This company is transforming Southeast Asia’s service industry

Southeast Asia is growing fast, thanks to its large, young population and improvements in doing business.

These factors are attracting investments, and helping local companies like Grab Holdings (GRAB) to grow.

Grab, which started as a ride-hailing app, has now become a super-app providing various services in eight countries.

However, concerns over the geopolitical risks and economic instability in the region have caused ratings agencies like S&P to be cautious about the name.

Today, we’re exploring Grab’s credit risk through the lens of Uniform Accounting to determine the accuracy of rating agencies’ assessments of the company.

We can use Uniform Accounting to put the company’s real profitability up against its obligations and decide for ourselves the true risk of this business.

Also below is a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Southeast Asia is a region that has been experiencing strong and steady growth in the last decades.

The drivers of this growth are many…

Southeast Asia has a growing young population with more than 675 million people, who are much more tech-savvy than older generations. This large and growing working-age population provides a strong labor force and a significant consumer base.

This has caused the region to become a global hub of innovation and manufacturing, with many companies scaling up impressively in recent years.

Additionally, the region has also made steady progress in improving the ease of doing business, including the process of starting a business, getting credit, and resolving insolvency.

As a result, Southeast Asia is not only attracting global investment but is also seeing the rise of homegrown companies that are making significant impacts both locally and internationally.

One noticeable example of these homegrown companies is Grab Holdings (GRAB).

Born out of humble beginnings as a taxi-hailing app in 2012, Grab has since expanded its vision and scale to address a wider array of needs across Southeast Asia.

Today, the company operates as the region’s leading super-app with offerings like ride-hailing, food delivery, and digital payments. Grab’s reach spans over 500 cities in eight countries.

The company’s investments in technology ensure a robust and user-friendly platform, while its data analytics capabilities optimize operations, personalize user experiences, and offer targeted promotions.

As Grab continues to innovate and expand, it aims to be Southeast Asia’s go-to platform for everyday services, transforming the way people move, eat, and transact in the region.

However, rating agencies are concerned about the geopolitical risks and economic instability in the region hurting the company going forward.

S&P gave the company a “B” rating, indicating a significant risk of default at nearly 25% over the next five years. It also puts the company in the risky high-yield basket.

Given its solid financial standing, we believe Grab deserves a more secure rating.

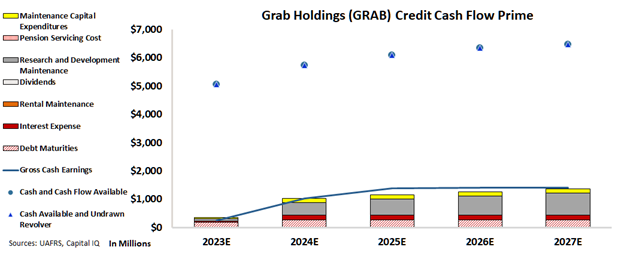

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (“CCFP”) to understand how the company’s obligations match against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart shows that Grab’s cash flows alone are more than enough to serve all its obligations going forward.

The chart indicates that the company is on solid financial ground and is very likely to fulfill its obligations with ease in the next five years.

The company has limited debt maturities in the next 5 years and it can easily handle its obligations with its massive cash flows.

Moreover, with the continuing growth in the region, Grab also has opportunities to sustain and even increase high profitability levels over the long run.

Our review of Grab shows that the company has a low risk of default, contrary to what rating agencies indicate.

Therefore, we are assigning an “IG4+” rating to the company, which places it in the investment-grade basket, with a risk of default of only about 2%.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Grab Holdings (GRAB:USA) Tearsheet

As the Uniform Accounting tearsheet for Grab Holdings (GRAB:USA) highlights, the Uniform P/E trades at 25.5x, which is above the global corporate average of 22.4x, but below its historical P/E of 92.9x.

High P/Es require high EPS growth to sustain them. In the case of Grab, the company has recently shown a 94% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations, that in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Grab’s Wall Street analyst-driven forecast is for a 97% and 936% EPS shrinkage in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Grab’s $3 stock price. These are often referred to as market-embedded expectations.

The company’s earning power in 2022 was below the long-run corporate average. However, cash flows and cash on hand are 5x its total obligations—including debt maturities and capex maintenance. The company also has an intrinsic credit risk that is 60bps above the risk-free rate.

Overall, this signals a low credit risk.

Lastly, Grab’s Uniform earnings growth is below its peer averages and is trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research