There’s more to the debt ceiling crisis than what’s being discussed

All anyone wants to discuss is the debt ceiling.

If you’ve been reading the news recently, you’ve likely seen the discussions around the U.S.’ huge amount of debt.

With everyone commenting on it, it might get confusing.

The story is simple: Congress is using the opportunity of the U.S. having to raise its debt ceiling (to pay for bills it already agreed on, not about spending) to make the government think how to be more responsible on its accounting.

The country has run at a deficit for a while. The U.S.’ total public debt has exceeded its gross domestic product (“GDP”) since the end of 2012 and it’s now 20% greater.

The Republican Congress is focusing on how we can cut costs, while the Democratic side, plus President Biden wants to focus on how we can increase revenue (raise taxes).

Either way, the focus is a classic game of chicken.

Each side is using the issue to try to get something they want, and the negotiations will continue until the 11th hour.

What’s likely to happen is that each side will show an effort in negotiating to show the U.S. voters they’re making a good faith gesture to avoid a default, until one side starts to come ahead in the public opinion polls.

The side that’s behind in the polls will cave at the last moment and then we’ll finally get a deal passed.

There’s something else to discuss, though. As we’ll explain today, folks should pay attention to what actually drives the country’s ability to borrow and if there’s any reason to worry about our ability to pay our debts.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

The U.S. is as safe of a borrower as ever.

In the news, the main story about the debt ceiling is whether it will be increased so the U.S. can borrow more.

However, we also need to discuss the government’s ability to pay its current debt obligations, since that’s relevant to whether or not we ought to raise our borrowing limit.

There’s a simple reason not to worry – the U.S. still remains a global superpower. The U.S.’ positioning in the world hasn’t changed.

We are still spending more on research and development (“R&D”) as a percent of GDP than Europe and China. And that’s leading to a consistent stream of innovations, exporting high-tech and energy products.

As of 2020, U.S. companies had over three times more innovation assets on their balance sheets than China.

American businesses are set up to benefit from the supply-chain supercycle as there’s strong demand for goods and services coming out of the pandemic.

The U.S. is the largest public market by far. Almost 60% of the total equity market value of the world is in the U.S. The next closest country is Japan at 6%.

As a result, U.S. companies are propelling the country upwards and leading us to future success.

This makes the U.S. dollar (“USD”) strong. It is still the world’s reserve currency, despite people worrying it won’t be. Countries have to deal in USD to participate in world markets, increasing the U.S.’ ability to borrow.

Additionally, when we look at the U.S.’ debt and income like financial statements, we can see the U.S. can easily handle its debts.

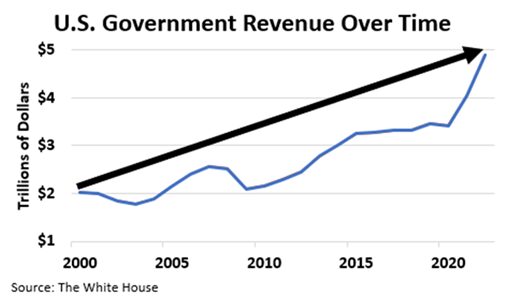

Specifically, the U.S. can spend less than it collects because its tax revenue continues to rise. It hit $4.9 trillion in 2022.

Take a look.

On the other hand, when looking at the expense side, it can easily afford the annual cost of its debt. In 2022, this was $420 billion, and this shouldn’t rise considerably, even as interest rates have soared this year.

Even if the U.S. did get to the point where we struggled to continue making debt payments, it has plenty of assets it could sell.

There are over $400 trillion worth of government assets to be used as collateral.

Therefore, the U.S. can afford its debt.

There’s no reason for the U.S. to go default in the short-term, and worries are out of place. We’re just a few weeks away from the June 1 debt ceiling headwall, and we don’t think there’s any reason to worry that we’ll fail to reach an agreement.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research