) to understand how the company’s obligations match against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart shows that News Corporation’s cash flows are more than enough to serve all its obligations going forward.

The chart shows that the company has two debt maturities in the next five years and that it can pay off this debt easily with its large cash flows.

Considering the company’s strategic positioning in the modern media industry and its significant investments in growing spaces like streaming and content ownership, its cash flows could even grow bigger as these spaces will gain more dominance in the overall media industry over the next few years.

These reasons show that the company deserves a much safer credit rating. That is why, at Valens, we are giving an IG4+ rating to this company.

This credit rating ensures that the company is placed within the investment-grade basket and implies a chance of bankruptcy of around 2%.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and News Corporation (NWSA:USA) Tearsheet

As the Uniform Accounting tearsheet for News Corporation (NWSA:USA) highlights, the Uniform P/E trades at 20.3x, which is above the global corporate average of 18.4x and its historical P/E of 16.4x.

High P/Es require high EPS growth to sustain them. In the case of News Corporation, the company has recently shown a 35% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations, that in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, News Corporation’s Wall Street analyst-driven forecast is for a -55% and 50% EPS growth in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify News Corporation’s $19 stock price. These are often referred to as market-embedded expectations.

Furthermore, the company’s earning power in 2022 was 3x the long-run corporate average. Moreover, cash flows and cash on hand is 2x its total obligations—including debt maturities and capex maintenance. The company also has an intrinsic credit risk that is 110bps above the risk-free rate.

Overall, this signals a moderate credit risk and a low dividend risk.

Lastly, News Corporation’s Uniform earnings growth is below its peer averages and is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research