Ratings agencies are blind for missing the real story in the insulation industry, leaving this company totally misunderstood

Some industries have thrived during the pandemic. One of these has been the home improvement sector, as consumers are spending more time in their homes.

Today’s company provides all the parts of the home you hope to never have a problem with, as they are some of the most essential. Despite this, rating agencies have viewed the company as a high credit risk.

Below, we show how Uniform Accounting restates financials for a clear credit profile. We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Last week, we talked about Masonite International (DOOR) and how it has benefitted from the At-Home Revolution. There is surging demand for home improvement and new homes, leading to stronger cash flows. Nevertheless, the rating agencies have still missed these tailwinds.

However, it is not only doors benefitting from the wave of demand. All parts of the home improvement industry are seeing a demand spike.

This includes companies that make insulation for homes, or moisture protection systems and sealants. These are parts of the home that owners rarely think about unless there is a problem.

Installed Building Products (IBP) is a leading name in the insulation industry. Those building or renovating a home are most likely familiar with the value of the company’s products.

Installed Building Products installs insulation, waterproofing, fire-stopping, rain gutters, window blinds and more. The firm’s products are used by homebuilders, construction firms, contractors and individual homeowners.

Installed Building Products is benefitting from increased demand seen during the pandemic. Homeowners are renovating their houses and need the company’s services in insulating these new additions.

Additionally, new housing starts are at record highs, meaning homebuilders are increasingly turning to the firm to seal newly built homes.

And yet, similar to Masonite last week, the rating agencies seem to think the company has a looming credit risk. Moody’s rates the firm a high-yield B1. This implies a default rate of close to 25% over the next five years.

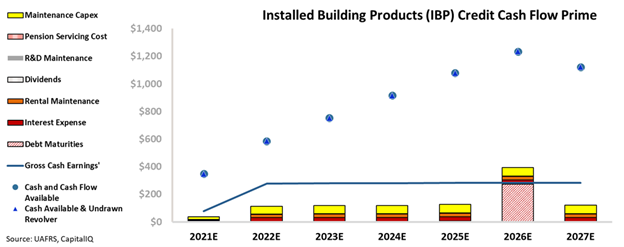

However, looking at the firm’s Credit Cash Flow Prime (CCFP) highlights the true safety of the firm’s credit.

The firm’s cash flows should exceed obligations until 2025, when the firm encounters a material debt headwall. In addition, Installed Building Products has a sizable cash balance that is expected to build to cover all existing obligations.

The company’s first debt maturity is not until six years out, which gives the firm ample time to plan around. Additionally, the pandemic tailwinds should drive increased business and cash flows on top of the already sizable cash balance.

Factoring in its strong liquidity position and fundamental tailwinds, Valens rates Installed Building Products as a much safer investment grade IG3 (A2) credit. This would imply an expected default rate of only around 1%, far less than the 25% predicted by Moody’s.

Ultimately, Installed Building Products is seen as having a high credit risk because rating agencies are looking at traditional metrics and misunderstanding the firm’s cash flows.

However, when looking at Installed Building Product’s CCFP from a Uniform Accounting perspective, the firm’s minimal credit risk can be seen. Even without the At-Home Revolution tailwinds, it is obvious the firm should have no trouble meeting obligations.

This is why the company is a safer credit risk than what Moody’s gives it credit for.

Moody’s Grossly Overstate IBP’s Credit Risk Despite Operating Sustainability and Strong Liquidity

Credit markets are accurately stating credit risk with a cash bond YTW of 4.249% relative to an Intrinsic YTW of 4.049% and an Intrinsic CDS of 320bps. Meanwhile, Moody’s is grossly overstating IBP’s fundamental credit risk, with its speculative B1 rating eight notches below Valens’ IG3 (A2) rating.

Fundamental analysis highlights that IBP’s cash flows should comfortably exceed operating obligations every year going forward.

Additionally, the combination of the firm’s cash flows and substantial cash on hand should be sufficient to service all obligations including debt maturities through 2026. This is important as the firm’s neutral 50% recovery rate and moderate market capitalization may make it difficult for it to access credit markets to refinance at favorable rates.

Incentives Dictate Behavior™ analysis highlights mixed signals for credit holders. IBP’s compensation framework should drive management to focus on EBITDA improvement, which may be negative for debt holders as it does not punish management for taking on excessive leverage or overspending on assets to drive growth.

That said, management is not well-compensated in a change-in-control situation, indicating they may not be incentivized to seek a sale of the company or accept a buyout, reducing event risk. Additionally, the management team holds material amounts of equity relative to their annual compensations, suggesting they are incentivized to create long-term value for shareholders.

Earnings Call Forensics™ of the firm’s Q2 2020 earnings call (8/6) highlights that management is confident about their ability to improve adjusted EBITDA.

However, management may lack confidence in their ability to continue expanding their multi-family and large commercial construction end markets, especially if coronavirus cases stay elevated. Moreover, they may lack confidence in the sustainability of lower fuel costs, and they may be concerned about the current labor market and the sustainability of their improving net sales.

Additionally, they may be concerned about their same branch sales volume and their ability to install and repair appliances during the pandemic. Finally, management may lack confidence in their ability to efficiently allocate capital towards acquisitions.

Operating sustainability and strong liquidity indicate ratings agencies are overstating fundamental credit risk. As such, a ratings improvement is likely going forward.

SUMMARY and Installed Building Products, Inc. Tearsheet

As the Uniform Accounting tearsheet for Installed Building Products (IBP:USA) highlights, the company trades at an 18.6x Uniform P/E, which is below global corporate average valuation levels, but around its own historical average valuations.

Low P/Es require low EPS growth to sustain them. In the case of Installed Building Products, the company has recently shown a 17% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Installed Building Products’ Wall Street analyst-driven forecast projects a 36% and 34% EPS growth in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Installed Building Products’ $100.58 stock price. These are often referred to as market embedded expectations.

The company needs to grow its Uniform earnings by 10% each year over the next three years to justify current prices. What Wall Street analysts expect for Installed Building Products’ earnings growth is above what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is 4x the corporate average, but intrinsic credit risk is 310bps above the risk-free rate. Together, this signals moderate credit risk.

To conclude, Installed Building Products’ Uniform earnings growth is around peer averages, but the company is trading well above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research