This SaaS business won’t go down even if its customers do

In the dynamic world of business, where innovation and growth strategies often take center stage, the views of rating agencies can be critically influential.

These agencies tend to favor stability and a conservative approach, particularly when evaluating companies whose performance is closely linked to consumer spending.

The fluctuating nature of consumer markets often breeds a sense of uncertainty, leading to a cautious stance from rating agencies.

This caution is further amplified in the case of companies that grow through acquisitions, as this strategy introduces additional layers of complexity and risk.

Within this cautious landscape, EverCommerce (EVCM), a provider of SaaS solutions for service-based small and medium-sized businesses, faces a challenging scenario.

Despite demonstrating strong growth and operational success, its reliance on consumer spending and its acquisitive growth strategy has not endeared it to rating agencies, resulting in a generally guarded outlook towards the company.

Today, our focus will be on assessing the credit risk of EverCommerce through Uniform Accounting, to evaluate whether the rating agencies’ analysis of the company is fair.

We can use Uniform Accounting to put the company’s real profitability up against its obligations and decide for ourselves the true risk of this business.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

The integration of digital technology has played a major role in the rapid evolution of the landscape for small and medium-sized businesses (SMBs) that provide services.

This transformation has fundamentally altered how these businesses operate, ushering in a new era of opportunities and challenges in the digital marketplace.

Central to this shift are Software as a Service (SaaS) solutions, which have become indispensable in driving growth, streamlining operations, and enhancing customer engagement.

These digital tools are reshaping how service SMBs approach their markets, manage their operations, and interact with customers.

They are now essential for businesses that aim to thrive in a digital-centric environment.

In this evolving scenario, EverCommerce (EVCM) distinguishes itself.

The company provides a comprehensive range of SaaS solutions, covering areas such as marketing, business management, and customer experience software.

These integrated services go beyond merely boosting operational efficiency for SMBs; they are transforming the competitive environment, enabling businesses to excel in the digital age.

EverCommerce helps its customers expand their market reach, improve customer retention, and enhance overall growth.

The company has grown through acquisitions, having completed 52 since its founding in 2016.

In addition to its strategic acquisitions, a key to its success is the ‘land and expand’ strategy.

This strategy starts by attracting clients with a basic set of services and then gradually offering them more comprehensive solutions.

The company has recorded impressive results in recent years, including significant growth in the first half of 2023.

This period, marked by challenging macroeconomic conditions, has been tough for SMBs and consumer spending, yet the company’s resilience and adaptability have been standout features of its business model.

The company managed to increase its revenues by 10% compared to the prior year.

Despite these operational successes and clear demonstrations of growth, EverCommerce’s reliance on consumer spending markets and its acquisitive growth strategy have led to a cautious outlook from rating agencies.

Therefore, S&P gives the company a “B+” rating. This rating suggests a risk of default around 11% over the next five years. It also places the company in the risky high-yield basket.

Considering EverCommerce’s strong financial health and successful growth tactics, it seems the company should be assigned a safer credit rating.

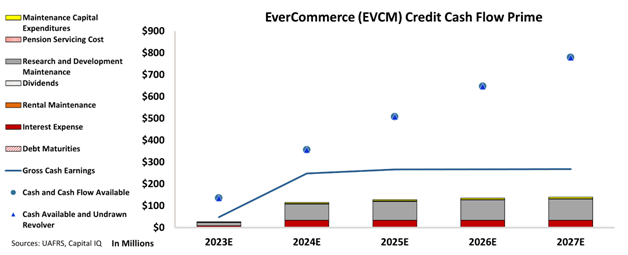

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (“CCFP”) to understand how the company’s obligations match against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart shows that EverCommerce’s cash flows are more than enough to serve all its obligations going forward.

The chart suggests that the company has a strong financial footing and should be able to meet its obligations without difficulty going forward.

Additionally, the company has no debt maturities staggered over the next five years.

Furthermore, the company is poised to boost its earnings through the implementation of its “land and expand” strategy.

Taking these into account, we believe that EverCommerce presents a low risk of default, contrasting with the opinions of rating agencies.

Thus, we are assigning an “IG3-” rating to the company. This rating ensures it is in the safer investment-grade basket and implies a risk of default of around just 1%.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and EverCommerce (EVCM:USA) Tearsheet

As the Uniform Accounting tearsheet for EverCommerce (EVCM:USA) highlights, the Uniform P/E trades at 13.7x, which is lower than the global corporate average of 18.4x, and its historical P/E of 17.7x.

Low P/Es require low EPS growth to sustain them. In the case of EverCommerce , the company has recently shown a 40% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations, that in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, EverCommerce’s Wall Street analyst-driven forecast is for a 26% EPS growth and a 16% EPS growth in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify EverCommerce’s $8 stock price. These are often referred to as market-embedded expectations.

Furthermore, the company’s earning power in 2022 was 8x the long-run corporate average. Moreover, cash flows and cash on hand are more than 2x its total obligations—including debt maturities and capex maintenance.

Overall, this signals a low credit risk.

Lastly, EverCommerce’s Uniform earnings growth is in line with its peer averages, and is trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research