This IT player is stronger than the market perceives

N-able (NABL) is a provider of managed services and security solutions targeting small and medium-sized businesses.

The company has become a key IT management partner, serving over 20,000 managed service providers and supporting the IT infrastructure of more than 500,000 customers worldwide.

N-able’s revenue is largely generated from recurring services, accounting for over 90% of its total revenues, which contributes to its financial stability.

Despite these factors, rating agencies have concerns over N-able’s financial health amidst a challenging macroeconomic environment.

Today, we’re exploring N-able’s credit risk through the lens of Uniform Accounting to determine the accuracy of rating agencies’ assessments of the company.

We can use Uniform Accounting to put the company’s real profitability up against its obligations and decide for ourselves the true risk of this business.

Also below is a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

N-able (NABL) is a provider of managed services and security solutions for small and medium-sized businesses.

Founded in 1986, N-able has established itself as a trusted partner for IT management over the past three decades.

Today, N-able empowers over 20,000 managed service providers through its unified platform that offers remote monitoring and management, backup and disaster recovery, and security services.

Its solutions help MSPs efficiently manage the IT infrastructure and applications of over 500,000 customers globally across various industries. Over the years, N-able has grown organically as well as through strategic acquisitions of complementary businesses to enhance its capabilities.

N-able generates recurring revenue streams through long-term subscription contracts with its customers.

Over 90% of its revenues come from recurring services. This provides financial stability compared to businesses dependent on one-time projects. N-able has also maintained a strong balance sheet, with low debt levels and consistent positive cash flows.

While N-Able has built a well-recognized brand name and loyal customer base through its consistent service quality, rating agencies have expressed concerns about the company’s prospects in the current macroeconomic environment.

The global economy is slowing down significantly due to high inflation, rising interest rates, and geopolitical tensions. This has led to widespread job cuts, especially in the tech sector. There are also warnings of an impending recession.

S&P gave the company a “B+” rating, indicating a significant risk of default at nearly 25% over the next five years. It also puts the company in the high-yield basket.

Given its solid financial standing, we believe N-Able deserves a more secure rating.

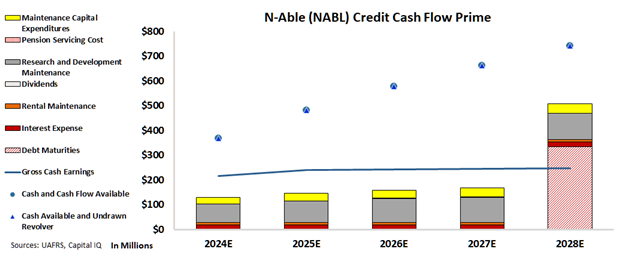

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (“CCFP”) to understand how the company’s obligations match against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart shows that N-Able’s cash and cash flows are more than enough to serve all its obligations going forward.

The chart indicates that the company is on solid financial ground and is very likely to fulfill its obligations with ease in the next five years.

The company has debt maturities coming in 2028 but its substantial cash flows and cash on hand should easily cover all of its obligations.

While macroeconomic conditions have weakened with high inflation and rising interest rates, N-able’s established market position and loyal customer base provide resilience.

Its decades-long experience and comprehensive suite of solutions tailored for the SMB segment have created a differentiated value proposition. Strategic partnerships with technology leaders help N-able continuously integrate best-of-breed capabilities.

Our review of N-Able shows that the company has a low risk of default, contrary to what rating agencies indicate.

Therefore, we are assigning an “IG4+” rating to the company, which places it in the investment-grade basket, with a risk of default of about 2%.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and N-Able (NABL:USA) Tearsheet

As the Uniform Accounting tearsheet for N-Able (NABL:USA) highlights, the Uniform P/E trades at 26.2x, which is above the global corporate average of 22.9x but below its historical P/E of 31.6x.

High P/Es require high EPS growth to sustain them. In the case of N-Able, the company has recently shown a 75% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations, that in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, N-Able’s Wall Street analyst-driven forecast is an 8% and 15% EPS growth in 2024 and 2025, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify N-Able’s $13 stock price. These are often referred to as market-embedded expectations.

Furthermore, the company’s earning power in 2023 was 4x the long-run corporate average. Moreover, cash flows and cash on hand are 3x its total obligations—including debt maturities and capex maintenance.

Overall, this signals a low credit risk.

Lastly, N-Able’s Uniform earnings growth is above its peer averages and is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research