Rating agencies account for too much credit risk for this company

Most of the biotech and pharmaceutical companies have stayed unprofitable for so many years, making investors wonder if those really can make money.

With the pandemic, we understood how innovation in this space is crucial for our lives, and how profitable these companies can be with these innovations.

There’s one missing point in this sector though, as most people do not recognize how clinical research organizations (CROs) are critical in these innovation processes.

Like most people, it seems like credit rating agencies fail to recognize their importance in the sector as well, since they rate one of the largest CROs, ICON Public Limited Company (ICLR), with a very high chance of bankruptcy.

Let’s have a look at the company through the eyes of Uniform Accounting and see if it really has that much risk as rating agencies recommend.

We can use Uniform Accounting to put the company’s real profitability up against its obligations and decide for ourselves the true risk of this business.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

The biotechnology and pharmaceutical sector has different dynamics relative to many of the other industries globally.

They focus on innovation and need constant capital investments to keep on going in order to create a viable medicine or product.

It’s the nature of this business and one reason why lots of biotech and pharmaceutical companies stayed unprofitable for so many years.

However, the pandemic changed this perception towards these companies as people realized once again that the innovation coming from this space is critical to our lives.

And with the emergence of the pandemic, innovation in the space started to ramp up as well.

This continued innovation growth in biotech and pharma led to a massive demand for clinical research organizations (CROs).

These organizations are at the heart of innovation in these sectors since they help to manage clinical trials as well as offer strategic development and analysis of programs that support various stages of the clinical development process.

As trials are getting more and more complex, the biotech and pharma sector realized that they shouldn’t specialize in this and should just focus on innovation.

This has led to massive profitability for CROs. One great example of this is ICON Public Limited Company (ICLR).

The company’s return on assets (ROA) before the pandemic, in 2019, was just around 32%. However, the emergence of the pandemic and the continued growth in innovation drove its ROA up to 54% in 2021.

Yet, rating agencies seem not to understand the business and rate it with a 10% chance of default.

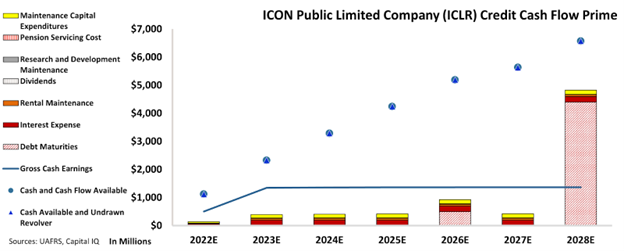

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (“CCFP”) to understand the company’s obligations matched against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart shows that ICON Public Limited Company’s cash flows are always above its obligations going forward.

CCFP chart indicates that the company does not have any debt maturities in the next few years and its cash and cash flows are way above its obligations.

The company only has debt maturities in 2026 and 2028, which could be refinanced by that time. Even if refinancing wouldn’t be an option, its cash on hand is enough to cover these obligations.

Additionally, its critical role in the innovation process for biotech and pharma sectors combined with its increasing demand and strong financial positioning accounts for a much safer credit risk than what rating agencies suggest.

That is why, we are giving a rating of IG3- for the company, which implies around just a 1% chance of default.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and ICON Public Limited Company (ICLR:USA) Tearsheet

As the Uniform Accounting tearsheet for ICON Public Limited Company (ICLR:USA) highlights, the Uniform P/E trades at 23.3x, which is above the global corporate average of 18.4x and its historical P/E of 22.2x.

High P/Es require high EPS growth to sustain them. In the case of ICON, the company has recently shown a 31% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, ICON’s Wall Street analyst-driven forecast is for a 15% and 4% EPS growth in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify ICON’s $228 stock price. These are often referred to as market embedded expectations.

Furthermore, the company’s earning power in 2021 was 9x the long-run corporate average. Moreover, cash flows and cash on hand are 5x its total obligations—including debt maturities and capex maintenance. The company also has an intrinsic credit risk that is 80bps above the risk-free rate.

Overall, this signals a low credit risk.

Lastly, ICON’s Uniform earnings growth is above its peer averages and is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research