Nuclear technology is saving lives, but credit agencies miss Lantheus’ role in it

Nuclear technology can sound intimidating, and there is a good reason for that. One of its first uses was the atomic bomb.

But right now, this technology plays a vital role in saving lives. It is essential for the diagnostics and treatment of many deadly diseases like cancer.

Lantheus (LNTH) is a major supplier of this industry and finds itself in a strong position, but the credit agencies totally miss the reality.

We can use Uniform Accounting to compare the company’s obligations with its cash flows and decide for ourselves the true risk of the business.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

People tend to not associate nuclear technology with many good developments. The term generally brings to mind nuclear weapons and disasters like Chernobyl and Fukushima.

However, the ability to split the atom has not only unlocked one of the deadliest weapons in human history, but also saves lives every day.

Nuclear technology goes beyond war and power. It also plays a vital role in healthcare.

Radiation is used to help fight cancers and is essential for many of the imaging technologies we use to diagnose our health issues.

This technology also enables tracking animal diseases even before they transfer to humans.

It is a huge industry with lots of suppliers. Lantheus Holdings (LNTH) is one of them.

The company is a major supplier in this industry, making nuclear isotopes and imaging technology. It also provides other imaging improvement solutions.

These products assist clinicians in the diagnosis and treatment of heart disease, cancer, and other diseases worldwide.

While a small portion of revenues comes from international sales, operations of the company are mainly in the U.S.

As innovations around cancer treatment and healthcare gain pace, Lantheus has found itself under the spotlight.

Developments in healthcare mean that treatments tailored for patients are more important now than ever before, which implies higher demand for Lantheus’ custom-tailored products.

However, credit agencies seem to miss this trend and Lantheus’ strong position to benefit from it.

Even with booming demand, they think there is a 25% chance the company will go bankrupt with a B+ rating.

Seeing the company’s ability to leverage its position in the industry, this rating makes no sense.

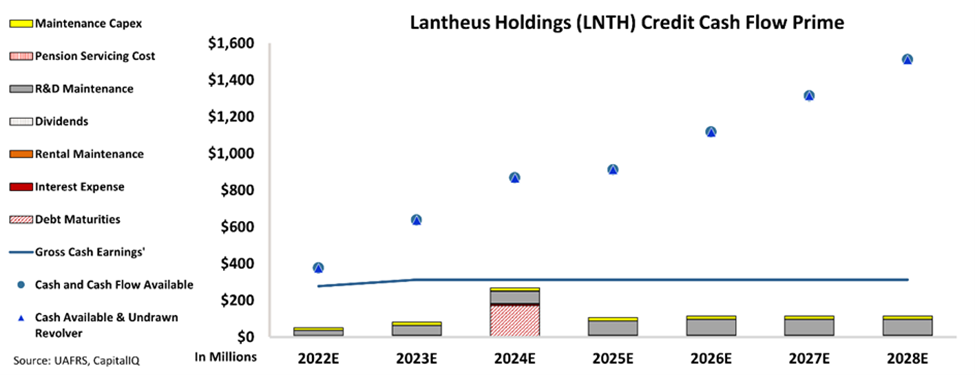

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (CCFP) to understand the company’s obligations matched against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

As evidenced by the following chart, Lantheus has a much safer credit profile than the credit agencies have been suggesting.

The CCFP clearly shows that the cash inflow of the company is enough to cover operating and financial obligations for the next seven years.

Contrary to what the rating agencies think, there is no real risk of default.

As a result, the company gets an IG3+ rating from Valens.

With the increased pace of innovations in healthcare and cancer treatment, Lantheus is in perfect condition to take advantage.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Lantheus Holdings Tearsheet

As the Uniform Accounting tearsheet for Lantheus Holdings, Inc. (LNTH:USA) highlights, the Uniform P/E trades at 18.6x, which is around the global corporate average of 19.3x and its historical P/E of 17.8x.

Average P/Es require average EPS growth to sustain them. In the case of Lantheus, the company has recently shown a 6% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Lantheus’ Wall Street analyst-driven forecast is for a 265% and 14% EPS growth in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Lantheus’ $74 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 21% annually over the next three years. What Wall Street analysts expect for Lantheus’ earnings growth is well above what the current stock market valuation requires in 2022 but below in 2023.

Furthermore, the company’s earning power in 2021 is 3x the long-run corporate average. Also, cash flows and cash on hand are 3x its total obligations—including debt maturities and capex maintenance. However, the company has an intrinsic credit risk that is 250bps above the risk-free rate. Overall, this signals a moderate credit and dividend risk.

Lastly, Lantheus’ Uniform earnings growth is well above its peer averages, but the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research