Not Every Acquirer Carries Credit Risk

In an exceptionally uncertain economic environment with concerns about a recession on the horizon, businesses in a variety of industries are reconsidering their strategies for growth.

Rating agencies have been more cautious during this period of macroeconomic instability, especially with regard to companies that are actively pursuing growth through acquisitions.

As we previously mentioned, rating agencies frequently view such expansion efforts with skepticism that might end up in less favorable credit ratings.

Molina Healthcare (MOH), during these challenging times, finds itself in a similar situation.

Today, we will delve into examining Molina Healthcare’s credit risk, using Uniform Accounting to determine if the concerns of rating agencies about the company’s financial standing are legitimate.

We can use Uniform Accounting to put the company’s real profitability up against its obligations and decide for ourselves the true risk of this business.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Acquisitions, while a powerful tool for growth, often come with heightened risks, especially in uncertain economic times.

Macro headwinds can amplify the challenges associated with acquisitions, such as increased costs of debt and the potential for unsuccessful integration of acquired companies.

In this climate, Molina Healthcare’s (MOH) acquisition strategy stands out. It is a managed care company that primarily provides health insurance services through government programs such as Medicaid and Medicare.

While Medicaid provides long-term support and services to low-income individuals, the Medicare program serves people who are disabled or over 65.

The company has been actively pursuing acquisitions to bolster its position in the healthcare sector.

Molina Healthcare has been intentional in its acquisition objectives, focusing on businesses that provide complementary services or broaden its geographic reach.

This calculated approach is crucial in times of economic instability because it allows for growth without overextending the company’s resources or taking on excessive risk.

Recent acquisitions by Molina Healthcare illustrate this strategy.

In 2020, the acquisition of Magellan Complete Care for $820 million added significant value to Molina’s portfolio, bringing in 155,000 Medicaid and Medicare dual beneficiaries and enhancing the company’s presence in three additional key states.

This acquisition, along with others, is not just about expanding the size of the company but also about enhancing the quality and reach of its services, which is crucial for sustainable growth in the healthcare industry.

In addition to acquiring companies, Molina Healthcare also buys various assets from entities.

These assets include expanded member bases, established provider networks, operational contracts and licenses, physical and technological infrastructure, experienced staff, and brand value to enhance its service offerings and market presence.

This acquisition strategy seems to be successfully implemented by the company as it has been able to increase its Uniform return on assets (“ROA”) in only four years from 8% in 2018 to 24% in 2022.

Nevertheless, despite Molina Healthcare’s significant improvement in profitability and earnings, it appears that rating agencies are primarily concerned about its aggressive acquisition strategy.

For instance, S&P gives Molina Healthcare a “BB-” rating. This rating suggests a risk of default around 11% over the next five years. It also places the company in the risky high-yield basket.

Given its established acquisition strategy and present financial condition, we believe it deserves a significantly safer credit grade.

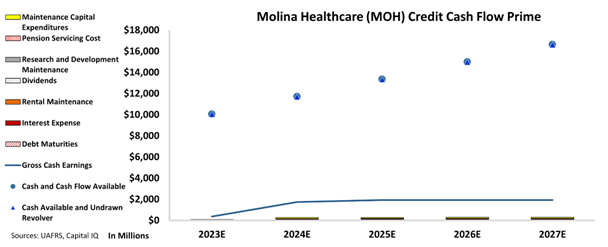

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (“CCFP”) to understand how the company’s obligations match against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart shows that Molina Healthcare’s cash flows are more than enough to serve all its obligations going forward.

The chart suggests that the company has a strong financial footing and should be able to meet its obligations without difficulty going forward.

It has highly limited debt maturities going forward which does not appear to be an issue given its massive cash flows.

Furthermore, as it expands through its outstanding acquisition strategy, its profitability may climb even further.

Therefore, we believe Molina Healthcare does not face a major risk of default, contrary to what the rating agencies perceive.

Thus, we are giving an “IG3+” rating to the company. This rating ensures it is in the safer investment-grade basket and implies a risk of default of around just 1%.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Molina Healthcare (MOH:USA) Tearsheet

As the Uniform Accounting tearsheet for Molina Healthcare (MOH:USA) highlights, the Uniform P/E trades at 17.1x, which is below the global corporate average of 18.4x and its historical P/E of 18.2x.

Low P/Es require low EPS growth to sustain them. In the case of Molina Healthcare, the company has recently shown a 49% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations, that in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Molina Healthcare’s Wall Street analyst-driven forecast is for a 17% and a 16% EPS growth in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Molina Healthcare’s $367 stock price. These are often referred to as market-embedded expectations.

Furthermore, the company’s earning power in 2022 was 4x the long-run corporate average. Moreover, cash flows and cash on hand are 15x its total obligations—including debt maturities and capex maintenance. The company also has an intrinsic credit risk that is 78bps above the risk-free rate.

Overall, this signals a low credit risk.

Lastly, Molina Healthcare’s Uniform earnings growth is above its peer averages and is trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research