Elliot Capital Management has the British pharma company GlaxoSmithKline in its crosshairs

For some investors, the patient process of identifying companies with solid fundamentals and long-term growth opportunities, then allowing compound interest to work its magic, is simply not enough to entice.

Today we’ll take a look at one such investor who is feared by corporate management teams around the world, and use Uniform Accounting to understand the target of its latest activist campaign.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

We’ve talked before here at Valens about activist hedge fund manager Paul Singer and his fund Elliot Capital Management. The team there loves few things more than sharp-eyed lawyers and an opportunity to shake up management teams.

As a matter of fact, just over the past few weeks, we have seen another example of Elliott Management’s activism, as the fund turned its attention to U.K. pharmaceutical giant GlaxoSmithKline (LSE:GSK) in one of its latest campaigns.

GlaxoSmithKline is a large player in the pharmaceutical space, with a market value of over $70 billion and sales spanning countries all over the world.

The company has already been in the midst of a focused turnaround in recent years, seeking to spin off its consumer products businesses, such as Advil pain relief and Nicorette chewing gum. Management wants to focus on vaccine research—unrelated to COVID-19—which currently makes up one-fifth of the business.

Historically, GlaxoSmithKline was the world’s largest vaccine manufacturer by revenue before the onset of COVID-19, producing jabs aimed at the likes of meningitis, hepatitis, and influenza.

However, the outbreak of the novel coronavirus in 2020 and the resultant rush to produce vaccines led to other shot-makers quickly surpassing the British firm.

Utilizing our Uniform Accounting data and Embedded Expectations framework, it is fairly obvious why Singer and Elliot Management have chosen right now as the best time to target the firm.

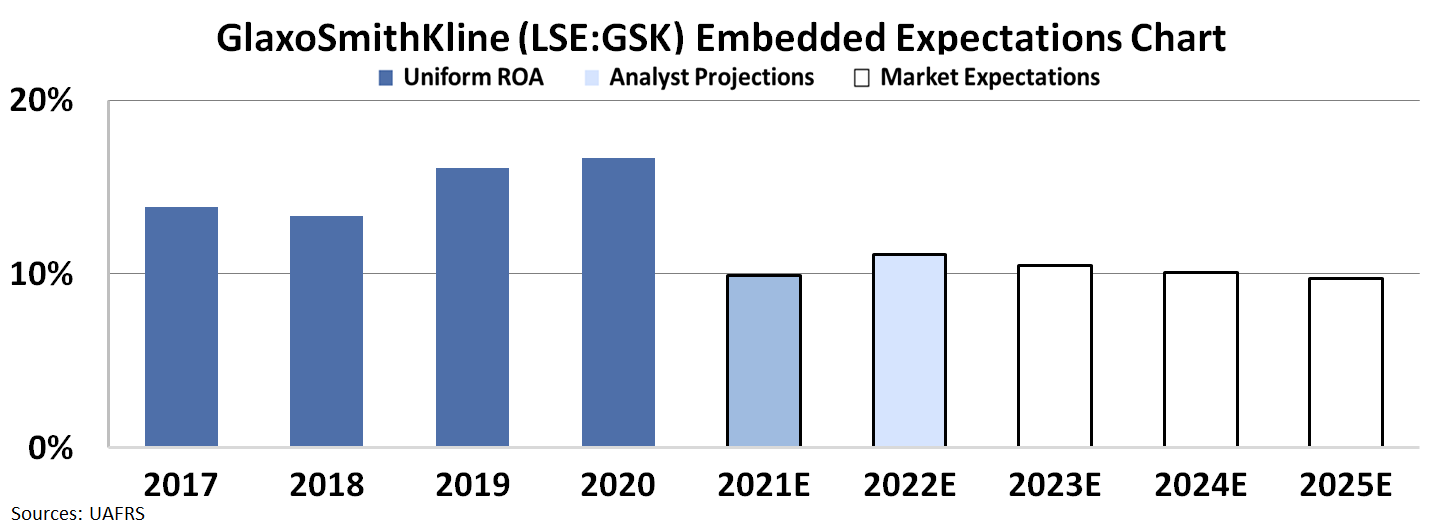

While CEO Emma Walmsley has done an impressive job boosting Uniform return on assets (“ROA”) from 7% to 17% since taking over the top spot in 2017, Uniform ROA is forecast by analysts to be cut down by over a third in 2021 to a paltry 10%, representing a complete revaluation of the firm’s profitability.

In the chart below, the dark blue bars represent GlaxoSmithKline’s historical corporate performance levels in terms of ROA. The light blue bars are Wall Street analysts’ expectations for the next two years. Finally, the white bars are the market’s expectations for how the company’s ROA will shift over the next five years.

As the Embedded Expectations analysis shows, the market doesn’t believe anything is coming to save the firm anytime soon, as market expectations are for ROA to remain at 10% levels going forward.

It appears Elliot Management’s plan may be to force a management change, with the reasoning being that it might be able to boost innovation and stave off the expected decline in returns.

In the worst case scenario, Singer may even opt to sell off pieces of the business for today’s prices before the market drives them down any further.

In any case, trouble appears to be brewing at GlaxoSmithKline, and investors may be hesitant to stick around and find out how one of the hedge fund industry’s most powerful activists proceeds.

SUMMARY and GlaxoSmithKline plc Tearsheet

As the Uniform Accounting tearsheet for GlaxoSmithKline plc (GSK:GBR) highlights, the Uniform P/E trades at 19.3x, which is below the global corporate average of 21.9x but above GlaxoSmithKline’s historical P/E of 15.8x.

Low P/Es require low EPS growth to sustain them. In the case of GlaxoSmithKline, the company has recently shown a 6% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, GlaxoSmithKline’s Wall Street analyst-driven forecast is a 30% EPS shrinkage in 2021 and a 17% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify GlaxoSmithKline’s GBP 14 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink 10% annually over the next three years. What Wall Street analysts expect for GlaxoSmithKline’s earnings growth is below what the current stock market valuation requires in 2021, but above that requirement in 2022.

Furthermore, GlaxoSmithKline’s earning power in 2020 is 3x the long-run corporate average. However, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low credit, but high dividend risk.

To conclude, the company’s Uniform earnings growth is below its peer averages, and the company is also trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research