Credit-focused investors can be slow during a market rebound, and this homebuilder is poised for a second look

Some industries have thrived during the pandemic. One of these has been the homebuilding industry, due to more people moving to the suburbs. People are looking to leave cramped apartment buildings and want the space provided by suburban homes.

Today’s company is a homebuilder in some of the hottest regions of the country. The firm has operations across the south and southwest, some of the most sought after destinations in the country.

Below, we show how Uniform Accounting restates financials for a clear credit profile. We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

We have highlighted in several of the last few credit IEDs how ratings agencies are skeptical about the sustainability of home demand. Just in the last few weeks, we wrote about a similar trend for Installed Building Products (IBP) and Masonite International (DOOR).

The market is treating increased home starts as a fad, rather than a sustained trend. During the pandemic, people have begun to move out of urban areas, looking for more space. Lockdowns have made consumers weary of small, cramped apartments in big cities.

As any credit investor would tell you, the field specializes in understanding and minimizing downside, as they are more risk-focused. However, they are also behind on the upside, again due to being risk averse and hesitant to make the first move when the market starts rebounding.

Since credit investors are not thinking about the upside, they are missing the transformation occurring in home improvement due to the “At-Home Revolution”.

One company that credit markets and rating agencies are totally missing in this space is Meritage Homes Corporation (MTH).

Meritage constructs single-family homes across the United States. Some of its biggest markets include Arizona, California, Texas, Florida, North Carolina, and Tennessee. People are leaving cold, northern cities, and heading to these warmer suburban areas.

Despite the strength of the homebuilding market, rating agencies are still pessimistic about Meritage. Moody’s gives the firm a Ba2 rating. This implies a greater than 10% risk of default over the next five years.

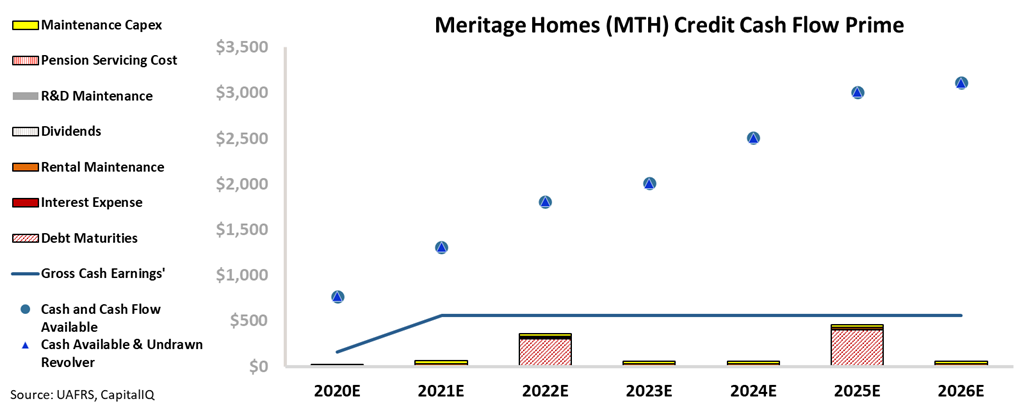

However, looking at the firm’s Credit Cash Flow Prime (CCFP), we can see just how safe Meritage’s credit is.

The firm’s cash flows should be sufficient to meet all outstanding obligations through 2026, including debt maturities. The expected cash build provides an even greater buffer.

This is not even taking into account the strength of the home building market and the potential to improve cash flows. Investors do not even need to believe in the “At-Home Revolution” for these ratings to make no sense.

Valens thus rates the firm at a much safer IG3+ credit. This implies a risk of default of only around 1%, a far cry from the 10%+ risk seen from Moody’s ratings.

Ultimately, rating agencies are missing the picture of this profitable home builder. Looking only at the credit agency’s ratings, it would appear Meritage has a sizable risk of default.

Once we look at the firm’s credit from a Uniform Accounting perspective, it is apparent how little risk Meritage actually has. Even without a significant bump in home building, Meritage is at virtually no risk of defaulting.

SUMMARY and Meritage Homes Corporation Tearsheet

As the Uniform Accounting tearsheet for Meritage Homes Corporation (MTH:USA) highlights, the company trades at an 8.6x Uniform P/E, which is well below global corporate average valuation levels but arounds its own historical average valuations.

Low P/Es require low EPS growth to sustain them. That said, in the case of Meritage, the company has recently shown a 19% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Meritage’s Wall Street analyst-driven forecast projects a 53% and 20% Uniform EPS growth in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Meritage’s $88.47 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 10% each year over the next three years and still justify current prices. What Wall Street analysts expect for Meritage’s earnings growth is well above what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is 2x the long-run corporate average. However, intrinsic credit risk is 220bps above the risk-free rate. Together, this signals moderate credit and dividend risk.

To conclude, Meritage’s Uniform earnings growth is above its peer averages, but the company is trading well below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research