The macro outlook shouldn’t be the only factor for rating agencies

Ever since the pandemic, the housing market has been in upheaval with increasing demand for homes. The real estate sector, and specifically homebuilders have enjoyed this trend for the last three years until March 2022, when the Fed started raising interest rates.

However, as interest rates started to rise aggressively and concerns for an economic downturn increased, people thought demand for homes will take a significant hit and home prices will decline in the short-term future.

It seems rating agencies shared the same idea and were highly concerned about these issues, which led them being overly cautious with their credit risk assessments for homebuilders.

KB Home (KBH) is one of these companies. It builds and sells single-family residential homes primarily for first-time home buyers.

Today, we will analyze KB Home’s credit risk profile using Uniform Accounting and see whether rating agencies gave the company a reasonable assessment or just evaluated it without taking into account company-specific factors.

We can use Uniform Accounting to put the company’s real profitability up against its obligations and decide for ourselves the true risk of this business.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Many people thought rising rates and looming recession would end the positive trend in the housing sector.

Expectations were focused on significant decline in demand for homes and consequently decreasing home prices.

Surprisingly, many people were wrong…

The demand surely has declined but aggressively, rising rates made people discouraged from selling their homes as they became reluctant to give up their relatively low mortgage rates.

This led to low levels of supply as existing home sales and new residential construction activity has declined substantially.

On top of that, some people still needed to buy a home due to important reasons like getting married, starting a family, and pursuing employment or education in a different area.

Due to this imbalance in supply and demand, home prices rose to its highest level since October 2022 despite high mortgage rates. So, instead of being the end of the housing boom, these macroeconomic issues led to another rally for homebuilders in 2023.

The S&P Homebuilders ETF (XHB) has increased by around 32% year-to-date, while the overall market has been up by around 17%. This could be a sign that the homebuilding sector has remained strong in the first half of the year.

However, it seems that rating agencies couldn’t realize these surprising side effects and continued on their negative outlook on homebuilders.

KB Home is one of the companies that was victimized along with the overall homebuilding sector. The company is primarily focused on building and selling single-family residential homes for first-time, first move-up, second move-up, and active adult homebuyers.

This means that its target market mostly consists of people that need to buy a home to establish a foundation for their lives, which makes the company less sensitive to declining demand relative to the overall housing market.

So, while the long term future might not be that bright for homebuilders even though they had a good half of the year and took advantage of the positive side effects of rising rates, it’s important not to put all of them in the same basket. That is what exactly rating agencies missed with this company.

For instance, KB Home received a “BB” credit rating from S&P, which denotes a substantial risk of default at around 11% in the next five years and places the company among the risky high-yield basket.

We think that it should have a higher credit rating considering its low levels of debt, financial health and its positioning in the homebuilding sector.

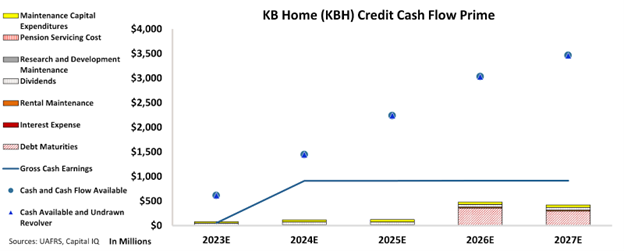

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (“CCFP”) to understand how the company’s obligations match against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart indicates that KB Home’s cash flows are more than sufficient to meet all of its financial obligations in the future.

The chart implies that the company has a solid financial foundation and should be able to meet its obligations without difficulty in the next five years.

Also, the debt maturities coming in 2026 and 2027 seem tiny compared to its massive cash flows.

As a result, being relatively less sensitive to economic downturns due to nature of its target market and having significant flexibility to cover obligations going forward makes KB Home a less risky business compared to the overall homebuilding sector.

That is why, we give an “IG3+” rating to the company. This rating places the company in the investment-grade basket and suggests a risk of default of only about 1%, as opposed to S&P’s overly concerned 11%.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and KB Home (KBH:USA) Tearsheet

As the Uniform Accounting tearsheet for KB Home (KBH:USA) highlights, the Uniform P/E trades at 6.9x, which is below the global corporate average of 18.4x, but around its historical P/E of 6.4x.

Low P/Es require low EPS growth to sustain them. In the case of KB Home, the company has recently shown a 16% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations, that in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, KB Home’s Wall Street analyst-driven forecast is for a 2% EPS growth and an immaterial EPS shrinkage in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify KB Home’s $65 stock price. These are often referred to as market-embedded expectations.

Furthermore, the company’s earning power in 2022 was 3x the long-run corporate average. Moreover, cash flows and cash on hand are 6x its total obligations—including debt maturities and capex maintenance. The company also has an intrinsic credit risk that is 130bps above the risk-free rate.

Overall, this signals a low dividend risk.

Lastly, KB Home’s Uniform earnings growth is above its peer averages but is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research